IndusInd Bank delivered another quarter of predictable high quality earnings giving investors another reason to cheer at the beginning of the earnings season. A strong growth in low-cost deposits drove margin stability despite the bank stepping up its presence in the competitive corporate lending business. Its asset quality showed no signs of stress and fee income growth was decent. While the bank awaits meaningful recovery in the retail business in the second half of the fiscal, it is also gearing up to acquire Bharat Financial, which the management feels would be margin accretive from day one.

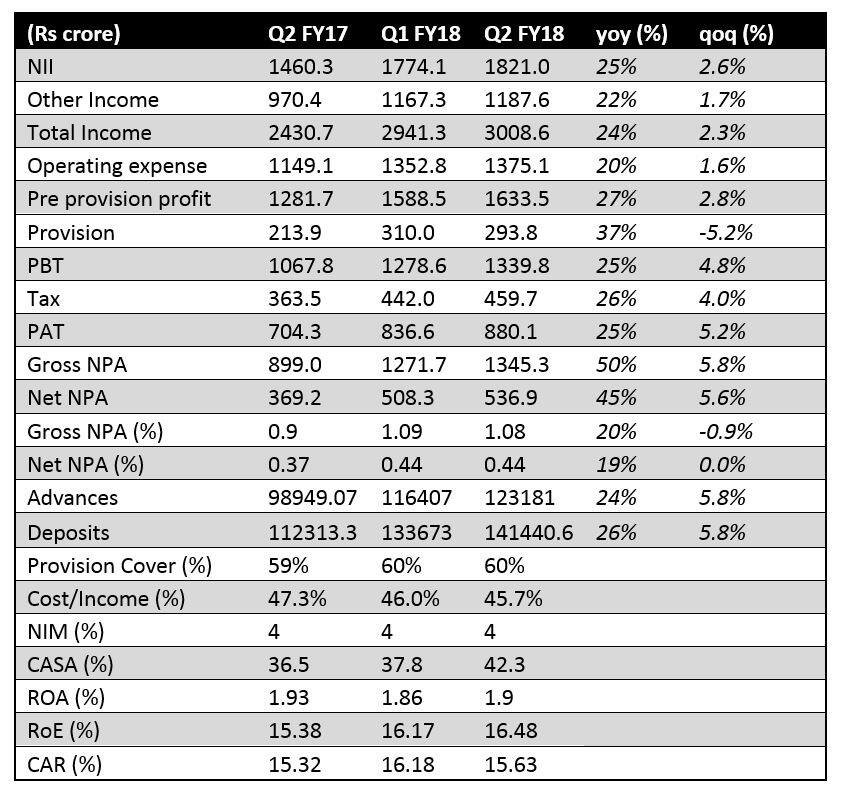

Results at a glanceIIB reported 25 percent growth in profitability driven by a similar growth in net interest income (NII (a difference between interest income and expense). The 14 percent growth in advances and stability in net interest margin aided the performance.

While the overall non-interest earnings grew by 22 percent, core fees showed a better traction at 23 percent aided principally by the distribution of financial products.

What stood out in the number is a well thought-out execution strategy.Building a solid liability franchise to take on the competitionBusiness parameters were impressive with overall advances and deposits growing by 24 percent and 26 percent, respectively. The bank has 3 percent share in incremental deposits and 4.9 percent share in the incremental credit.

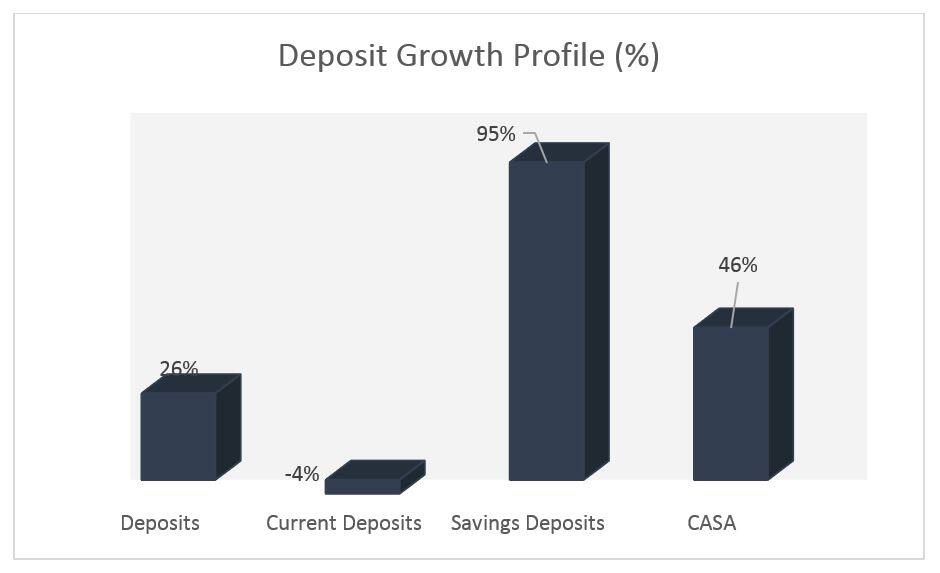

What stood out in the quarter was the healthy growth in low-cost deposits – especially savings deposits that took the overall CASA to 42 percent beyond the bank’s own internal target. Maturing of branches and gains in government businesses have principally contributed to this success.

The strength of the liability explains the steady stride in the asset side without impacting margin. For instance, while the yield of advances has fallen by 26 basis points, cost of deposits have also fallen by a similar magnitude thereby lending stability to margins.

On the asset side, while the growth is now being driven by the corporate book that showed a growth of 26 percent as opposed to the 22 percent growth in retail, the bank attributes the same to market share gains, a phenomenon that is here to stay as public sector banks continue to vacate the market.

Asset quality comfort continuesThe headline NPA (non-performing assets) numbers were stable and there was a sequential decline in slippages as well. While the bank has exposure to 6 cases in the next round of bad asset resolution under NCLT (National Company Law Tribunal), it has provided an incremental Rs 36 crore for the same thereby taking the provision cover for these accounts to 65 percent. The restructured book stands at a minuscule 0.16 percent and ARC book at 0.3 percent. We feel IndusInd has negotiated the worst of the NPL cycle with ease and looks set to expand business at the expense of NPA-laden competitors.

The value accretive Bharat Financial Inclusion dealThe long-awaited deal to acquire Bharat Financial Inclusion (formerly known as SKS Microfinance) is likely to see the light of the day soon. While it is premature to comment on valuation, the deal certainly should benefit the bank’s shareholders in the short as well as long-term.

The bank plans to offer the entire gamut of the asset as well as liability products to this clientele and expands its reach in the hinterland.

The lower cost of funds of a bank is a significant boost to margins on a high yielding asset book of microfinance. In addition, the risk weight of these assets is lower at 75 percent in a bank compared to 100 percent under the NBFC (non-banking finance company). The excess priority sector loans should enable the bank to get active in the priority sector lending certificate market thereby earning a decent commission of 1.5-2 percent without having to let go of these assets from its books.

So the bank is eagerly eyeing the “Bandhan opportunity” (a very successful competitor bank catering to the bottom of the pyramid) from the deal. The management sees early signs of traction post the twin disruptions of demonetisation and GST implementation. The second half of the fiscal should see a higher growth in the retail book that should support earnings. Finally, the acquisition of Bharat Financial will add one more feather to IndusInd’s cap.

The valuation of the stock at 3.8x FY19 book might look optically expensive, but investors should look at the bank for the pristine earnings quality coupled with market share gains and earnings expansion that lie ahead.

For more research articles, visit our Moneycontrol Research Page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.