Shishir Asthana & Jitendra Gupta

Moneycontrol Research

Value investing is generally termed as contrarian investing. Not many can withstand the heat of staying aloof when the market is going crazy around them. It needs a cool head, a strong discipline and complete faith in one’s abilities to be a contrarian investor.

Ace investor Kenneth Andrade is all this and much more. With nearly 27 years of experience in the equity markets, 15 of them in managing money and staying at the top of the table, Andrade surprised the market by quitting his job as the chief fund manager with IDFC Mutual Fund and managing money on his own.

With an enviable track record of a compounded return of 22 percent for a period of 10 years, Andrade was bitten by the entrepreneur bug. He decided to launch his own portfolio management scheme (PMS) fund Old Bridge Capital. He has now opened up an Alternate Investment Fund (AIF) with an aim to garner Rs 400 crore.

With a passion for investing that can be seen in his constant search for next multi-bagger, Andrade also has an ear for music. He loves reading and likes to go on long drives in his electric car.

In a free-wheeling interview with Shishir Asthana and Jitendra Gupta of Moneycontrol Research, Andrade shares his his investment philosophy and the learnings he gained from the journey.

Q) How did you enter the investing industry?

Andrade: Well, I used to do some small investments in college and post my graduation took up a job with the investing magazine Capital Markets in 1990-91. I took up freelance assignments with a lot of other publications, and a few brokerage houses. In 1997, I also had a stint with television with Nimbus Communications which was the only one with a program on markets then.

I moved on the buy side with Kotak Mutual Fund in 2002-03 just after the tech collapse. I took care of a small portfolio called Kotak Energy. Towards the end of 2005, we launched a mid-cap fund for which we raised around Rs 600 crore. This was a sizeable amount in those days. Until that time the entire size of Kotak Mutual Fund was around Rs 800 crore.

My stints with Standard Chartered and IDFC Asset Management for nearly a decade helped me streamline my investing process. Thereafter, I started Old Bridge Capital Management in 2016. We made our first investment in September 2016. Today, we have close to Rs 1,500 crore in asset under management (AUM).

We are now launching a public market focused alternative investment fund (AIF).

Q) Has your investment philosophy changed over the years since the time you started managing funds at an asset management company to the present format?

Andrade: There has not been a tremendous change, it has happened in the sub-conscious. In all years of managing money qualitatively, you stop making mistakes. You tick off the wrong ones and everything you do incrementally adds up to your improvement.

ALSO READ: Companies with 9% return on equity are good bets: Kenneth Andrade

Q) You have been largely a mid-cap fund manager. How come you have an all-cap fund in Old Bridge?

Andrade: Back in 2000, we had a tech boom. It was a bubble economy. Any company that had anything to do with technology did well. This also holds true for 2008, everything that had to do with any form of infrastructure did well. We had commodities — cement, a contracting company, an engineering company — in our portfolio then. We called it diversified, but it was one pipeline of companies that had to do with the capex cycle.

To put it differently, I like financial bubbles. But that is the end point of it all. So, we need to identify when it actually starts. Bubbles happen in parts of the economy, they happen in sectors. Technology was one such sector. Tech companies catering to the capex cycle were part of the bubble. It happened briefly in the pharmaceutical sector as well.

It happens in a corporate which has a rising profit boom. The challenge is how do you recognise the rising profit boom. If you are early in the cycle you catch the entire cycle because eventually, everyone will participate in the boom.

So those are cycles that keep on happening in the market. I believe that if you can capture the cycle in the early stage you gain.

Q) How do you identify these companies or sectors in the early stage of the cycles?

Andrade: Rather than sectors I prefer to look at industry verticals and try to figure out which will do well. In 2013, it was very simple — the small-cap index was hitting its all-time low and companies were available at distress valuation. Around 10 percent of the companies were making profits. Everyone was exiting these companies when the market price showed that the risk was already priced in.

That was the time when we launched a fund in the mid-cap or the small-cap space called the IDFC Equity Opportunities Fund. Next three years it performed brilliantly, in fact, we paid back the entire capital as dividends.

That is how we narrow down on verticals. It operates at both the extremes. What helped me out in 2008 is we stayed out of infrastructure companies. We had a very conservative portfolio of consumer-specific companies.

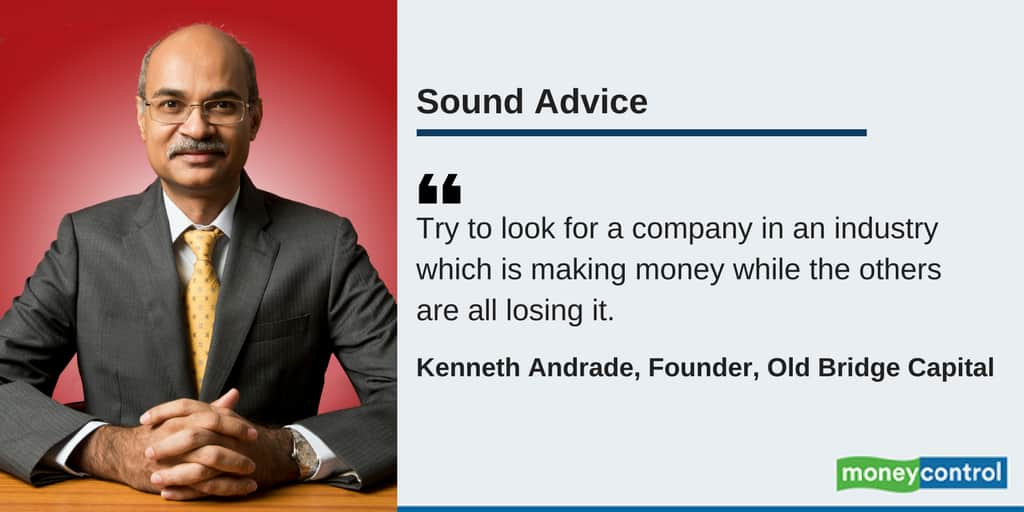

How we do it? The process is very simple — try to look for a company in an industry which is making money while the others are all losing it. So, when the industry comes back you are with the best company. It happens in sugar all the time.

It’s not easy to find them. I could only find it in sugar. I was also possible to spot them in the fertiliser chain.

Q) Are there any companies that are available at distressed valuation, especially as you will be raising money through the new AIF?

Andrade: You will find something that is good at all points of time. We have a pipeline of stocks that we like ready to invest at all points of time. We like media companies, but they have not given any returns over the last one year. The underlying structure of the industry itself is deteriorating. The spend by corporate India does not exist.

Q) When you buy a company at a low valuation and sell it at fair value, you are essentially playing the valuation arbitrage. How do you decide when to sell?

Andrade: You have to give some time for these things to evolve. I have bought a stock at the same price for three years. This was Bosch. Nothing happened to the company between 2007 and 2009. But with every year that passed the company became more attractive because the denominator (earnings of the price to earnings ratio) continued to grow even though the price remained static. So you have to have the patience to go through the entire cycle.

It’s like one year has gone since I have bought media nothing has happened to them. I don’t know if anything will happen to them. But I am willing to take the chance because I know that valuations are in my favour. The environment will expand itself. The derivative of this expansion will come to these companies bottom line.

Q) What attracts you to the agriculture space?

Andrade: My job as a fund manager is to buy capital efficiency in my fund. So, if I remove the industry from the equation what is my cash flow yield, what is my investing yield.

Let me put it little differently. For you, to compound returns you need the price-earnings ratio to expand and at the same time, you need the denominator (earnings) to expand. If I get a stock at a price-earnings multiple of 30 times I would like it to go to 40 times or 50 times. But, I would rather buy them in the range of 10 to 30.

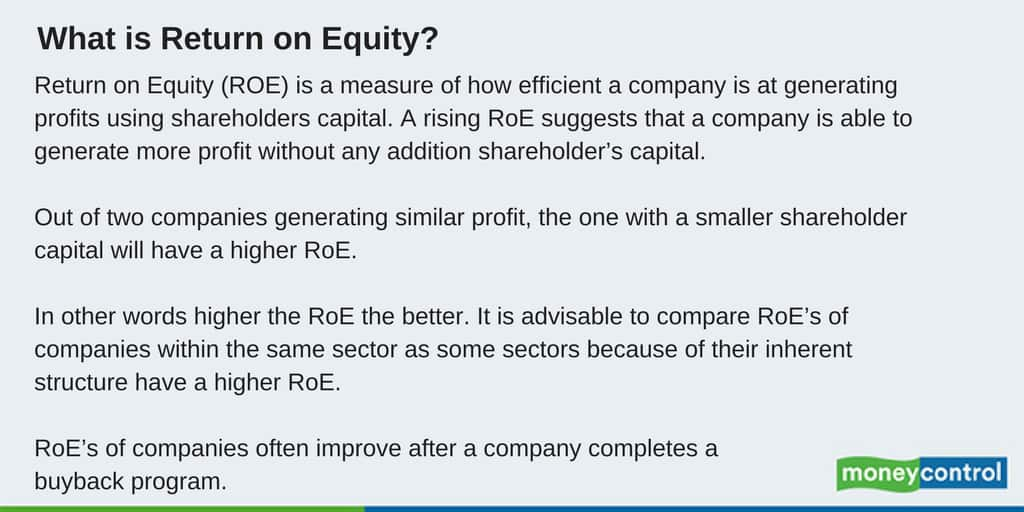

I like to buy companies that are making profits. I define companies that are making profits as the ones that are making 9 percent return on equity (RoE). Even if it making 9 percent ROE, it is a good business, especially at a time when the rest are losing with that vertical. Because when the cycle turns they are the first off the block.

Q) Is this the only strategy through which you pick up stocks?

Andrade: We keep on searching for opportunities. We like to work on this parameter that only if this one does not throw up opportunities, should we look at others.

Q) Are banks and technology stocks popping up in your search?

Andrade: Banks, not in this cycle. Technology, yes we like a few companies. We have expanded our universe of looking at pharmaceuticals. I want low valuations and I want cash flows.

Q) Are you comfortable sitting on cash if there are no opportunities?

Andrade: We are comfortable sitting on cash, but we rarely do that. We are lucky to have an environment that offers a large universe to work with. I was invested in consumables during the peak of the 2007-08 run. After the market crashed, they were the first to bounce back. That’s when I learned never to hide behind cash in a bear market.

Q) You follow a concentrated portfolio approach of 15-20 stocks. What do you do when you get a new opportunity?

Andrade: Yes, we are happy to have 5-7 percent of our portfolio in one stock at the upper end. Any reason that we see to buy and if the converse is happening we exit. We generally give a long rope to the companies to operate in. If the company is operating in an industry where the macros are deteriorating, there is very little that the company can do. It has to just increase its ability to survive by the day because when the cycle turns it will lead the pack.

I need to be very focused on seeing that everything is right and the balance sheet is not deteriorating. Balance sheet deterioration is the last thing that I can stand. So, we manage business which we know goes through cycles. But in every cycle, the company has to come out on the top. That’s a good company for us.

But if a company is leveraged it cannot come on the top, then it carries a lot of financial risks. Because on the down cycle the leverage hits it.

Now if a new company comes up we evaluate the opportunity with the existing basket.

Q) ROE is one of the parameters that you look at, but the small-cap index has an ROE between 2 and 3 percent which does not fall into the minimum criteria of 9 percent that you have set for yourself. Is there a strict 9 percent rule you follow or a return above the cost of capital that is necessary?

Andrade: That is (Small-cap index) not a fair indicator of the space we operate in. If you look at the BSE 500 the ROE there is between 16-17 percent. In the small-cap index, if you go to their P&L account they have not reached their peak level in net profits. Their all-time high was around Rs 51,000 crore they are still at around Rs 24,000 crore. So, that is where the disconnect in valuations is.

Even in the BSE 500 space, the asset turnover ratio is off its peak offering enough headroom. That is the key — as capacity utilisation improves cash flow comes in that is when we see the denominator improve.

Q) How much importance do you give to meeting company management and studying the market environment?

Andrade: So, knowing the business and the company you invest in is very relevant. The thought process of the management and how it behaves with its stakeholders is key. Stakeholders are not shareholders, but the customers. If the customers are happy and your employees are happy, you have a good company. Then there are other stakeholders and bondholders who count.

Q) Anything in particular that you look at in the management?

Andrade: From the management perspective I like to look at quantitatively. As in management quality is dictated by financial ratios. And if he is not growing with the external capital he is doing a damn good job. So if a company is in an industry which is not growing the management is able to increase market share with the same amount of capital employed, it is a no-brainer. So when the cycle turns and the pricing power comes back this company is going to increase profitability in a bigger turnover and bigger market share.

On the other hand, we have seen what happened in the last cycle was businesses were growing at a 15 percent CAGR (compounded annual growth rate) over 4-5 years. And between 2008 and 2010 capacities that came on stream anticipated growth at 30 percent CAGR. So what we have is a very large build-up of capacity and your capital employed. But your profit continued to grow at a 10 percent CAGR which saw your return on capital and RoE nosedive. And all of that (capacities) came in with debt.

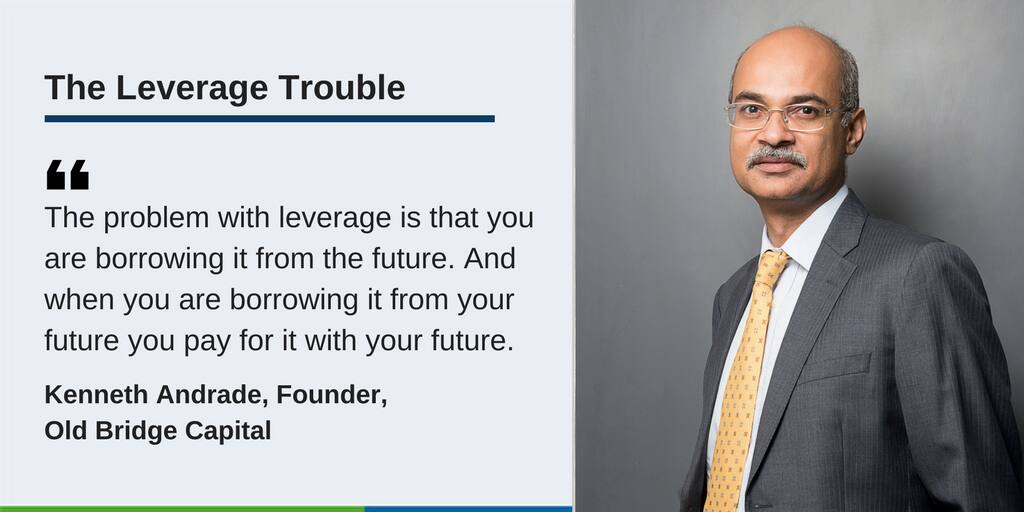

The problem of leverage is that you are borrowing it from the future. And when you are borrowing it from your future you pay for it with your future. Which is why I stay away from significant leverage.

Q) How does gauge that the management will be able to run business cycles well in future?

Andrade: You need to work for a 60 percent strike rate (in stock picking) and you will end up with a 55 percent. We all work for a 100 percent strike rate but we never get that. All you need to do is get 50 percent strike rate on businesses that do well. You have to make lesser numbers of mistakes. You can’t be aiming for the boundary all the time because then you leave your wickets wide open.

You buy companies when the valuations are right. When we looked at Hero Motors (then Hero Honda), it was available at 5 percent dividend yield. The darling of the market was L&T which was at a historically high valuation. L&T is a great company but it was mispriced.

Q) What are the valuation parameter you look at for cyclical businesses?

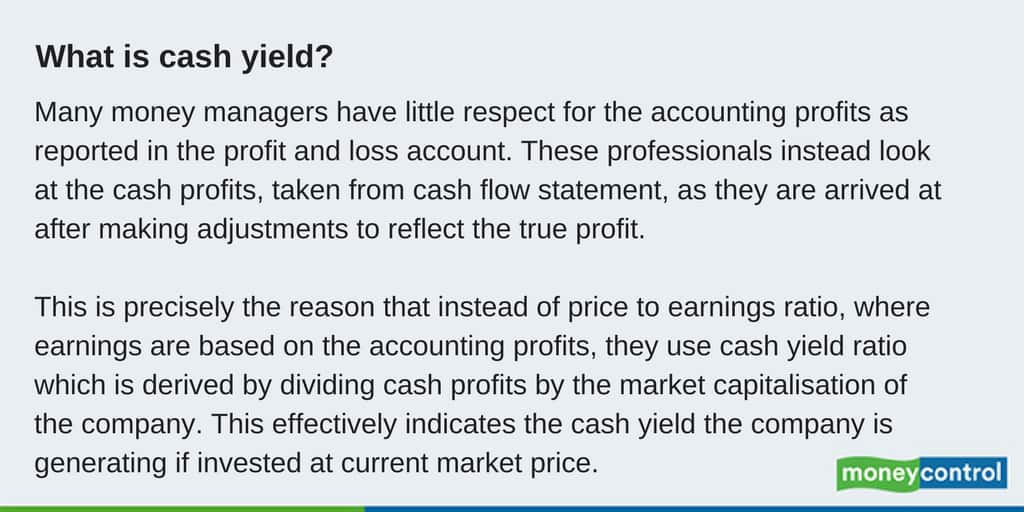

Andrade: We generally look at cash flow to market cap or free cash flow to market cap.

Q) What has been your best pick? Something where your call played out exactly like you thought…

Andrade: I think we got the previous cycle correct. We were out of infrastructure and were not trapped like many others. So we got that call right. For me, that was the inflection point. That was a career change move for me.

There are many companies that kept on coming. I got Page Industries on the table, because I had a Glaxo SmithKline with me and because of that I bought Asian Paints, and because I had Asian Paints I got Bata. All these companies in the consumable verticals were available at a price to earnings of 15 to 18 times. But that is now history.

Q) Any mistakes that you would like to highlight?

Andrade: Plenty, so if you work on a 50 percent strike rate you are bound to make many mistakes. I think I was too early in the cycle for public sector companies in 2012 end when I put together a public sector fund. The idea was not wrong, but I executed it terribly. In hindsight, it was one of my larger mistakes or largest mistake. We did not lose money, we managed index-linked returns but that is not what an investor expects from us.

Q) Is valuation a sufficient condition to exit? Many fund managers exit based on high valuation but concedes the opportunity to compounding.

Andrade: See the largest shareholder with a 10 percent stake in Bajaj Finance exited the company at a price of Rs 2,500 (pre-bonus and pre-split — the current unadjusted price will be around Rs 18,000). He was their largest shareholder. I think PE expansion shakes out a lot of people. It shakes me out too.

Q) Why are you planning an AIF rather than continue with the PMS (Portfolio management scheme) structure?

Andrade: AIF is a simpler instrument. It is an extension of the mutual fund the taxation is the same, it’s a single entity and documentation is easier. From an investing standpoint, nothing changes in terms of strategy.

Q) But will you be able to get new ideas to invest in the current market?

Andrade: There are always opportunities. The challenge is the number of companies will be lower than what it used to be. In 2013 if you had nine companies to invest in you would have made money in eight of them with a success rate of 90-95 percent. In 2017, that ratio has probably come down to 30 percent.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.