The market recently corrected sharply due to weak global cues, and the imposition of dividend distribution tax on equity oriented mutual funds & long term capital gains. It, however, managed to break the fall, and tried to recover with support from bargain hunting and bounce-back in global peers.

Last week, the market lost 3 percent and ended over its one-month low at 34,005.76 on the Sensex, but recovered nearly 300 points to end at 34,300.47 on Monday. In fact, the broader markets recovered faster than frontline indices as investors got an opportunity to buy quality stocks on sharp correction.

This recovery may continue but consolidation is majorly seen in short term as the market will watch out for stability in global peers before sharp recovery, so further correction can't be ruled out, experts suggest.

As we are near the fag end of the earnings season and most of major corporate earnings already priced in, and no major event lined up in the offing, the market is likely to take cues from globe, according to experts.

"We feel global cues will continue to dominate our market trend, in absence of any major event. Nifty may see some bounce or consolidate further however sustainability at higher level seems difficult," Jayant Manglik, President, Religare Broking said.

Traders should use further recovery to reduce existing longs and creating fresh shorts, he advised.

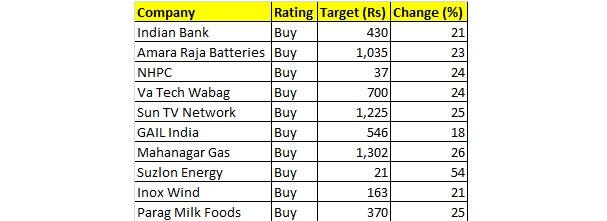

Here are top 10 stocks that can give up to 54 percent return in 12 months:

Indian Bank reported core operating profit (excluding treasury gains) growth of 55 percent YoY to Rs 1,130 crore. However, PAT of Rs 300 crore was 38 percent below estimates, as provisions of Rs 920 crore were above estimates (included Rs 470 crore of provisions for MTM losses).

NII grew 30 percent YoY (6 percent above estimate) led by 22 percent YoY loan growth and 3bp QoQ improvement in global margins. NII growth was partially offset by other income.

Fresh slippages increased 168 percent QoQ led by 4 lumpy accounts slipping from SDR. However, elevated write-offs and sale to ARCs led to QoQ flat gross non-performing assets at Rs 9,600 crore.

The Bank has a total exposure of Rs 2,640 croreb (8 accounts) towards first list and Rs 740 crore towards second list (10 accounts). The bank has made total provisions of Rs 1,820 crore towards the two lists against a requirement of Rs 1,980 crore (by FY18), the balance to be made in Q4FY18.

Focus on balance sheet consolidation and core operating parameters has led to improving earnings, despite challenging macros. Indian Bank has a strong capital position with Tier-1 of 10.9 percent and is thus well-poised to grow its loan book and benefit from further improvement in operating leverage.

We upgrade FY19/FY20 PAT estimates by 6 percent/10 percent to account for pick up in loan growth and opex control.

Amara Raja Batteries | Rating - Buy | CMP - Rs 845 | Target - Rs 1,035 | Return - 23%Net sales grew 17.1 percent YoY (+8.8 percent QoQ), led by growth in auto across the OE and aftermarket segments. This was led by continued channel expansion of Amaron and Powerzone brands. Further, higher exports to South-East Asia and Middle-East countries aided growth in the auto segment. Industrial battery segment too recorded growth, backed by higher sales in UPS segment and a sequential increase in volumes in the telecom segment.

EBITDA margin expanded 20bp YoY (-110bp YoY) to 15.6 percent, led by a favorable product mix (higher share of autos), optimal utilization, and price hikes. High other income and low depreciation boosted PAT by 20 percent YoY.

Management guided for capex of Rs 400 crore each in FY18/19 and expects 2-wheeler capacity to touch 15 million units (by May-18). Current 4-W capacity is 10.5 million units, which company expects 12 million units by end FY19.

We keep FY19/FY20 earnings estimates unchanged.

NHPC | Rating - Buy | CMP - Rs 30 | Target - Rs 37 | Return - 24%NHPC’s Q3FY18 underlying PAT grew 40 percent YoY (ahead of our estimate), led by higher incentive income, lower other expenses, and saving in interest cost. Underlying PAT is adjusted for (a) dividend income from NHDC and (b) late payment surcharge.

Generation was up 1 percent YoY to 3.4 billion units. PAF increased around 270bp YoY to 76.8 percent. Incentive income increased 59 percent YoY to Rs 110 crore.

Interest cost saving of Rs 110 crore was achieved on repayment and refinancing of debt. Refinancing will generate annualized saving of Rs 34 crore, of which Rs 17 crore will be retained by NHPC.

Of the five projects pending capex approval, PIB has cleared three projects and the remaining two are likely to get cleared over the next few months. The next step is approval by Cabinet Committee before final tariff orders are issued by CERC. Rs 680 crore of revenue was pending recognition due to capex approval at the end of FY17.

We expect Parbati-II to be commercialised in FY21 against FY20 earlier. Resultantly, consolidated PAT is cut by around 13 percent and DPS is cut from Rs 2.25 per share to Rs 2 per share for FY20.

VA Tech Wabag | Rating - Buy | CMP - Rs 562 | Target - Rs 700 | Return - 24%Consolidated sales grew 20 percent YoY to Rs 870 crore, below our estimate of Rs 930 crore. Revenue growth was supported by a pick-up in execution of key orders like Petronas (Malaysia), Polghawela (Sri Lanka), Koyambedu (Chennai), AP Genco and AMAS (Bahrain). Standalone sales rose 21 percent YoY, while subsidiary sales grew 20 percent.

In Q3FY18, consolidated order intake declined 74 percent YoY to Rs 32 crore, while order backlog fell 14 percent YoY at Rs 6,520 crore.

Management maintained its FY18 guidance of revenue of Rs 3,800-4,000 crore (+25%) and order inflow of Rs 4,300-4,500 crore (+25%). Order guidance for FY18 implies around Rs 2,500 crore in Q4FY18 – of this, Rs 1,000 crore is from India, Rs 1,000 crore from GCC countries and Rs 300-400 crore from Europe.

We cut FY18/19 estimates by 4/6 percent to factor in lower order inflows and resultant execution over the next few years. We maintain Buy with a target price of Rs 700.

We believe that from the medium- to long-term perspective, VA Tech is in a sweet spot to take advantage of a pick-up in domestic order inflows, led by state-driven municipal orders, and central government schemes like Namami Gange, AMRUT, Swachh Bharat and Smart Cities.

Sun TV Network | Rating - Buy | CMP - Rs 984 | Target - Rs 1,225 | Return - 25%Subscription revenues are likely to grow at 16 percent CAGR over FY18-20, led by digitization in Tamil Nadu. We believe there is further upside, driven by higher market share of DTH players, growth in MSO-led subscription revenue following TRAI’s tariff order requiring price parity, as well as growing HD penetration and ARPU increase.

Higher viewership on the back of content rejig coupled with shift to commission model should help Sun TV capitalise on potential ad revenue growth. Given the low base of FY17, we expect 14 percent CAGR over FY18-20.

Near doubling of IPL revenue to Rs 280 crore, driven by substantially higher auction of media rights and fresh inventory driving the radio business bodes well. Steady movie investments should lead RoCE to reach around 33 percent by FY20.

With the growth pillars in place, we believe Sun TV is well poised to witness standalone revenue/PAT CAGR of 16/24 percent over FY18-20.

With growth revival in the next 2-3 years driving healthy standalone EPS CAGR of 24 percent, RoE of 33 percent and steady FCF generation, the stock should continue to offer healthy upside.

Prabhudas LilladherGAIL India | Rating - Buy | CMP - Rs 464 | Target - Rs 546 | Return - 18%GAIL reported strong Q3FY18 results. It has multiple growth drivers in the medium term led by 1) improving profitability at the gas transmission and LPG division on the back of higher volumes and benign gas prices 2) likely implementation of unified pipeline tariff and 3) rising confidence on placement of US LNG volumes given sharp jump in crude oil prices; bulk of CY18 placed and over 50 percent of CY19 volumes placed.

GAIL's Q3 transmission volumes improved to 109mmscmd (106 in Q2) due to higher volumes to power and fertiliser sector. However, transmission EBIDTA was impacted by provision of Rs 80 crore for settlement of dues and higher raw material and employee costs for Rs 57 crore. LPG EBIDTA was robust at Rs 680 crore (+45 percent QoQ), supported by higher realisation.

Petrochemicals operating performance improved as the plant operations remain strong.

We increase estimates by 8 percent for FY18/19E to factor in higher LPG prices tracking higher crude oil prices and make other minor changes. We expect GAIL to benefit from full utilisation of petrochemicals capacity as also from increased gas utilisation in the overall energy footprint. Maintain Buy" with revised DCF-based price target of Rs 546 (Rs 534 earlier).

Mahanagar Gas | Rating - Buy | CMP - Rs 1,030 | Target - Rs 1,302 | Return - 26%Going forward, CNG volumes are likely to remain improve on the back addition of organic and geographical expansion. Also, government's push for PNG's domestic connections will support volumes. Tailwinds of cheaper domestic gas, opportunities in two-wheeler space, along with favourable demand traction from new geography, will drive earnings.

CNG/PNG sales volume traction is likely to continue on the back of continued conversion of taxis/private vehicles, along with geographical expansion.

We increase earnings estimates by 2/7 percent for FY18/19 to factor in improvement in margins. MGL remains a play on increased gas penetration from rising vehicle and PNG penetration. Reiterate Buy with a PT of Rs 1,302 (Rs 1,267 earlier).

KR ChokseySuzlon Energy | Rating - Buy | CMP - Rs 13.9 | Target - Rs 21 | Return - 54%We believe negatives are already discounted in the stock price. Going ahead, better execution largely on account of strong visibility post SECI auctions can augur well for the entire industry.

Further, many IPP’s have adjusted their IRRs assumptions post witnessed a decline in the wind tariff as OEMs are not going to reduce price beyond certain limit. This in turn could provide some stability in the operational performance of wind players in the years to come.

We have revised estimates for FY18 to incorporate better wind execution. We assigned 8.5x EV/EBITDA on FY20 and arrived a target price of Rs 21, potential upside of around 54 percent from CMP of Rs 13.9.

(Note: Improvement in the ordering activity from SECI provides strong revenue visibility going ahead. Further, any progress towards divesting stake in O&M business along with positive surprise of getting ratification for 455MW worth of wind contracts will remain a key trigger for improvement in the valuations going ahead.)

Inox Wind | Rating - Buy | CMP - Rs 127 | Target - Rs 163 | Return - 21%Karnataka govt has started to ratify earlier signed PPAs. Inox has around 150MW of wind contracts towards Karnataka, which is expected to get commissioned in Q4FY18. Hence, working capital to the tune of Rs 800-1,000 crore will be eased in the coming quarter.

In terms of execution of SECI 1 & 2 contracts, we expect given the 18 months timeframe is stipulated by SECI, the company is poised to commission at least 600MW in FY19.

Additionally, any success on winning contracts from SECI 3 & 4 could provide some visibility for FY19 and thereby FY20.

We have lowered estimates for FY18 to adjust poor execution. We have valued the company on 8x of FY20E earnings of Rs 20.4, we arrived a target price of Rs 163, an upside potential of 29 percent from CMP of 127. We have Buy rating on the stock.

EdelweissParag Milk Foods | Rating - Buy | CMP - Rs 296 | Target - Rs 370 | Return - 25%Parag Milk Foods’ Q3FY18 revenue grew 16 percent YoY (beating estimates by 6 percent) post mere 7 percent YoY growth in H1FY18, following bounce back in value-added products (VADP) at 16 percent YoY growth.

Gross margin expanded by strong 1,053bps to 30.7 percent (20.2 percent in Q3FY17 and 28.0 percent in Q2FY18), led by better realisation and favourable input costs, as the average procurement price declined by 4-5 percent QoQ. EBITDA stood at Rs 58.8 crore (beating estimates by 26 percent) compared to loss of Rs 18.3 crore in Q3FY17, leading to EBITDA margin at 11.3 percent (-4.1 percent in Q3FY17 and 9.9 percent in Q2FY18).

We expect the growth momentum to sustain and estimate VADP’s share in sales to catapult to 70 percent (66 percent currently) over FY17-20, riding sustained innovation focus and increasing utilisation in high-margin products (whey consumer, paneer, cheese).

On strong beat in gross and EBIDTA margins, we raise FY18/19/20 earnings estimates by 21/21/9 percent and estimate earnings CAGR of 21 percent over FY18-20, and RoCE to catapult to 19.5 percent. Maintain Buy, valuing the stock at 24x FY20E P/E, with a revised target price of Rs 370 (Rs 340 earlier).

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.