Ever since the Reserve Bank of India (RBI) pegged home loans to external benchmark rates, borrowers have seen their home loan interest decrease consistently. The RBI reduced the repo rate by 115 basis points (100 basis points = 1 per cent) ever since the lockdown began in March, to 4 per cent on May 22. So far, so good.

With home loan rates continuing to be benign, at least for now, a segment of home loan borrowers is contemplating locking into fixed-rate home loans, fearing rise in rates later in the year.

However, lenders decide on home loan rates based on multiple factors, such as the RBI policy rates, other broader market interest rates, the cost of funds and credit risk assessment. Hence, it would be very difficult to predict whether the home loan interest rates have indeed bottomed out. If the uncertainty is making you consider fixed-rate loans, you need to understand the few nitty-gritties.

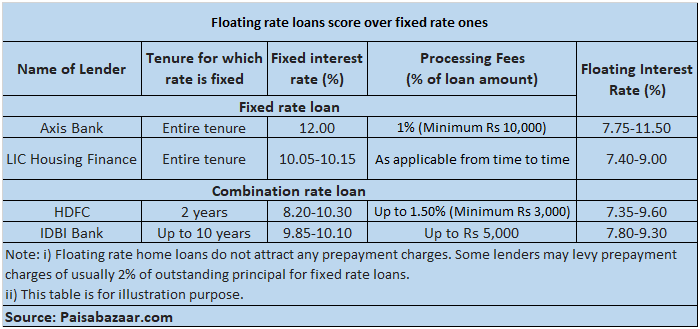

Low interest rate: an opportunity or a trap?It might be tempting to switch to fixed rate loans, now that the interest rates are already down significantly so far this year. Typically, the EMIs of a fixed rate loan remain the same through the loan tenure. Axis Bank and LIC Housing Finance offer fixed interest rate loans for entire tenures.

Lenders charge more for fixed rate home loans to cover their own interest rate risk. That’s mostly the norm even if you compare the two types of rates from the same lender. The difference can be as high as 250-400 bps depending on the lender.

Naveen Kukreja, CEO and Co-founder, Paisabazaar.com says, “The higher interest cost will thereby reduce the home loan eligibility of the borrower seeking fixed rate home loans.”

The choice in fixed rate loans is also limited as most lenders offer only floating rate loans. “Existing fixed interest rate loans are still overpriced, so don’t jump in to take them. Around the festive season between September and December, banks may launch fixed rate home loan schemes at a reasonably competitive price,” says Harsh Roongta, a SEBI-registered Investment Adviser.

In fixed interest rate home loans, lenders levy prepayment charges of usually two per cent of outstanding principal. Floating rate home loans do not attract any prepayment charges. Thus, floating rate home loans are cost effective for borrowers wishing to make prepayments in the future.

How about loans that offer a combination of fixed and floating rates? So, your loan rates remain fixed for about 3-5 years to begin with, and later the interest rates becomes floating, as per the rates prevalent then. The features are similar to teaser loans that were launched in 2010. The benefit here is if you feel interest rates are about to rise soon and may keep rising for a few years, you enjoy the low and fixed rate initially. Later, when interest rates in the economy look to head south, you can switch to floating rates.

That’s more complicated than it looks. It is difficult to predict interest rate movement in the future. If interest rates are still on the rise when the time comes for you to switch from fixed to floating rates, you might end up paying a higher EMI. The RBI had frowned upon such teaser loan schemes in the past.

Kukreja adds, “At present, the interest rate charged during the fixed-rate period is usually higher than the rates charged on floating rate home loans.” That’s another disadvantage.

Switches from fixed to floating rate home loan schemes attract switching fees. The State Bank of India (SBI) charges 0.56 per cent of the outstanding loan for switching from fixed to floating rates.

Benefit now, but pay laterThe devil lies in the fineprint. Sometimes, fixed rate loans come with reset clauses. Some lenders reset it every 2-5 years; others have clauses linked to their cost of funds. Depending on the product’s feature, a few others convert fixed interest rate loans to floating interest rate loans.

Raj Khosla, Managing Director and Founder, MyMoneyMantra says, “The major drawback in a fixed rate home loan is that if the interest rate remains benign or drops further during the tenure of the loan, you will not get the benefit of reduced interest rates as banks will not change the fixed interest rate while you are servicing a loan.” At present, despite massive cuts, nobody can tell exactly how far interest rates can go down.

Therefore, it’s crucial that you understand or have knowledge of where interest rates are headed, if you opt for a fixed rate loan.

If your fixed rate loan becomes floating in future, ask if the new floating rate would be linked to an external benchmark or linked to your bank’s own marginal cost of funds. Lastly, understand the costs involved in switching from fixed to floating interest rates.

Khosla says, “Today, banks are finding it difficult to disburse home loans. So, negotiate the fixed rate down to levels as close to the present floating rate as possible and then lock in for five to seven years’ loan tenure. This may give you maximum value.”

Moneycontrol’s takeAll said and done, floating rate home loans are more transparent. They give flexibility in moving between banks and benefitting from competitive pricing structures. Also, there are no prepayment charges applicable. Thus, it becomes easier and inexpensive for floating rate borrowers to move to another lender in case their rates don’t reduce as much as the market. Such flexibility comes at a price for a fixed rate home loan borrower.

A fixed interest rate home loan will help borrowers in a rising rate scenario. This, however, comes at a higher price.

Go for a fixed rate loan only if it is a slightly shorter tenured loan and you believe that interest rate movement in the economy works to your benefit. But it is better to stick to floating rate loans benchmarked to external rates.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.