Loan interest rates for buying a property in India are their lowest currently, at 6.70 percent. Many people are rushing to get their rates fixed at constant levels, as it helps in better money management during the initial loan tenure. This is because borrowers can better forecast their equated monthly instalments (EMIs) and thereby repay their home loans with ease.

Fixed interest rate home loans are usually offered at over one percent point higher than the floating interest rate, and have been mostly targeted at the non-resident Indian (NRI) community. Financial institutions would usually never market fixed interest rate home loans to their domestic customers; you would be encouraged to take a floating interest rate product.

Globally, it is common to see borrowers opting for fixed rate home loans during periods of low interest rates. The key takeaway is that the fixed interest rate averts the risk of having to pay more in the case of increased loan rates. The sense of stability that fixed rate loans instil in the borrowers’ minds has led many to include them in their financial planning, so that they may budget their future accurately.

These kinds of home loans are best suited for people who foresee a rise in lending rates and are apprehensive about having to pay more towards interest in the future.

Also read: Home loan interest rates unlikely to fall any further: Godrej Housing Finance

Why should you be wary of fixed rate home loans?Despite all their benefits, fixed interest rate home loans may not serve your purpose. The following facts may force you to think about how these loans, which look advantageous at the outset, may prove to be expensive in the long run.

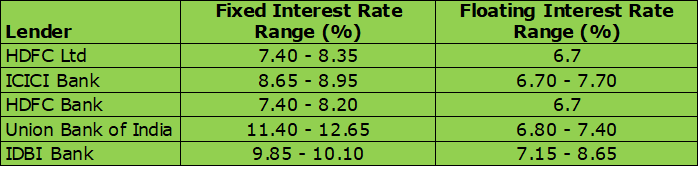

You could not be more wrong if you think that you would be offered a loan at the prevailing rate. This is because the fixed rate offered by banks or non-banking financing companies (NBFCs) is always higher than the floating interest rates. In most cases, rates are fixed at around 75 basis points more than the floating rates offered on home loans by lending institutions.

Also read: Why floating rate home loans hold an edge over their fixed interest peers

Rate cuts not effectedNo interest rate is too low, which means that the Reserve Bank of India may announce lowering of the lending rates after you take the home loan. However, due to the fixed nature of your interest rate, you will not qualify for paying EMIs at the new rate, which may be lower than the previous interest rate.

Temporary phenomenonVery few lending companies offer home loans at fixed interest rates for the entire tenure. This means the fixed rates chosen would be valid only for the first few years, after which borrowers will have to repay the loans at the revised interest rates (as available in the market).

This is because most lending institutions, barring a few banks, offer mixed home loan rates that allow the interest rate to be fixed only over the first two to five years. Floating interest rates apply to the remaining tenure of the loan.

Also read: How women can make the most of lower rates on home loans and stamp duties

Prepayment chargesUse any windfall gain to repay your entire home loan at one go. Prepayment of home loans is always an option if you wish to get rid of your debt altogether or reduce your existing debt burden to secure a new loan. Borrowers who have opted for floating interest rate loans do not have to pay any prepayment charges. However, lenders impose a penalty on prepayment of fixed interest rate home loans if it is a balance transfer.

In an economy prone to rising interest rates, availing of home loans at fixed interest rates is conducive to home loan repayment soon.

However, a sudden decrease in interest rate charges may mean that you remain bereft of the benefits of low-interest charges and continue to repay the same amount as determined during loan approval.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.