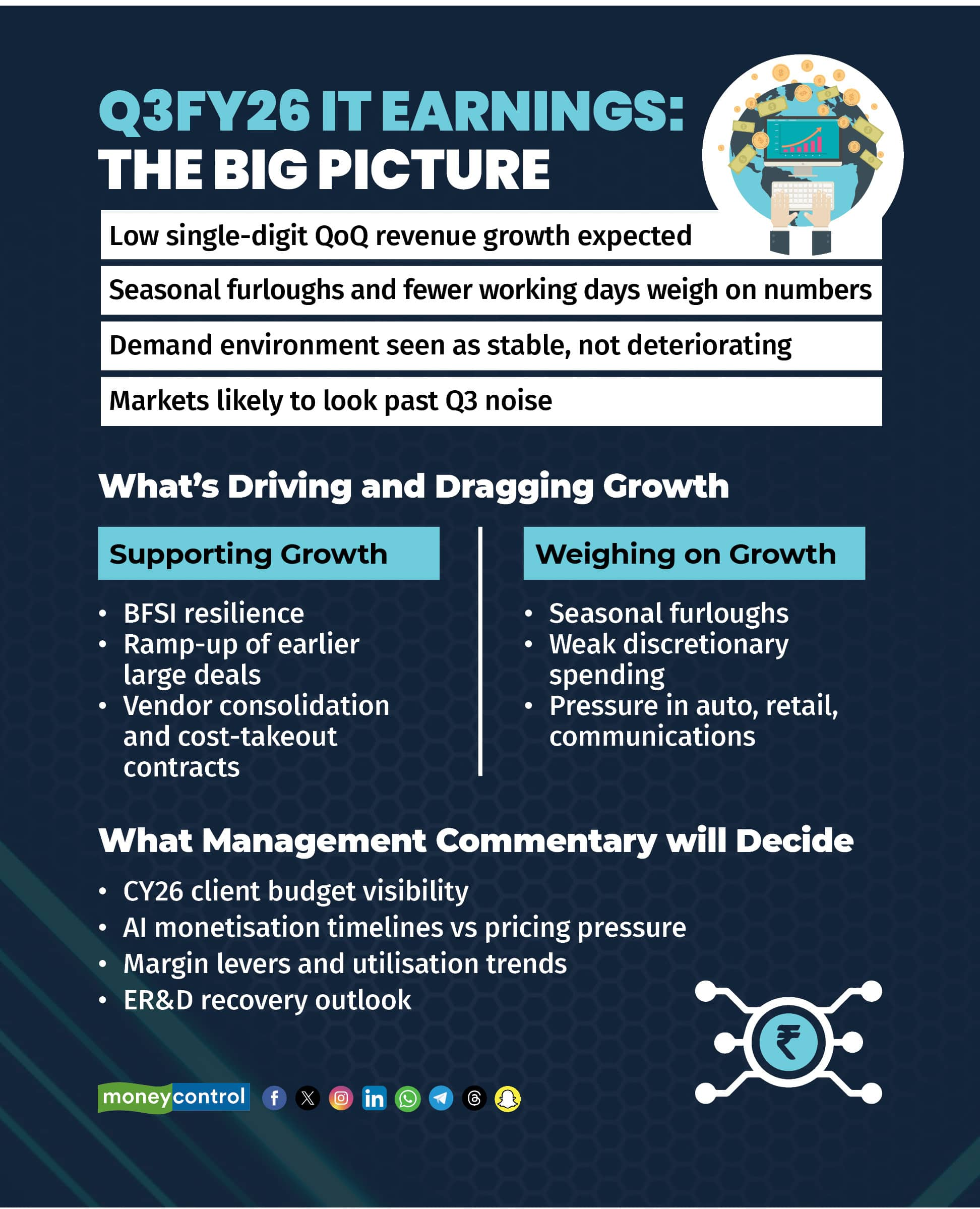

Brokerages expect information technology (IT) services sector to report another unexciting quarter, with seasonal furloughs, fewer working days and cautious client spending in the October-December period keeping third quarter revenue growth in check.

While the demand environment is seen as broadly stable, analysts do not expect a decisive pickup in discretionary spending. The Street is of the view that the December quarter will be more about looking past short-term noise and reading early signals on CY26 client budgets, AI monetisation, and margin sustainability.

Engineering, research and development (ER&D) shows early signs of stabilisation but remains fragile, while generative artificial intelligence (AI) continues to sit at the centre of the debate as both a productivity lever and a deflationary force.

Here are the five themes to watch out for in Q3FY26.

Seasonal softness, not demand collapse

Brokerages broadly agree that Q3 weakness will be driven more by seasonality than by a deterioration in demand. Furloughs and lower working days are expected to weigh on sequential growth, with large-cap IT companies seen reporting low single-digit constant currency growth.

The slowdown is in line with historical trends for the December quarter rather than a signal of worsening client behaviour, analysts say.

Growth has been driven largely by ramp-ups of previously won large deals and vendor consolidation contracts rather than any broad-based revival in discretionary technology spending.

“After some respite in 2QFY26 on beaten-down expectations, we expect seasonal furloughs to weigh on growth in 3QFY26. We think markets are likely to look through this seasonality and instead focus on signals around the demand environment from client budgeting for CY26,” brokerage Motilal Oswal Financial Services said in a pre-earnings research note.

BFSI continues to stand out as the most resilient vertical, while manufacturing, especially auto, along with retail and communications, remains under pressure.

Markets are expected to look past the seasonal softness and focus on commentary around demand visibility beyond the quarter.

Margins under pressure from furloughs, wage hikes

Margins are expected to remain under pressure, with the Street flagging furloughs, wage hikes and deal ramp-ups as near-term headwinds.

While rupee depreciation and AI-led productivity gains provide some cushion, analysts caution that seasonal inefficiencies, compensation resets and initial margin dilution from large deal ramp-ups are offsetting these.

Margin outcomes are, therefore, expected to remain mixed across companies.

Most brokerages believe that meaningful margin expansion will require a return to stronger revenue growth and improved utilisation, making Q3 more of a transitional quarter rather than a turning point.

“We expect the results of TCS (-70 bps QoQ), Persistent (-80 bps QoQ) and Coforge (-90 bps QoQ) to indicate the impact of salary increments during the quarter on margins,” Nomura said in its pre-earnings note.

AI: deeper embedding, limited revenue visibility

Generative AI is expected to feature prominently in management commentary but brokerages have cautioned against expecting any near-term revenue upside.

AI has moved decisively beyond pilots, with companies embedding it across application modernisation, testing, infrastructure operations, and data platforms. However, direct AI revenue contribution remains limited and largely bundled into larger transformation deals.

“Expansion in client tech budgets is not driving current AI adoption. Spending continues to be largely reallocated from existing IT and digital transformation pools, indicating that AI is, for now, a substitution layer within tech spend rather than a net new demand driver,” brokerage Emkay Research said.

While only Nomura has explicitly flagged AI-led deflation, other brokerages are increasingly pointing to a gap between rising AI-driven productivity and muted revenue growth.

The absence of incremental pricing benefits from AI adoption suggests that efficiency gains are being absorbed within existing contracts rather than being reflected in higher billing, particularly during renewals.

Wider enterprise adoption of AI, which could unlock larger deal sizes and incremental cloud and data spend, is expected to gather pace only over the next 12 to 18 months.

Visa risks slip down the priority list

Visa-related concerns have receded further, featuring more as a monitorable than a driver of earnings.

While ICICI Securities flagged H-1B renewal delays as a factor to track, most brokerages have not highlighted immigration issues as a material headwind for the December quarter.

“We await management commentary on… any impact from H1-B visa renewal delays due to US government shutdown/other policies,” the brokerage said in its pre-earnings release.

This marks a shift from earlier quarters when visa costs were discussed more actively in the context of delivery models and margins.

Brokerages had previously highlighted that visa-related constraints were largely a cost consideration and not a growth limiter. That assessment appears to be holding as companies lean more on offshore delivery and local hiring to manage regulatory risk.

Also read: H-1B visa lottery scrapped: Little change for Indian IT as reforms formalise long-running shift

ER&D: stabilisation, not recovery

ER&D, a drag through much of FY25 and early FY26, is expected to show stability rather than a sharp recovery in Q3.

Brokerages flag that tariff-related uncertainty and muted capex at global original equipment manufacturers continue to weigh on decision-making, particularly in auto and manufacturing-linked programmes.

While the pace of deal deferrals has slowed, analysts caution that ER&D spending remains closely tied to macro clarity.

Any sustained recovery in the vertical is now pushed to the second half of FY26 and will depend on easing tariff uncertainty and improved visibility on global manufacturing demand.

Also read: Nasscom ER&D head flags fundamental business model change, as IT sector faces similar churn

CY26 budgets take centre stage

With Q3 numbers unlikely to excite, brokerages say the focus will be on commentary around CY26 client budgets.

Analysts caution that limited clarity is likely to emerge from the Q3 earnings, as most global enterprises typically finalise their technology spending plans between January and February. While demand conditions are seen as stable, a sharper pickup in discretionary spending is expected only if macroeconomic conditions improve meaningfully.

Until then, growth recovery is expected to remain gradual and uneven, driven more by deal ramp-ups and cost-takeout programmes than fresh discretionary spend.

Bottom line

Q3FY26 is shaping up to be another holding quarter for the IT services sector. Any early signs of discretionary spending returning could begin to shift sentiment but for now, caution remains the dominant theme.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.