Anubhav Sahu

Moneycontrol research

The slowdown in China growth even as various state-wide reforms unfold, including deleveraging, is an interesting aspect to look at. It perhaps has some policy implications for India, in terms of the sectoral impact, even as we witness potential credit moderation in non-banking finance companies (NBFC).

Further, given the weak domestic growth, the US-China trade war can potentially thaw supply-side reforms, which can have ramification for sectors like metals and chemicals.

GDP growth lower-than-expected, but exports data surprised

Economic growth in China has slowed down more-than-anticipated in Q3 CY18. GDP numbers at 6.5 percent (versus 6.6 percent in Q2 CY18) was lower than consensus expectation of 6.6 percent. This is slowest growth after the global financial crises (2008-09) for a country that is transitioning from investment to a consumption-led one.

Interestingly, China posted a record trade surplus in September ($34 billion) with respect to the US. For nine months of CY18, China’s trade surplus with the US was $226 billion, which is 15 percent higher than last year.

The recent upsurge, however, is more likely due to bringing forward import orders before US tariffs gets implemented.

Deleveraging cycle has begun

The reason behind China’s economic growth slowdown can be mainly attributed to slowing domestic growth as the country moves ahead with rebalancing of the economy: from investment to consumption. In recent times, gross capital formation (proxy for investment) to GDP growth was 42 percent in 2015, which reduced to 31.5 percent in Q2 CY18. At the same time, share of consumption expenditure to GDP growth has risen from 59.7 percent to 79.2 percent over the same period.

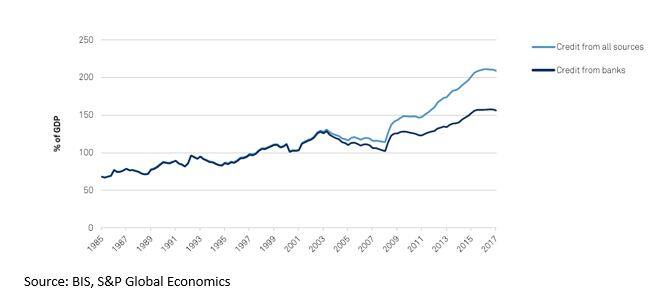

Massive investment-led growth witnessed in first decade of the 21st century majorly contributed to the lengthiest credit cycle, which is showing signs of tapering as the country focuses on deleveraging.

According to Bank of International Settlements (BIS), total credit to non-financial sector is about 208 percent of GDP, slightly off from its peak.

China’s credit creation is moving past its peak

After the global financial crises, there has been a remarkable rise in credit from the non-bank sector which rose to 58 percent from 12 percent of GDP. In early days of the financial crises, this was necessitated due to tight control on deposit rates and the need for credit innovation. Various off balance sheet activities emerged like high yield wealth management products came up, where funds were used to essentially purchase loans that banks wanted off from their books.

Implications:

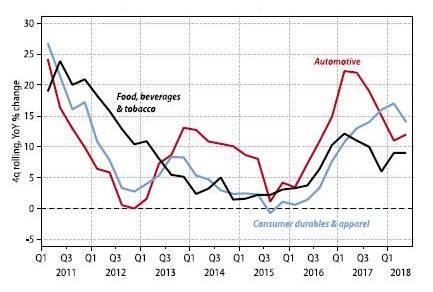

Consumption slowdown: Current deleveraging exercise focuses on clamping various non-banking sources of credit. This has led to contraction in consumption loans as well, which have come from consumer financing platforms, mostly funded by bond issuance.

Not surprisingly, growth in retail sales, particularly in urban areas, has moderated from double-digit to high single-digits. Sector-wise sales data suggests that growth in consumer durables have peaked in Q1 CY18. Automobile sales have decelerated in 2018.

Median sales growth for listed firms (sector-wise) Source: Wind, Gavekal Data/Macrobond

Source: Wind, Gavekal Data/Macrobond

Interestingly, this has an obvious corollary for the Indian consumer discretionary counterpart, where in due to a potential slowdown in NBFC credit, consumption growth can moderate.

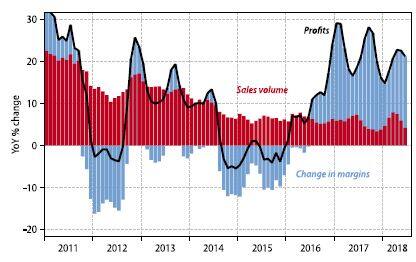

Old economy impact: Supply-side reforms have resulted in a cut down in excess capacity. Deleveraging ensured limited capacity addition elsewhere, resulting in moderation in volume growth. A check of components of the industrial profit cycle suggest that profit growth was mainly contributed by margin expansion and not volumes. Margin expansion itself was a result of favorable supply-demand balance domestically and elevated material prices worldwide.

China’s industrial survey profit cycle (three months moving average)

Source: CEIC, Gavekal Data/Macrobond

Brake in effort: Fed policy cycle and trade war

China’s effort towards economy rebalancing, deleveraging and supply-side reforms have been programmed for a gradual slowdown (soft landing), avoiding the debt trap. As per S&P Global Ratings, consistent improvement was noticed in China Inc’s credit metrics. However, there is a likelihood that deleveraging trend would pause. One of the reason is, on account of slowdown in investment and consumption, industrial earnings growth is likely to contract further.

Further, recent political and economic threats from the US has also thrown a spanner.

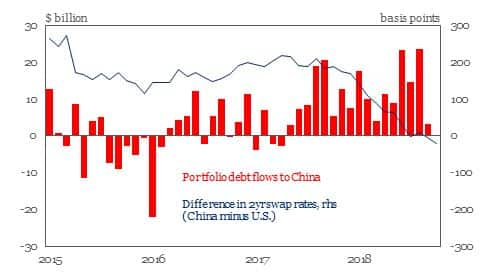

Consistent positive macro data from the US and Federal Reserve’s hawkish stance has been instrumental in reversal of portfolio flows from China and other emerging markets to the US.

Portfolio debt flows to China versus China-US rate differentials

Source: IIF, Bloomberg

Source: IIF, Bloomberg

As far as the trade war is concerned, while manufacturing sector’s share of exports as percentage of sales is around 10 percent in Q2 (from 18 percent in 2008), implication is more indirect. Impact of a trade war is expected to be felt across the supply chain.

Pause or partial reversal in various policy stancesImplications of domestic slowdown and geo-political situation can be observed in loosening of both fiscal and monetary policy. While the government had announced a spending plan (1.35 trillion yuan) for infrastructure projects, People’s Bank of China has enhanced liquidity injections, so as to increase lending to small scale industries. Banking regulator has also signaled taking off some constraints from the off-balance sheet financing.

Likewise, a relaxation in supply-side reforms cannot be ruled out. If it happens, global sectors (metals, chemicals) which benefitted from Chinese supply-side reforms may have to tread cautiously.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.