Anubhav SahuMoneycontrol Research

Bhansali Engineering Polymer Ltd (BEPL), leading manufacturer of ABS (Acrylonitrile butadiene styrene), reported continued momentum in earnings growth aided by elevated capacity utilisation, improved product pricing and better operating performance.

Near term earnings guided by better pricing and higher capacity utilisation

In Q3 FY18, BEPL posted net sales of Rs 258 crore, adjusted for both GST and excise duty, it was up 4% QoQ and 110% YoY. Improved turnover reflected higher pricing trend for ABS and the elevated capacity utilisation.

EBITDA margins improved sequentially by 154 bps (+938 bps YoY) on account of lower raw material cost (57.1% of net sales vs. 57.5% of sales in Q2 2018) and better realisations offsetting higher employee cost (22% QoQ). In addition, higher other income and moderate other expense helped net profit rise by 16% QoQ and 850% YoY.

Styrene/ABS pricing trend

News flow suggests elevated ABS (Acrylonitrile butadiene styrene) prices from the Asian region to continue in first quarter of calendar 2018. European counters indicate that price quotes from the Asia region are not competitive as it used to be, historically, suggesting strong demand in China and India.

Recently, global major Trinseo has added new capacity of 75,000 MT in China. However, ICIS reports that a good part of new supply could be absorbed in China due to new regulations banning the import of scrap plastics and pollution crackdown.

Further, raw material – particularly styrene – needed for the production of ABS are also expected to rise, particularly due to plant shutdowns in global styrene market. However, prices of Acrylonitrile have eased recently due to increase in supply.

Thus, raw material price volatility continues to be a norm in the ABS market but improving demand scenario is expected to be a key determinant for ABS pricing.

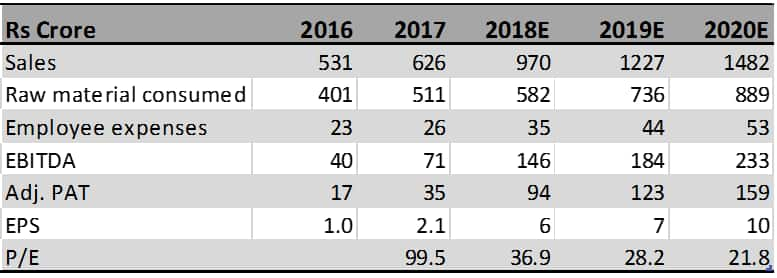

Financial projections and valuations

It is noteworthy that company is building a fourfold increase in manufacturing capacity in two stages, which should help in capturing the import-dependent domestic market (industry’s domestic capacity caters to 60 percent of demand).

In the near term, company is on course to increase capacity to 137,000 MT (from 80, 000 MT) involving capex of Rs 50 crore. As per the minutes of the recent Board meeting, it was confirmed that expansion would be complete by December 2018.

Further, the company expects that the greenfield expansion of 2lac TPA capacity would be commissioned earlier than expected i.e. by March FY 2021 vs. March FY 2022 previously anticipated.

As far as quarterly results are concerned, we are encouraged by the performance as the bottomline numbers are slightly ahead of our estimates. We therefore expect Bhansali to post earnings growth at a CAGR of 66% (FY 2017-20E).

However, after a remarkable performance (3 times since we initiated on 10th July’17), the stock is currently trading at 21.8x FY 2020 earnings which prices in near term expansion plan.

Having said that, Bhansali with its green field expansion plan, is on course to become a dominant player in the domestic ABS market. Additionally, it is incurring a capex of Rs 20 crore for the R&D centre in Aburoad, which would be useful for customized and high margin variants of ABS applications. Further, positive outlook for the end markets viz. Auto (50%) and consumer durables make it an accumulation candidate with a long-term horizon.

For more research articles, visit our Moneycontrol Research Page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!