Bank credit growth rebounded in double digits in the quarter ended March 2022 as businesses gradually returned to normalcy after two years of a lull, aided by lower interest rates, data showed. However, it also revealed that the lower interest rates have adversely impacted the interest earnings of banks.

During Q4FY22 (January-March), the spread between banks’ weighted average lending rate (WALR) for outstanding loans and weighted average domestic term deposit rate (WADTDR) reduced by 11 basis points (bps) year-on year (y-o-y) and stood at 3.71 percent in March.

This was on account of banks reducing interest rates on loans faster than deposits, domestic rating agency CARE said in a report dated June 17.

The average spread between lending and deposit rates of state-led banks fell by 9 bps YoY to 3.24 percent in March 2022, while private lenders’ spreads declined by 3 bps to 4.52 percent in the same period, it added.

Source: CARE Ratings

Source: CARE Ratings

With expectations that the Reserve Bank of India (RBI) will raise the repo rate more in view of a higher annual inflation forecast, spreads are likely to rise going ahead, analysts said.

“Usually, in a rising interest rate environment, banks tend to see an increase in their margins as assets tend to get repriced faster than the liabilities. However, competitive pressures could subdue the movement if banks were to tweak the credit risk premiums that they charge,” says Karan Gupta, director of financial institutions at India Ratings & Research.

Even as the spreads remained under pressure during the January-March period, lenders’ net interest margin (NIM) improved by 17 bps YoY to 2.8 percent in Q4FY22 due to higher growth in retail loans and improvement in asset quality, CARE Ratings said.

The NIM of state-owned lenders improved by 20 bps YoY to 2.4 percent during the January-March quarter while private banks’ NIMs improved by 8 bps YoY to 3.6 percent in the same period.

Asset quality

Lenders reported an improvement in asset quality in Q4 on account of lower slippages and higher recoveries and upgrades.

Banks’ gross non-performing asset (GNPA) ratio improved to 6.1 percent as of March 31 from 7.6 percent as on March 31, 2021, and 6.7 percent as of December 31, CARE Ratings data showed.

Credit cost, or capital set aside for potential bad loans, declined to 0.7 percent in Q4FY22 from 1.4 percent last year due to an improvement in the asset quality position and banks’ assessment of lower incremental provisioning requirements, it added.

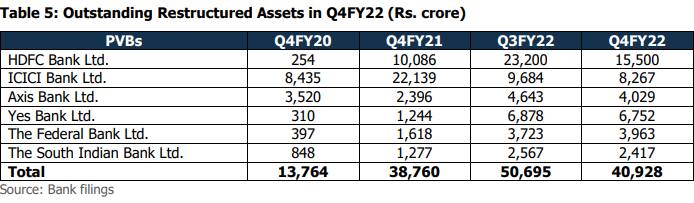

State Bank of India (SBI), the country’s largest lender, reported its outstanding restructured advances at Rs 30,960 as on March end, lower than Rs 40,000 crore as on December 31, CARE Ratings said. Private sector major HDFC Bank’s restructured loans, on the other hand, stood at Rs 15,500 crore as of March end as against Rs 23,200 crore a quarter ago.

Source: CARE Ratings

Source: CARE Ratings

On an overall basis, banks’ provisions declined by 42.6 percent on year to Rs 0.4 lakh crore in January-March, the lowest in the last two years, due to an improvement in asset quality and thanks to holding a buffer for provisions.

Slippages arising from loans extended under the central government’s emergency credit line guarantee scheme (ECLGS) and movement of loans in the restructured pool of advances will be a key monitorable in FY23, analysts said.

Opex rise, muted treasury income continue

Even as lenders’ credit growth and asset quality metrics continued to improve in Q4, higher operating expenses and muted treasury income hindered the overall performance of banks.

Non-interest income of public sector banks (PSBs) fell 28.9 percent on year due to a rise in government bond yields, while private banks’ other income fell 1.3 percent on year to Rs 26,012 crore during the same period.

Another trend that sustained its upward momentum in Q4 was the rise in operating expenses as lenders upgraded systems to support their digitalisation push.

The operating expenses of banks rose by 5.1 percent on year to Rs 96,741 crore in Q4FY22 on account of an increase in expenses related to digitalisation, higher commission fees and marketing expenses.

“Operating expenses are likely to rise as banks will chase higher loan growth and will need to invest heavily in the right people for the same to achieve the growth target,” Gupta said.

“Income from treasury is likely to remain muted with sharp movement in interest rates. However, banks are trying to arrest the fall, having reduced the modified duration of their investment portfolio,” he added.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.