Banks, especially state-run banks, are seeing increasing pressure on their net interest margins (NIMs) which bankers attributed to a mix of factors including a low interest-rate regime, high provisioning on stressed assets and the lack of meaningful credit growth.

NIM is the difference between interest earned on loans and interest paid on deposits.

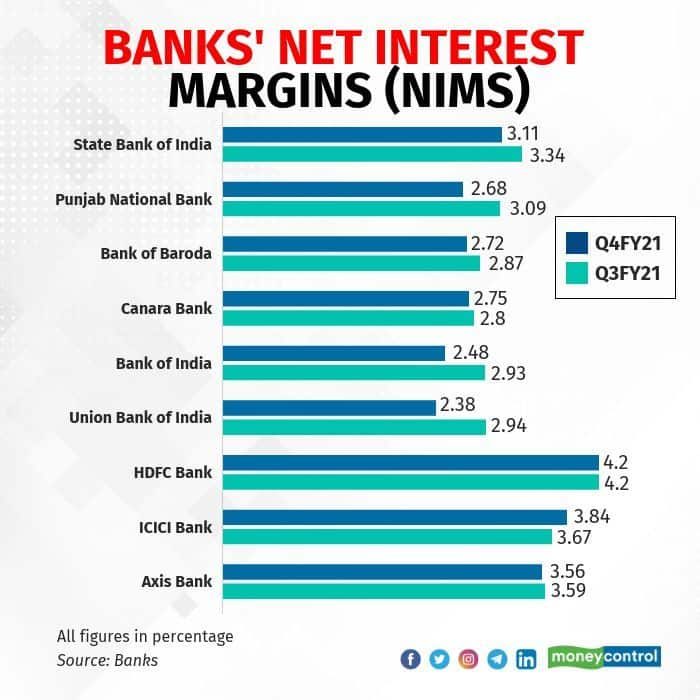

A Moneycontrol analysis of the margins of nine top banks showed that public sector banks have seen a clear decline in NIMs between the October-December and January-March quarter of FY21. NIMs fell up to 56 basis points (bps) on a sequential basis. A basis point is one-hundredth of a percentage point. In comparison, private banks either saw NIMs remain stable or increase.

In a report dated May 2, Nomura analysts Nilanjan Karfa, Amit Nanavati and Tanuj Kyal said that the average spread for private banks and public sector banks stood at 4.6 percent and 3.2 percent, respectively. Spread refers to the difference between the average rate of interest on loans and that on deposits.

“The sharp divergence in spreads is mostly reflecting on the higher share of higher-yielding loans for private sector banks than SOE (state-owned enterprise) banks,” Nomura said.

Some banks have said low interest rates and poor credit growth are the reasons behind margins falling. “The primary reason for our net interest margin to see a decline is a fall in yield on advances, which was more than the fall in our cost of deposits,” AK Das, MD & CEO, Bank of India, said on 4 June.

Das added that another factor was muted growth in advances. Bank credit growth has been languishing in the five-six percent range for a year now, which means banks have fewer opportunities to earn interest income.

“Slowly but surely, we are moving towards a regime where we have to operate within a lower margin because a lot of transmission is happening. That may bring us in line with our foreign counterparts who operate within a smaller margin,” Das added.

Das referred to the directive of the central bank to link new loans to retail and small enterprise borrowers to an external benchmark, which came into effect in April 2019. As a result of that regulation, much of the new loans in the system are priced over the repo rate, which has fallen by 115 bps since March 2020.

High provisions hurt

Analysts said there are also other factors at work. “NIMs have been hit also because banks have been making a lot of accelerated provisions in anticipation of new stress emerging,” said Madan Sabnavis, Chief Economist, CARE Ratings. Of course, stable interest rates are also playing a part because they limit the gains banks make on sale of government securities, Sabnavis added.

Public sector banks may also be getting affected harder because of their presence in international markets where loan yields are low. The management of Bank of Baroda, which has historically had a significant overseas presence, told analysts after the March quarter results that NIMs are under pressure in the international book. “We are trying to focus on geographies where we actually are making very good money,” said Sanjiv Chadha, MD & CEO, Bank of Baroda. The bank expects to see the trend of negative growth in international loans continuing.

Even though private banks have been able to manage their NIMs better, they are having to put in some effort in an environment of excess liquidity. HDFC Bank’s March quarter core NIM remained unchanged sequentially at 4.2 percent. Its Chief Financial Officer Srinivasan Vaidyanathan told analysts after the bank’s results that its average liquidity coverage ratio was 138 percent.

“The excess liquidity position of the bank impacts current NIM 10 basis points to 15 basis points or so. This drag was offset by monetising some of the investments in the form of trading gains, which we have described in the past quarters,” Vaidyanathan said, adding that this was part of the bank’s asset liability committee strategy.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.