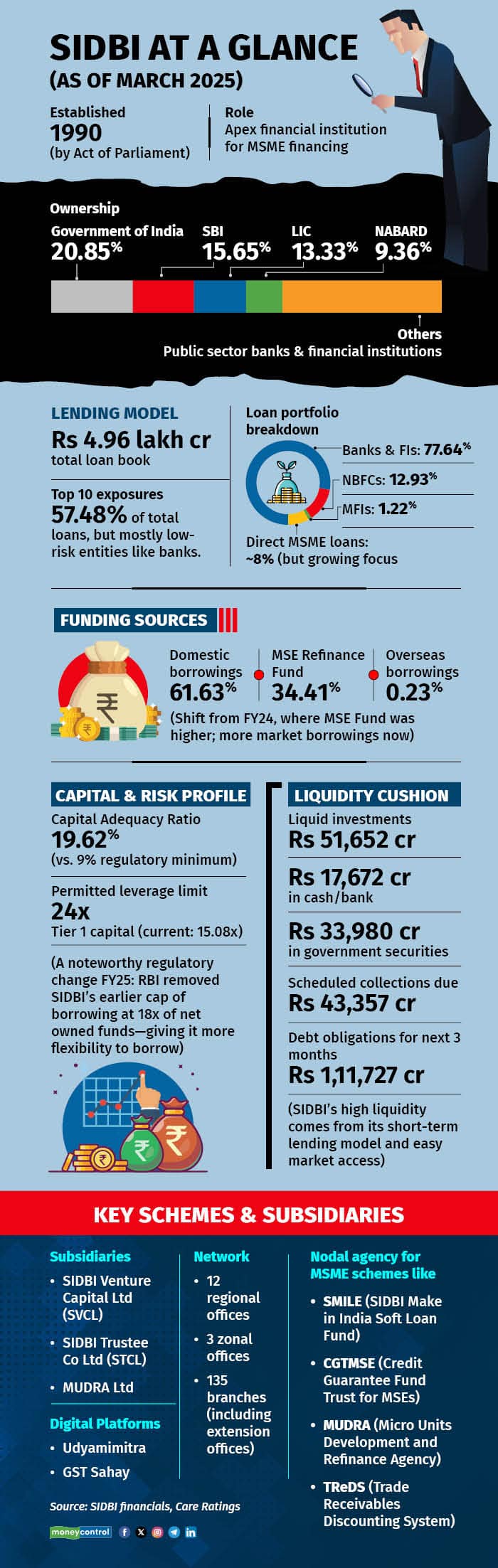

The Small Industries Development Bank of India (SIDBI), a key financial institution for MSME financing, ended the financial year 2025 with striking numbers in India’s financial sector, reporting a standalone net profit of Rs 4,811 crore, nearly 20 percent higher than a year ago. Its total income crossed Rs 38,511 crore, while the loan book expanded to Rs 4.96 lakh crore, marking steady growth in both profit and lending.

On a consolidated basis, which includes subsidiaries such as MUDRA and SIDBI Venture Capital, net profit stood at Rs 5,596 crore, up around 16 percent from Rs 4,813 crore the previous year, on a 19 percent higher total income of Rs 40,753 crore.

Among all the numbers, SIDBI’s gross non-performing assets (GNPA), or bad loans stood out, at Rs 183 crore, a mere 0.04 percent of its total loans, while net NPAs were nil.

These figures come from an institution whose primary mandate is to finance the micro, small and medium enterprises (MSME) sector, an area usually seen as carrying higher credit risk, yet, SIDBI’s loan book has remained remarkably clean.

Not a regular lenderOne of the reasons for this lies in the way SIDBI operates. It is not a typical bank that lends directly to small businesses on a large scale, instead, it acts as a refinancing institution, providing funds to banks, non-banking financial companies (NBFCs), and microfinance institutions (MFIs) which then extend loans to MSMEs.

According to its latest financial statements, more than 91 percent of SIDBI’s total loan portfolio comprises such indirect lending. In simple terms, most of its loans are to other lenders, not to small businesses directly.

This business model means that SIDBI’s borrowers are usually well-established, regulated financial institutions, including government-owned banks. These entities tend to have stronger balance sheets and better credit profiles. As a result, the credit risk faced by SIDBI is much lower than that faced by lenders operating directly in the MSME segment.

SIDBI’s lending is also structured to limit risks in other ways. Its refinancing loans typically have shorter durations, often between one and one-and-a-half years. These loans are regularly repaid and renewed, allowing the bank to monitor risks closely and keep its exposure limited.

SIDBI’s largest exposures are highly concentrated but involve mainly low-risk entities. As of March 2025, SIDBI’s top 10 borrowers accounted for about 57 percent of its total loans, though these were largely banks and top-rated NBFCs.

SIDBI operates with very low overhead costs, with operating expenses of Rs 1,430 crore in FY25, which translates to a cost-to-assets ratio of just 0.26 percent.

Its operations are focused mainly on wholesale lending, requiring fewer staff and limited physical infrastructure compared to banks with large retail loan portfolios.

How SIDBI funds its operationsSIDBI funds its lending activities through a mix of market borrowings and government-backed schemes. One of its key sources is the MSE Refinance Fund, under which it received Rs 50,040 crore in FY25. Along with this, it also raises money through bonds and other borrowings.

However, market borrowings are gradually becoming a larger part of its funding base. This pushed up its average cost of funds to 5.73 percent in FY25, from 5.43 percent the previous year, SIDBI has said.

The reason for this is that interest rates are higher in market borrowings than the concessional government funds it earlier depended on. Therefore, SIDBI had to raise its lending rates accordingly to cover these costs and maintain profitability.

Lending rates increased, with the yield on advances rising to 7.03 percent from 6.86 percent, per Care Ratings analysis. This essentially means that on an average, SIDBI earned more interest from its loans in FY25 than the previous year. This yield represents the average interest SIDBI earned from its loans during the year.

This squeezed its net interest spread/margins slightly, narrowing to 1.3 percent from 1.43 percent a year ago. Despite this, SIDBI maintained its profitability due to its low operational costs and stable loan book.

Surge in networthSIDBI’s capital position remains strong, with a tangible net worth of Rs 33,999 crore as of March 31, 2025, up from Rs 30,040 crore a year earlier. It reported a capital adequacy ratio (CAR) of 19.62 percent, comfortably above regulatory norms, and holds additional provisions of Rs 3,657 crore on standard assets.

A proposed capital infusion of Rs 5,000 crore by the central government is expected to further bolster its balance sheet.

SIDBI’s liquidity remains comfortable as of March 2025, holding Rs 51,652 crore in cash, bank balances, and government securities. Given its short-term loan profile, most of its borrowings also have similar maturities, helping it manage cash flows efficiently.

A new pattern of direct lending

A new pattern of direct lending While SIDBI's lending model is mainly indirect, it has been gradually increasing its direct lending to MSMEs, which now contributes around 8 percent of its total loans. This includes long-term loans, working capital solutions, and bill discounting, particularly aimed at small businesses that may otherwise be left out of formal banking networks.

Although the direct loan book is small, it has higher credit risks compared to refinancing operations. However, its overall impact on asset quality is limited.

As per CARE Ratings, refinancing to banks and financial institutions formed 77.6 percent of its loan book as of March 2025, followed by NBFCs at 12.9 percent and MFIs at 1.2 percent. Refinancing to NBFCs and direct lending grew during the year, while allocations to banks and MFIs slightly declined.

Low GNPA, margins under pressureSIDBI’s GNPA ratio remained exceptionally low, inching up marginally to 0.04 percent from 0.02 percent a year earlier. In absolute terms, bad loans stood at Rs 183 crore, entirely provisioned for.

SIDBI also remained active in managing its stressed loans. During FY25, it sold Rs 153 crore of bad loans to asset reconstruction companies, which had already been fully provisioned.

Credit costs rose slightly to 0.43 percent in FY25 compared to the previous year. However, its low operating expenses - at 0.26 percent of assets – has supported profitability. Return on assets (standalone) stood at 0.89 percent, marginally higher than 0.87 percent last year.

Analysts noted that while SIDBI’s lending margins narrowed during the year, profitability remained stable and is expected to be driven more by operating expenses and credit costs than by spreads going forward.

BackgroundSIDBI was established in 1990 as a wholly-owned subsidiary of IDBI. Over time, IDBI diluted its stake, and as of March 31, 2025, SIDBI’s majority shareholding rests with the Government of India (20.85%), State Bank of India (15.65%), LIC (13.33%), and NABARD (9.36%).

SIDBI has three wholly-owned subsidiaries - SIDBI Venture Capital (SVCL), SIDBI Trustee (STCL), and MUDRA.

MUDRA, set up by the government through a statutory enactment, is tasked with refinancing and supporting institutions that lend to micro and small enterprises across manufacturing, trading, and services. It works with state and regional partners to fund last-mile microfinance lenders.

The institution operates through a network of 12 regional offices, 3 zonal offices, and 135 branch offices, including extension branches, across India.

SIDBI’s importance also lies in the fact that it is not just a lender, but a nodal agency for MSME-related government schemes. Over the years, it has been tasked with executing and anchoring some of the most significant programs such as the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE), SMILE (SIDBI Make in India Soft Loan Fund), MUDRA, and Trade Receivables Discounting System (TReDS).

It also operates digital platforms like Udyamimitra and GST Sahay to simplify access to credit for small entrepreneurs, especially in remote and underserved regions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.