")

Making Flipkart synonymous with 'e-commerce' in India was not an easy milestone to achieve for co-founders Binny and Sachin Bansal. The fact that the concept of online shopping was unheard of when Flipkart was launched in 2007 and internet penetration was non-existent puts this further into perspective.

Binny Bansal resigned on November 13 after a probe was initiated against him in allegations of sexual misconduct, and Sachin Bansal quit after the Walmart-Flipkart merger. However, the company they started transformed e-commerce for both consumers and businesses.

Flipkart, as a start-up, started off by selling books online with doorstep delivery and had 20 shipments in their first year. Offline shopping was still a popular concept and consumers did not trust the internet as they do now for even small purchases.

The company grew over the next two years and hired its first employee in 2009. It also opened its first book to pre-order Dan Brown’s The Lost Symbol.

Accel Partners, a venture capital firm, bought into Flipkart’s idea and the company received its first funding of $1 million. The employee count and the number of offices increased. Then came another $10-million funding from a US hedge fund.

Flipkart received funding from SoftBank, Tencent, eBay and Microsoft in subsequent years and it expanded its products, delivery network and payment options. Internet facilitated the company’s innovation and helped establish the biggest e-commerce network in India.

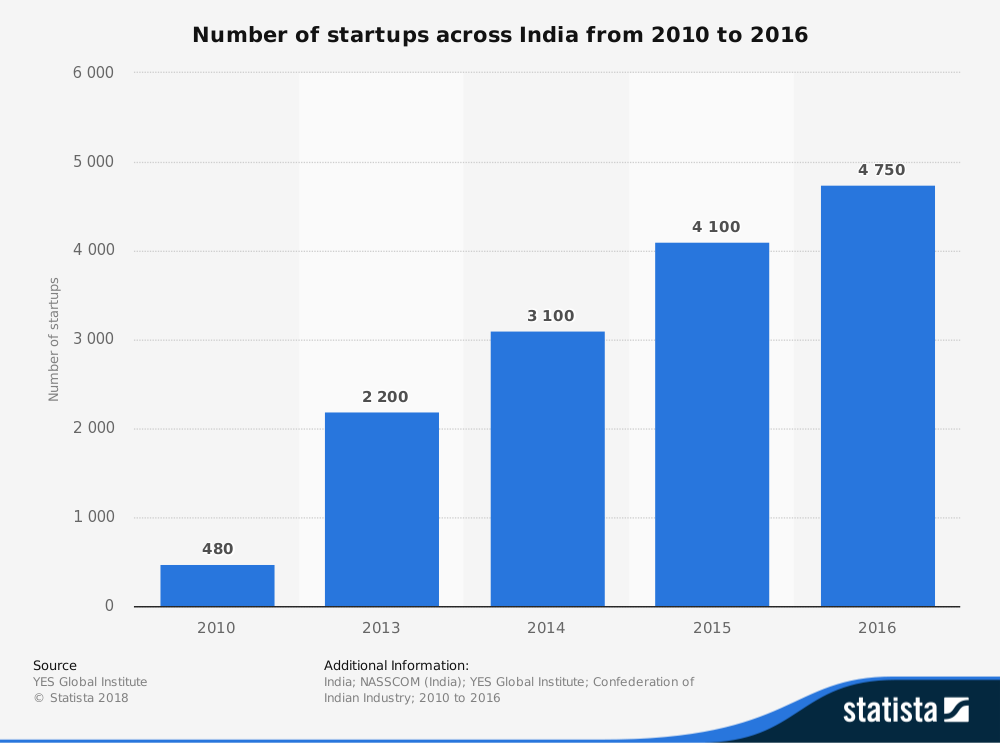

Make way for start-ups The success story of Flipkart has changed the landscape of India’s start-up ecosystem. The number of startups in India rose drastically from 2010 as confidence grew following Flipkart’s strides.

Source: Statista

Source: StatistaCorporate players realised the need for innovation and digitisation to expand business and serve customers better. They started working with start-ups in India and helped build one of the largest start-up hubs in the world. Corporate players brought their reach and resources, while start-ups lent the technology.

Financial technology has been one of the most consistent sections for start-ups over the years, with a stream of new players and investment by many reputed companies.

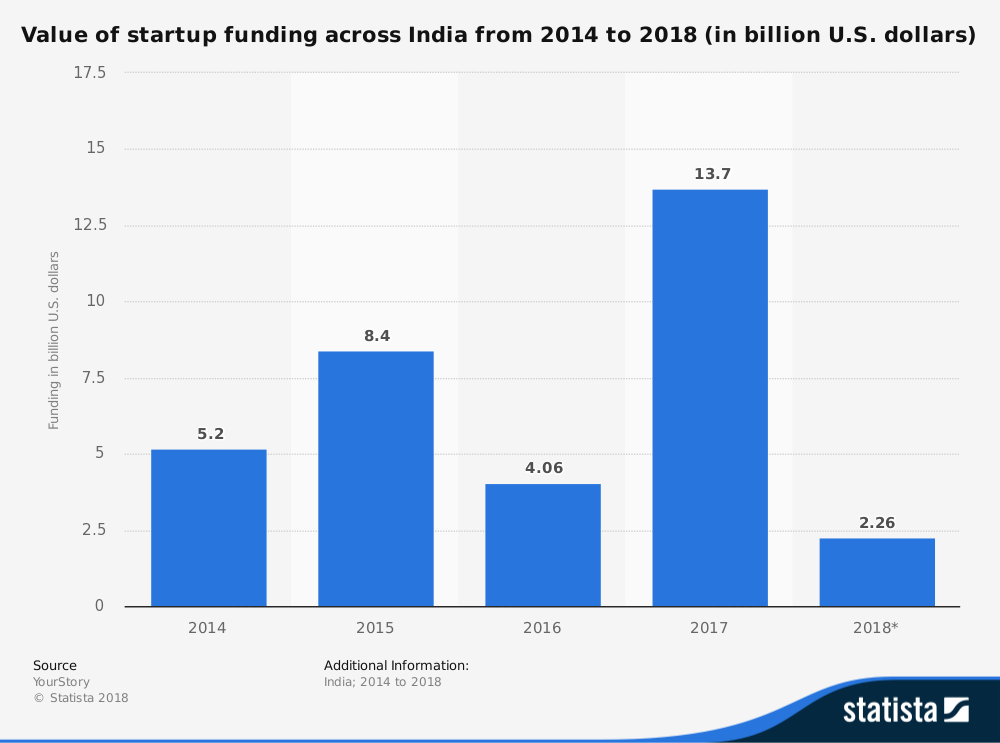

Funding rounds led by Indian start-ups increased in number every year. In 2017 alone, $13.7 billion was invested in 820 deals across India.

Source: Statista

Source: StatistaStart-ups valued over $1 billion, called unicorn start-ups, are fast growing. As of now, there are 13 unicorn start-ups in India including hospitality start-up Oyo Rooms, Ola Cabs, e-commerce platform SnapDeal, food delivery start-ups Zomato and Swiggy.

The number of mergers and acquisitions shot up significantly in 2017, with many non-tech Indian companies acquiring start-ups, including Walmart buying a controlling stake in Flipkart.

Introduction of entrepreneurship With the growth of start-ups in India, entrepreneurship was introduced in education and policy. Most courses at the under-graduate level train students in start-up business models and ideas.

Even the government realised the potential of the country’s start-up scenario and launched Startup India, a scheme to facilitate the growth of a business environment where new ideas and innovations could be implemented easily. The Centre has also introduced many policies to push India’s standing in the World Bank’s Ease of Doing Business index.

Sachin and Binny Bansal’s start-up was launched in a room and grew into an e-commerce behemoth to inspire thousands of ideas to turn into successful businesses.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.