In the investing world, sales and product brochures are cleverly laced with data that shows the potential investor exactly what the product manufacturer wants to present. It's common to see the numbers being picked and chosen to convince someone of the opportunity or the lack thereof. As Mark Twain once said, "There are lies, damned lies and statistics."

We recently came across a video in which they speak about why investments should be concentrated in India; the reason cited primarily that this is a growing market with more opportunities to make money; and comparing the returns of HDFC Bank over Apple (not ideal to compare a bank with a consumer tech company) and Maruti Suzuki over Honda and Toyota.

So, we decided to explain why we disagree with the thoughts of being a India centric investor.

For someone looking to invest outside India, the first choice or preference is the US market. This is because we all face something called the "familiarity bias". Some of the largest companies in the world are listed there and it's not just that, these are also companies whose products we use extensively in our daily lives – Amazon, Alphabet (Google), Facebook, Netflix, Apple. And since we're familiar with the brands and their products, we prefer to own these stocks because we think we understand these companies. The problem however with buying these "multi-baggers" is that in hindsight we always know which one we should have bought, it doesn't tell us what we should buy to generate the higher than average returns.

Let's look at it from an Indian context. How often have we received a WhatsApp forward saying if you’d invested in 100 shares of Eicher Motors (the markers of the Royal Enfield motorcycles) in the early 2000s you could’ve now bought 10 Bullet bikes with wealth the shares would have created for you. And similarly goes the story of Page Industries (distributor of the Jockey brand in India) or Symphony (makers of air coolers).

Now, do you know anyone who had the prescience to buy these stocks and just hold it patiently irrespective of what was happening with the markets during a 10-15 year period? The question is not just of identifying a stock but also evaluating whether consumers prefer that brand over its peers. Given a choice in the 90s, would you have bought shares of Maruti Suzuki (erstwhile Maruti Udyog) over Hindustan Motors or Eicher Motors over Bajaj Motors? And in the 2000s, would you have bet all your money predicting that the golden era of Nokia or Blackberry would be disrupted (very quickly) by Apple? It's easy to make statements in hindsight.

So, what’s the alternative? Buy an actively managed fund or the index. With diversification, you may not find that 1 multi-bagger you’ve been dreaming about, but you’ll also save yourself the trouble of having mini panic attacks each time your chosen stock drops by 20% or it misses a quarter’s earnings estimate.

Global diversificationNow that we’ve established that investing in a mutual fund (whether domestically or internationally) is a simpler and smarter strategy for most retail investors than trying to identify ‘the stock’, ‘let’s look at why we must think about global diversification. If we take a step back and take a look at our portfolios, in all probability we’ll find that our investments are concentrated in Indian mutual funds and stocks. It’s a stronger form of the familiarity bias at play here- we suffer from home bias. We do this because we believe (whether wrongly or rightly) that the Indian economy will grow at a fast clip and this in turn will create large wealth for us in the Indian equity markets. And the media sharing quotes of foreign fund managers speaking about investing in India doesn’t hurt the justification process as well.

So, let’s break the returns down so that you can judge for yourself.

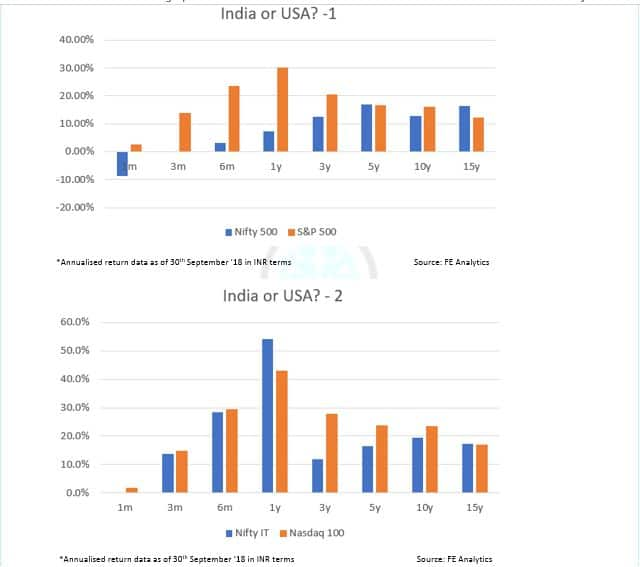

It doesn’t seem so straightforward now, does it? While India’s Nifty 500 index has outperformed the US S&P 500 for a 5 year and 15 year period, the S&P 500 has come out on top when you look at the 3 year or 10 year data. And despite India being an IT powerhouse, the tech heavy US Nasdaq 100 index has trumped the Nifty IT index for a 3, 5 and 10 year period.

It doesn’t seem so straightforward now, does it? While India’s Nifty 500 index has outperformed the US S&P 500 for a 5 year and 15 year period, the S&P 500 has come out on top when you look at the 3 year or 10 year data. And despite India being an IT powerhouse, the tech heavy US Nasdaq 100 index has trumped the Nifty IT index for a 3, 5 and 10 year period.

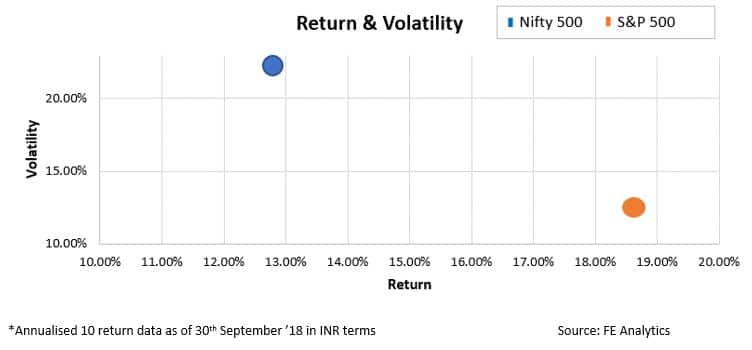

Now if we overlay the risk factor (in terms of how volatile the returns are), the S&P 500 emerges the winner quite comfortably with volatility that is almost half of that of the Nifty 500. As we’ve seen earlier, the returns vary depending on the time period you choose for analysis but the volatility of the S&P 500 has been far lower than the Indian indices irrespective of the time period chosen.

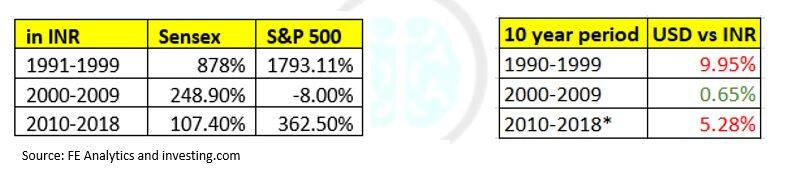

Let’s break the returns down on a decadal basis; and suddenly the numbers look extremely different. For an investor who decided to participate in the S&P 500 during the 2000s by looking at the returns from the 90s, she would likely have berated herself for her folly of missing out on the Indian markets.

Let’s break the returns down on a decadal basis; and suddenly the numbers look extremely different. For an investor who decided to participate in the S&P 500 during the 2000s by looking at the returns from the 90s, she would likely have berated herself for her folly of missing out on the Indian markets.

If you also consider how the currency behaved during these periods, you’ll find that the ‘lost decade’ in the US coincided with a period during which the Indian rupee actually strengthened against the US dollar. While traditional economic theory says that the currency of a country with higher inflation (India) weakens against a country with lower inflation (US), the numbers only seek to remind us that while this is true in the long term, there will be periods when this link can be broken.

If you also consider how the currency behaved during these periods, you’ll find that the ‘lost decade’ in the US coincided with a period during which the Indian rupee actually strengthened against the US dollar. While traditional economic theory says that the currency of a country with higher inflation (India) weakens against a country with lower inflation (US), the numbers only seek to remind us that while this is true in the long term, there will be periods when this link can be broken.

Since no one can accurately and consistently predict when these periods will occur, we diversify.

So how do we go about doing this? The easiest route for most retail investors is to opt for one of the ‘feeder mutual funds’ in India. These funds typically invest into a larger fund that is operated internationally. Unlike many others, we won’t tell you that a minimum of 5% or 10% of your portfolio should be in these funds; since that’s usually not a number that has been arrived at by a scientific calculation. However, if you have dreams and goals that are intrinsically linked to the foreign countries such as holidays and higher education, you should allocate part of the investments towards these goals into foreign market feeder funds. The primary objective of this isn’t to chase supernormal returns but as an investment which will also serve as a currency hedge in case of a depreciating Indian rupee. This just means that if the Indian rupee falls against the US dollar, that will get added into the returns of your US based fund (when you withdraw the investment).

Many years from now, an investor who again believes firmly in the ‘India growth story’ will probably come back and say why we should invest in India because historically the Thomas Cook stock outperformed the Expedia group (their returns in the past 5 years have been similar) but we don’t know that now.

And as Chester Nimitz said, "Hindsight is notably cleverer than foresight." Happy investing!

The writer is co-founder and head of research at Investography.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.