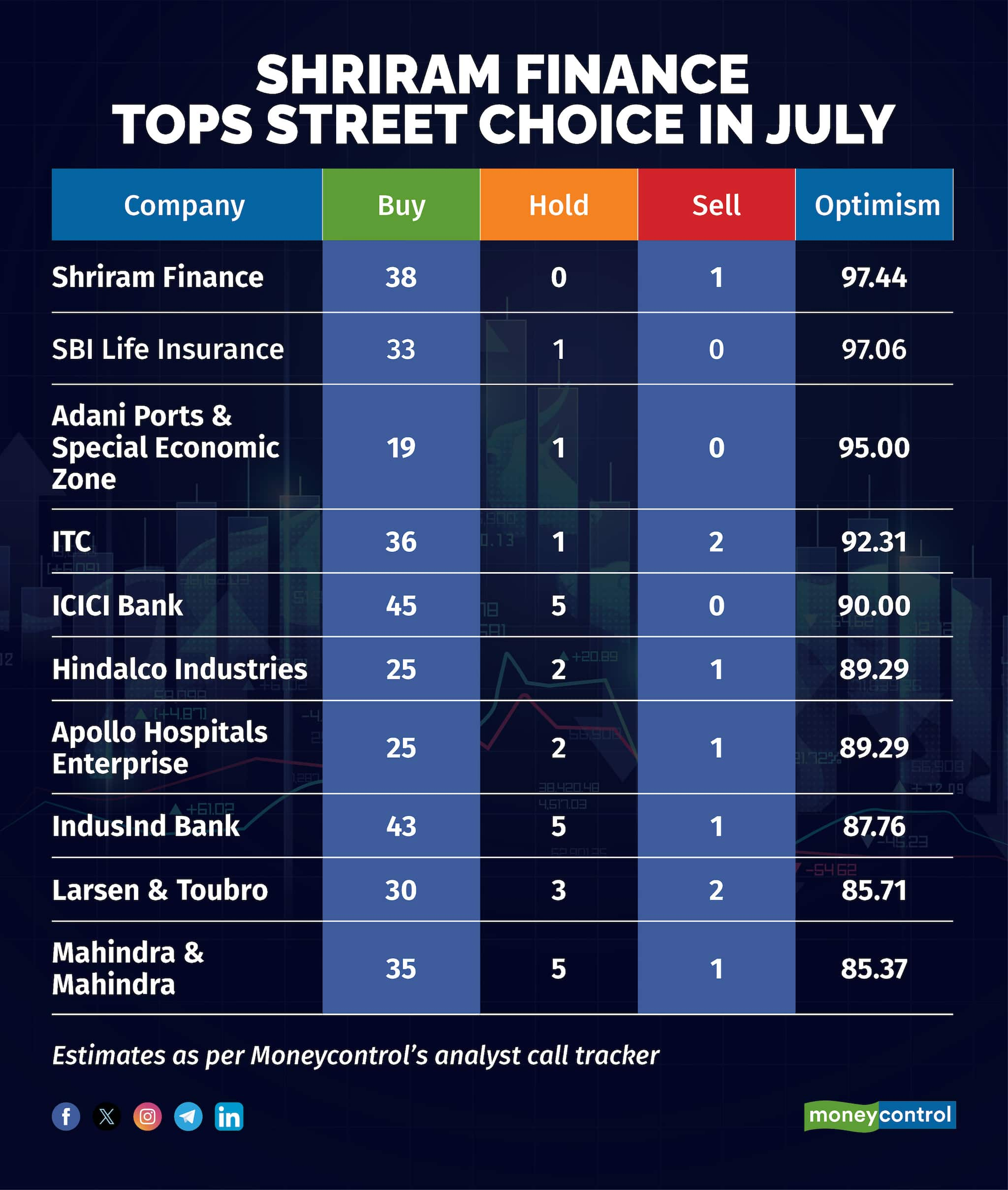

India's largest retail non-bank lender Shriram Finance continued to be analysts’ most favourite pick in July, again topping the list of Nifty 50 stocks with maximum optimism. The NBFC stock gained more strength with ratings upgrades during the month -- it now has 38 'buy' calls and just one 'sell' call from analysts, according to Moneycontrol's analyst call tracker.

The optimism on the stock is due impressive back-to-back quarterly performance, attractive valuations, historically low bad loans, and a positive growth outlook.

Elara Securities maintained an 'accumulate' rating on Shriram Finance, increasing its target price to Rs 3,140 per share, reflecting a 9 percent upside potential from current levels. Analysts expect that a favourable asset mix, cross-selling opportunities, and the benefits from a recent merger of group entities will enhance Shriram Finance's earnings.

JM Financial noted Shriram Financial’s robust growth potential due to a high proportion of secured loans (96 percent) amid concerns about unsecured lending. Additionally, its substantial provisions balance (total ECL provisions at 6.3 percent of AUM) will help shield the lender from unforeseen shocks. JM Financial maintained a 'buy' rating with a target price of Rs 3,460 per share.

All-round Q1 show

In the April-June quarter, Shriram Finance delivered strong results with an 18 percent year-on-year profit growth to Rs 2,022 crore, driven by a 21 percent increase in AUM and net interest income. The company plans to expand its MSME and gold loan offerings, which is expected to further boost AUM growth and yields.

Despite a 23 basis point YoY decline in net interest margins (NIMs) to 8.79 percent in Q1 FY25 due to a drop in the cost of borrowing, the management expects the cost of funds to remain stable. They expect to maintain NIMs at 9 percent for FY25E, supported by shorter-term, high-yield products.

Meanwhile, its asset-quality has shown consistent improvement in the last 2 years. Shriram Finance's gross non-performing asset (GNPA) stood at 5.39 percent in Q1FY25, down 64 bps YoY and net NPA stood at 2.71 percent, down 25 bps YoY.

Its arm Shriram Housing also reported healthy topline growth, with NII up 41 percent YoY in Q1FY25, but higher opex growth restricted profit growth to 16 percent YoY.

Attractive valuations ripe for re-rating

HDFC Securities said that Shriram Finance has ample liquidity to meet its growth target. "The RoA and RoE ratios of the company seem to be stabilising now and expected to expand from current levels," said the brokerage analysts. They see an upside potential of 19 percent on Shriram Finance stock.

So far this year, shares of Shriram Finance jumped over 44 percent, outpacing benchmark Nifty 50's 12 percent rise. In a year, the stock has witnessed a sharp run-up of over 60 percent.

Currently trading at a price-to-earnings (PE) ratio of 14.36, Shriram Finance is valued lower than the sector's PE ratio of 19.81x. Analysts at HDFC Securities believe that despite comparable return ratios and AUM growth, Shriram Finance's valuations are significantly discounted relative to its peers. They recommend buying the stock within the Rs 2,905-2,955 range and adding on dips between Rs 2,630-2,670, with a base case fair value of Rs 3,225 and a bull case fair value of Rs 3,440 over the next 2-3 quarters.

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.