Anubhav Sahu

Moneycontrol research

Alufluoride reported another stellar quarter as it progresses into a new contract cycle and demand outlook improves. While the capacity expansion plan has been slightly delayed, order pipeline and a potential ramp-up in utilisation makes the prospects of topline growth appear promising. Operational efficiency measures could also boost future earnings.

Q1 update: Surge in sequential sales

Source: Company

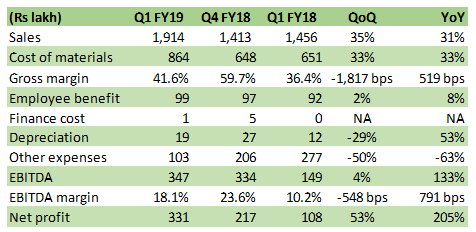

Q1 FY19 sales rose 31 percent year-on-year (YoY) on the back of higher sales realisation and inventory gains. While the plant is operating at full utilisation and produced around 2,000 tonne, aluminum fluoride sold was about 2,700 tonne, aided by spot selling opportunities. Other income jumped significantly (Rs 10.2 crore versus Rs 0.2 crore YoY) as the investment portfolio was liquidated for funding its capacity expansion plan.

Gross margin improved YoY but declined sequentially partly due to expensive purchase of raw material (silicic acid) as sourcing from adjacent fertiliser complex remains challenging.

Margin pressure was partly offset by lower power and fuel costs (12.8 percent of sales versus 14.7 percent in Q4 FY18) as the management focused on higher share from captive power plants.

Expansion schedule delayed by two monthsVenkat Akkineni, Managing Director of Alufluoride, said its capacity expansion plan (4,500 tonne vs current capacity of 7,500 tonne) has been delayed by a couple of months due to which its operationalisation may spill over to Q2 FY20. This extension is mainly due to delay in sourcing of raw material from Coromandel International as its new capacity for phosphoric acid production would be available with a delay of 1-2 months.

Better demand visibility and improving margin profile

Based on the latest quarterly update, estimates for new contract cycle and inputs from the management, we have tweaked our financial projections. Current capacity is fully utilised and the management has raised its sales guidance to about 8,600 tonne (earlier 8,000 tonne) in FY19 before benefits from capacity expansion accrue in FY20. On the domestic front, the company has a strong order pipeline/contracts from major aluminum players such as Hindalco Industries and Vedanta, while smelters from the Gulf have also evinced interest for long term supply of aluminum fluoride.

Taking account of the delay in expansion plan we have moderated our FY20 sales growth expectation . On the operating margin front, we continue to expect improvement on mainly two counts. One, the company’s new plant would have better operational efficiency. Two, it is in the process of installing three solar power plants (around 3 MW) which shall take care of 90 percent of the electricity requirement (including new capacity). The management expects about five percent of operational cost savings due to the above measures.

The balance sheet remain strong and capacity expansion is funded through internal accruals. However, additional debt raising would be required for solar power projects towards fiscal end.

Source: Company, Moneycontrol Research

Near term earnings growth priced in

Improving growth outlook and better-than-expected quarterly result is reflecting in the stock's performance. The stock has more than doubled from its lows in July and moved 41 percent from the time we initiated coverage in December last year.

At present, the stock is trading at 17 times FY20e earnings and at an enterprise value of 8 times estimated EBITDA, which is at a premium to valuation multiples for the non-ferrous sector.

Though the company deserves some valuation premium being the major domestic supplier of aluminum fluoride and also because they are unaffected by sourcing and pricing challenges of fluorspar, investors should wait for some consolidation to accumulate.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!