Specialty chemicals manufacturer Rossari Biotech has become the first company to launch an initial public offering (IPO) during the coronavirus lockdown and the second after SBI Cards this year. The company was to launch its IPO in March but unfavourable market conditions forced it to put off the plan.

The Mumbai-based company opened its Rs 496-crore IPO for subscription from July 13 to 15 with a price band of Rs 423-425 per share.

The IPO comprises a fresh issue of Rs 50 crore and offer-for-sale of up to 1.05 crore equity shares by promoters Edward Menezes and Sunil Chari, who are selling 52.5 lakh shares each.

ALSO READ: Rossari Biotech IPO, Bharat Bond ETF & Yes Bank FPO: Where should investors put their money?

Given the company's debt-free status, best asset turnover ratio, strong financial performance and an increase in demand for hygiene products after COVID-19 pandemic, a majority of brokerages advise subscribing to the issue for listing gains and long-term investment despite a high valuation.

At the upper end of the price band, Rossari Biotech demands PE multiple of 31-33x FY20 fully diluted EPS, while its peers such as Aarti Industries, Fine Organics, Vinati Organics, Atul and Galaxy Surfactants are available at PE multiples of 31x, 35-36x, 31x, 21x and 24x FY20 fully diluted EPS respectively.

"None of the listed chemical companies has the same business as Rossari. We believe Rossari will command a premium over most of its chemical peers as it is net debt-free as well as it has better asset turnover, working capital days, RoE and RoCE better than most of its peers. Only 10 percent of sales are dependent on imported raw material, of which less than 5 percent comes from China. As we are positive on the future outlook for the industry as well as the company, we would recommend subscribing to the issue," Angel Broking said.

Arihant Capital Markets, which has a positive outlook on the company's growth prospects, said due to a growing demand for hand sanitisers, disinfectants and cleaning chemicals manufactured by Rossari, its business performance has boomed. "Thus, we recommend investors to subscribe for this issue."

Rossari Biotech has a well-diversified product portfolio of 2,030 different products across its three categories--home, personal care and performance chemicals (HPPC; 47 percent revenue share); textile specialty chemicals (TSC; 44 percent revenue share) and animal health and nutrition products (AHNP; 10 percent revenue share).

The company has delivered robust growth in revenue/EBITDA/PAT over FY15-FY20, reporting CAGRs of 31/51/78 percent, leading to high return ratios (RoE/RoCE), largely due to its strong promoter and management team.

Its return on equity (RoE) has increased from 7.9 percent in FY15 to 22.8 percent in FY20, registering a growth of 1,490 bps. Similarly, the return on capital employed (RoCE) has increased from 8.7 percent in FY15 to 18.8 percent in FY20, at a growth of 1,010 bps.

Rossari also has a high return on invested capital (RoIC) of 31.6 percent in FY20 compared to 8.8 percent in FY15 due to the flexible assets that can be used for multiple purposes and it is a flexible and agile company known for its speed to market innovative products and customised solutions, said Ventura, which also recommended subscribing the issue.

After its Silvassa facility, having an installed capacity of 1,20,000 MTPA, the company is adding another plant at Dahej that is expected to be a game-changer, brokerages said.

"High asset turnover in the business of more than 6x (FY20) augurs well for around Rs 540 crore incremental revenue potential from capacity expansion at peak utilisation," said Emkay Global.

The first phase (30,000 MT) of the second facility started in July 2020 and balance would come online by March 2021.

"The new capacity expansion at Dahej (1,32,500 MTPA) with Rs 90 crore capex should strengthen its portfolio in the high-growth HPPC segment to serve its wide customer base. Customised product offering, fungible capacities and rapid finished product conversion rate remain the key differentiators for the company," said Emkay. It, too, favoured subscribing the issue.

While the valuations may appear high, Motilal Oswal also likes the company given its strong financial performance, lean balance sheet and doubling of capacity over that next one year.

Hence, investors can subscribe to the IPO from a long-term perspective, the brokerage said. Considering market conditions and bright prospects for specialty chemical space, one may also get listing gains, it feels.

Rossari holds around 6 percent market share in the highly fragmented textile specialty chemicals (TSC), which has grown at an 11 percent CAGR over FY18-20, while its HPPC and AHNP segments have grown at 125/39 percent CAGRs over FY18-20.

Management is keen on sustaining TSC market share and is confident of Health and Hygiene Prospects (HPPC) to supplement growth by consistently delivering tailored solutions across all business segments.

In addition, expansion plans are ongoing, which should enable to service segments such as water treatment solutions (in place), pet shampoos, distilleries, dairy industry and breweries (R&D completed), Emkay said.

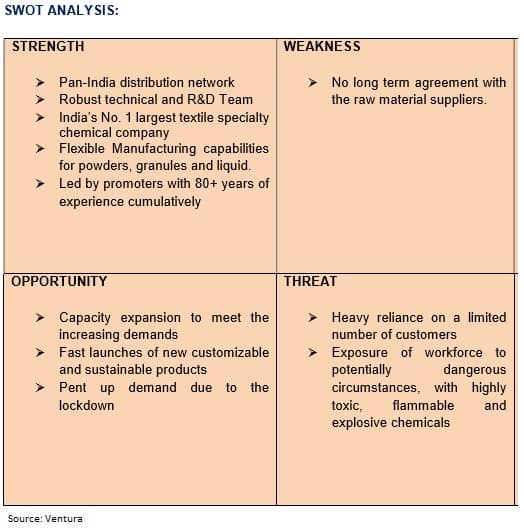

However, brokerages say any slowdown in the textile industry, dependence for revenue on a few customers, a delay in capacity addition and failure in maintaining return ratios, etc could be risky.

Rossari Biotech will utilise around Rs 100 crore raised from the fresh issue and the pre-IPO placement for debt repayment (Rs 65 crore), working capital requirements (Rs 50 crore) and balance for general corporate purpose. After the IPO promoters' shareholding will reduce to 72.7 percent from 95.1 percent.

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not that of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!