Neha Dave

Moneycontrol Research

CreditAccess Grameen’s Rs 1,131 crore initial public offering (IPO) opens for subscription today. The company plans to raise Rs 630 crore of fresh capital in addition to an offer-for-sale from promoters and existing shareholders amounting to Rs 500 crore. The primary market offering of the non–bank microfinance institution comes at a time when the MFIs are back on the growth path, shrugging off impact of demonetisation, which proved to be an Achilles heel for the sector.

In addition to the sector’s demonstrated resilience and growth potential, some of the structural changes has made microfinance a promising sector. The sector is thriving with eight MFIs converting into small finance banks (SFBs) and one of the largest MFIs (Bandhan Bank) transitioning into a universal bank. Acquisition of Bharat Financial by IndusInd Bank has added to the dynamism in the sector.

CreditAccess Grameen (CAGL), the third largest MFI in term of loan book size as at March-end, operates right at the heart of rural India, providing finance to the unserved masses at the bottom of the socio-economic pyramid making it a unique rural financial services play.

Background and financials

CAGL is an established player in the microfinance industry with over 18 years of operations. Promoter CreditAccess Asia NV holds 98.8% stake in the company which will reduce to 80.3% after the issue. The Netherlands-based entity provides financial services to micro and small businesses and self-employed people, via controlled companies, in India, Vietnam, Indonesia and the Philippines.

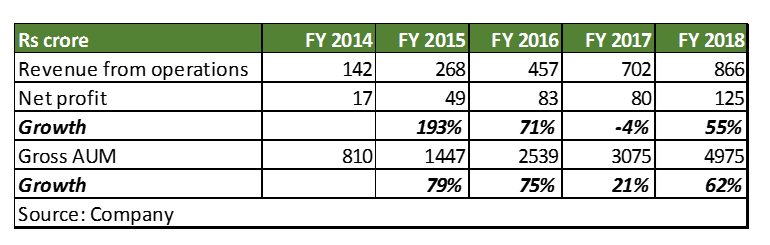

As at March-end, it had a loan portfolio of Rs 4,975 crore serving 1.85 billion active borrowers across 132 districts of Karnataka, Maharashtra, Tamil Nadu, Madhya Pradesh and Chhattisgarh. Despite the demonetisation induced slowdown in FY17, loan book has grown 44 percent (compounded annually) between FY14 and FY18.

Financials at a glance

The company provides micro-credit to economically backward women through the joint liability group (JLG) mechanism. The core focus is to provide income generation loans to customers, which comprised 87 percent of total JLG loan portfolio as of March-end. Credit risk, which is inherent in any financing business, is generally lower in case of lending through JLG. The access of personal information of each group member and social pressures are the key reasons for the same. However, the JLG model can prove to be a double-edged sword — containing risks in good times, but triggering large-sale defaults during a crisis.

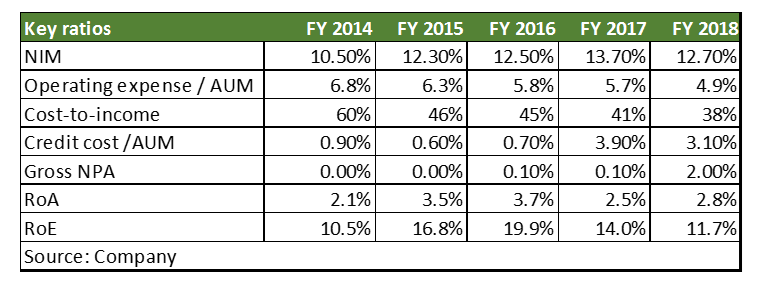

Something similar was experienced by CAGL. It witnessed a steep deterioration in asset quality after demonetisation. The same was reflected in its gross non-performing assets (GNPA) which rose 2 percent in FY18 from 0.10 percent in FY17. This was because the company had made use of the Reserve Bank dispensation for deferral of recognition of NPAs in FY17. Recognising the pain in FY18 led to increase in NPAs and provisioning. On account of additional provisioning during FY17, profitability was impacted with return on assets falling to 2.3% in FY17 from 3.6% in FY16.

In FY18, CAGL’s credit costs – albeit elevated compared to its historical average - declined, thereby supporting its profitability, with RoA improving to 2.8% in FY18.

Credit costs can remain high going forward, in line with the change in its provisioning policy. The transition to IndAS will require the company to assess provision requirement based on forward looking expectations vis-a vis the backward looking days past due (DPD) used currently. While expected credit loss (ECL) can be higher, the management sounded confident on credit loss declining going forward.

CAGL has maintained its strong operating efficiency over the years as reflected by the cost-to-income ratio of about 38% and operating profit-to-average managed assets of 4.9% during FY18.

What we like about CAGL?

Though Karnataka accounted for around 59% of the company’s portfolio exposing it to risks associated with significant regional concentration, no single district (apart from one) contributes more than 5% to gross loans. The regional concentration will continue to reduce as CAGL scales up through its district-based expansion strategy.

CAGL’s significant rural presence – close to 82% of branches and about 81% of the customers are in rural areas, its predominantly weekly collection model, and prudent customer on-boarding and monitoring provides comfort to an extent.

There is scope for potential return improvement driven by lower credit costs and controlled expenses. As the company levers its capital to grow the loan book, return on equity should improve significantly.

Microfinance sector can be a roller coaster ride

The microfinance sector has come a long way from just a 'not-for-profit' endeavour to a business model of sustainable growth with strong returns. The remarkable journey has been marked by many highs and lows. The exponential growth of the sector was halted by the Andhra Pradesh crisis in 2010. Evolution of the regulatory framework after the crisis has helped the sector mature while attempting to protect the borrower’s interest by regulating product pricing. While demonetisation disrupted the sector once again in November, 2016, it is heartening to see growth return to pre-demonetisation levels

Given the enormous potential, rating agency ICRA expects traction in disbursements to sustain and the microfinance industry to report 25-30% per annum portfolio growth over the medium term.

However, low income group concentration, unsecured nature of lending and political risks are the key concerns for the sector.

Issue priced to perfectionWhile microfinance is a relatively riskier asset segment with weak borrower profile, susceptible to socio-political issues and resulting unhealthy credit culture, few in the industry boasts of a track record as CAGL.

At the upper end of the price band (Rs 422 per share), the stock is valued at 2.9 times trailing book on a post-money basis. While the MFI has strong earnings growth potential and ability to generate RoA of around 3-3.5%, part of the near term growth seems to be priced in. On a relative basis, valuations are at a premium when compared to small finance banks (SFBs) like Ujiivan and Equitas operating in the micro-lending space. Hence, we see limited scope for listing gains.

There can be upside potential emanating from the possibility of an acquisition by a bank. While investors can play the sector through SFBs, a lower cost structure, higher returns and potential to convert or being acquired by a bank makes a pure-play MFI a worthy consideration and should support relatively higher valuations. Investors with an ability to shoulder risks associated with a microfinance business and looking for high quality business operating at the bottom of the pyramid should subscribe to the IPO for long term gains.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!