Jitendra Kumar GuptaMoneycontrol Research

It was mid-2015 and Dalal Street’s two stalwarts Vallabh Bhanshali (through Talma Chemical, a group company) of ENAM and Radhakishan Damani, promoter of D-Mart, bought into Balaji Telefilms at around Rs 80 a share. Other notable investors whose names figured in the list of shareholders included Rahul Saraogi of Atyant Capital, an offshore investment firm focusing on value investing opportunities in India.

While they still remain shareholders in the company, the stock has just started showing movement as it forays into the digital space that should play out meaningfully in the coming years.

Balaji Telefilms is a household name which has produced some of the best television serials including the famous Kyunki Saas Bhi Kabhi Bahu Thi. Its programmes such as Nagin-2 (Colors), Chandra Nandani (Star Plus), Ye Hai Mohabbatein and several others have a good viewership.

But those was the past laurels. Having made small screen magic, Balaji is now betting on the digital business to leverage on its existing fan followers, content library and its ability to produce original content. It has already made a beginning with the recently launched app ALTBalaji.

Unlike the television business, which is largely a B2B business (business to business), digital will operate on a B2C (business to consumer) business model, thus allowing the company to command higher margins and have a better control over its inventories.

The app will allow viewers to watch serials made from original content. This will be largely a subscriber-based model, catering to people who wants to enjoy their own choice of content at their own convenience. To begin with, Balaji has launched 6 shows and intends to add one new show every 15 days aiming to reach 32 shows in a year. Within a week of its launch, the app on android has been already downloaded by over one lakh viewers.

The company is looking at 4-5 million subscribers in the next three years which at Rs 60-90 per month is expected to fetch a revenue of close to Rs 300-400 crore. This will be in addition to revenues of Rs 292 crore which the company clocked in FY16. It will largely compete with YouTube and Netflix with the unique strategy of focusing on original content developed by the company in Hindi and other regional languages. YouTube has about 180 million subscribers in India and 67 percent of them are supposed to be watching Hindi content.

Hotstar, which allows viewers to watch live cricket and other TV shows, has close to 10 crore subscribers. While Hotstar is a free app, ALTBalaji is hoping to attract viewers or subscribers through delivering unique content capabilities.

"Balaji, in our view, has an edge in this regard going by its successful and long run in the TV space. Also, differentiated original content producers are better placed than aggregators due to high content acquisition costs," said Abneesh Roy, who is tracking the company at Edelweiss Securities

Profitability will get a bigger boost considering that it is going to be a low-cost model which will reap benefits of operating leverage. For instance, the traditional television programming usually reports operating margin of about 18 percent. For digital, the margins are expected to be in the range of 20-25 percent (at 4-5 million subscribers) and improve further as the subscriber base goes up.

If Balaji can replicate the success of its television content business in the digital space, the subscriber target of 4-5 million is not a tall ask. The app has already been downloaded in 70 countries and it will be particularly suitable for the Indian diaspora (NRIs) who view Indian sops as their daily connect to their country of origin. This population is relatively wealthier, have access to smart phones and would prefer the flexibility of watching their favorite sop at their own convenience.

As the penetration of smart phones improves, the industry can witness significant growth. US has close to 22 crore smart phones and a company like Netflix has close to 5 crore subscribers. India, which has a much larger population than the US, has only 34 crore smartphone users, considering the country has a total population of 130 crore. As the usage of smart phones become more popular, digital content can witness exponential growth.

Cash Cow

Digital is yet to make money for the company. Television programming business, which is the bread and butter business of Balaji, is making close to Rs 40 crore of annual cash flow on a total capital employed of Rs 120 crore. This business is also on the path of turnaround.

Sameer Nair, who had a very successful stint at Star as CEO, with television programmes such as Kaun Banega Crorepati to his credit, joined Balaji in mid-2014. Thereafter, there have been few strategic changes leading to improvement in its core programming business. The annual number of hours of programming has increased from 590 hours in FY14 to 962 hours in FY15 and 1002 hours in FY16. This led to optimum utilisation of resources leading to higher margins and revenue. Consequently, television programming business, which accounts for over 90 percent of its revenues has seen its margins improving from 4 percent in FY14 to 6 percent in FY15 and further to 14 percent in FY16.

Rational Capital Allocation

But the biggest drag so far has been the movie business. While the company has scaled down this business so that there are no major losses, a large part of the capital is still employed in this business. In the first nine months of FY17, this business released about four movies and incurred losses of Rs 39.2 crore on a revenue of Rs 116 crore. Film business, which employs Rs 144 crore of capital, has been incurring losses over the last four years. The company now intends to scale down the business and is looking for partners to unlock capital and rationalise its capital allocation. Around Rs 60-70 crore of capital is stuck in advances, which will get released once the operation is scaled down. Another Rs 60 crore of capital is employed in the inventory of two movies Half Girl Friend and Super Singh, which will get released in May 2017.

The shift in focus stands to improve the return ratios. Film business accounts for close to 30 percent of total capital employed. To put the numbers in perspective, in FY16, despite a 19 percent return on capital employed earned by the television programming business, the overall (consolidated) return on capital employed was negative as a result of losses in the film business.

Valuations

The company last year raised funds through QIP at a price of Rs 140 a share and the large part of this money is still parked with mutual funds. At the end of December 2016, it was holding cash and cash equivalents of close to Rs 200 crore which is 26 percent of the market capitalisation of Rs 758 crore. Currently, around Rs 340 crore of capital (Rs 140 crore in films, Rs 200 crore of cash equivalent) or 56 percent of the total capital employed in the business is not generating any meaningful return, once the losses reduce in the movie business and the idle cash gets deployed in digital, the impact on earnings and hence valuation can be meaningful.

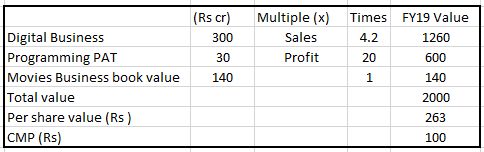

It is not unrealistic to assume that the digital piece of Balaji will mimic the growth trajectory of Netflix. Hence, we employ a sum of the parts valuation to look at the intrinsic value of this diversified business. Even if one excludes the value of the movie business, the value per share works out to Rs 245, driven largely by the new digital strategy.

Note: Estimated figures.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.