Jitendra Kumar GuptaMoneycontrol Research

The tug of war between the bankers and the acquirers of the steel assets is intensifying each passing day. The share price of two much discussed steel assets - Bhushan Steel and Monnet Ispat -- have moved up swiftly which has attracted investors hoping to be part of their turnaround stories.

While an immediate resolution of these assets and acquisition by a serious player could definitely help revive these companies, will investors make money? The question needs to be seen in the light of the prospective acquisition of the deal.

Crystal ball gazing

Moneycontrol presents a scenario to see if Monnet Ispat and Bhushan Steel are worth their mettle. Currently, the value of assets in both the cases comes out to be lower than the debt in the books, which essentially means there is no value left for the equity shareholders. The value will only be created through a structure that benefits equity investors.

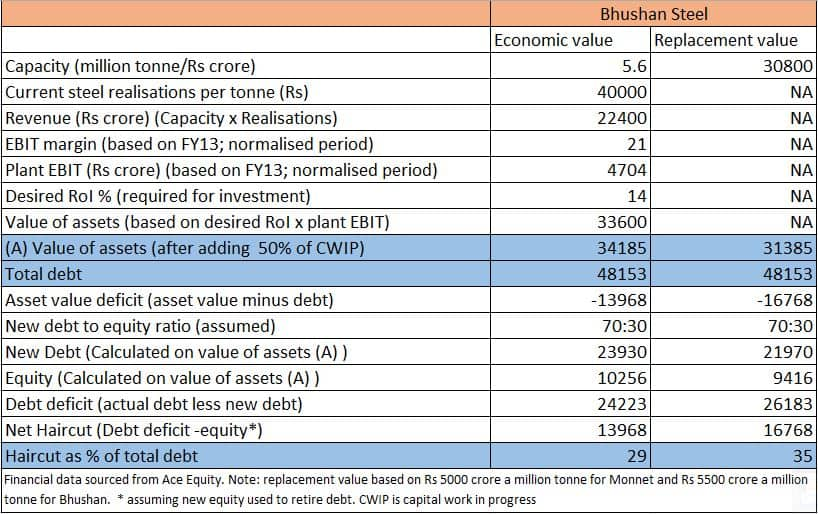

Bhushan Steel

Bhushan Steel, which is into the value added steel earning relatively higher realisations for every tonne of steel, has capacity of 5.6 million tonnes. Based on replacement value at Rs 5,500 a tonne, this capacity is worth Rs 31300 crore and based on economic value (ability to produce profits at 14 percent rate of return) it is worth about Rs 34000 crore.

In both the cases (economic value and replacement value) value of these assets is far lower than total debt of Rs 48000 crore (FY17) indicating there is nothing left for equity shareholders of the company.

To make it commercially viable so that equity investors can make money at current market price, the lenders will have to take a certain haircut. Assuming a new buyer comes at debt-to-equity of 70:30 ratio at which it could be financially viable, banks will have to take hair cut of about 30-35 percent (as discussed in the illustration). The value of equity will be close to Rs 10,000 crore. To infuse that much money, the company will have to issue fresh shares resulting in a huge dilution to the existing equity.

In this structure assuming a project RoI (return on investment) of 14 percent, there is a reasonable possibility of profit approaching around Rs 1300-1400 crore, which translates to a price-to-earnings multiple of about 8 times (on fully diluted earnings) at the current price, which is quite reasonable.

However, calculations defer depending on the amount of the final haircut taken by the banks and price at which the new shares are issued. Higher haircut and low dilution (as against what we assumed in the illustration) will mean more bucks for existing investors. Nevertheless, generating a good return would also be in the interest of buyer or the acquirer, if they can sweeten the deal; it would also benefit existing shareholders. Notably, without the deal today there is no value even if the market is quoting its shares at Rs 65 a piece or market capitalisation of Rs 1474 crore.

Monnet Ispat

Monnet Ispat is relatively small with the annual production of capacity of 1.5, which is worth about Rs 10,000-11,000 crore including 50 percent of capital work in progress of Rs 5585 crore reported in FY17. Here as well, the debt at Rs 12,262 crore is higher than the value of assets (Rs 10000-11000 crore) leaving almost nothing for the equity shareholders.

During financial year 2017, the company incurred a loss of Rs 364 crore before interest cost of Rs 1141 crore. This essentially means that banks will have to take a haircut to the extent that the acquirer can make money on his/her investment.

Our calculations suggest a haircut of about 11-16 percent and an infusion of about Rs 3000 crore by the acquirer based on new debt-to-equity ratio of 70:30.

As indicated in the illustration, with this structure, profits work out to around Rs 430-460 crore and fully diluted (after fresh issue) EPS of Rs 4 per share working out to a price-to-earnings of 8-9 times at the current price.

Effectively, in this case as well, today there is no value left for the equity shareholders. Investors will only make money if the banks take a haircut and fresh issue of shares is value accretive in the sense that it leads to lower dilution. If the number of shares issued are lower it would result in higher EPS and thus better return for equity shareholders.

The timing of these investments and valuation ratios, too, will have a role to play. Today, the price-to-earnings multiple works out to 8-9 times but if the market is able to give higher multiple, which is quite possible, because of the visibility, stability, stronger steel cycle, industry consolidation, greater pricing power, better return ratios and synergic benefits of businesses, stock returns could be even higher.

Key risks: assessing such turnaround companies often requires information beyond the scope of the balance sheet. Acquirers of these assets are relatively better equipped as they can physically verify assets, undertake forensic audits, use industry network and hire consultants and valuers as against secondary market investors. Last but not least if the companies are not acquired as speculated by the market that could cause a permanent loss of capital.

For more research articles, visit our Moneycontrol Research Page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!