There has been increased penetration of credit card usage in India. However, credit card is not offered by banks to all the applicants. Banks have denied credit cards to customers due to low or no credit score, inadequate income, or risky job profile. Now, you need not worry if your credit card application is rejected, as you can apply for secured credit cards offered against your fixed deposits.

Sanjeev Moghe, EVP and Head, Cards & Payments at Axis Bank says, "At Axis Bank, the secured card (credit card issued against FD) as a product has been around for more than a decade now. We have over one lakh cards as of today.”

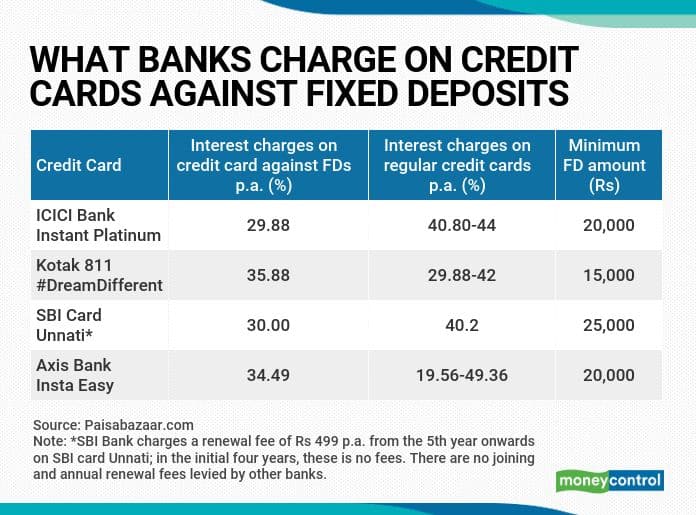

What’s on offerState Bank of India, Bank of Baroda, Kotak Mahindra Bank and Axis Bank among others offer secured credit cards against fixed deposits. The fixed deposit acts as a collateral or security against which the credit card is issued to the applicant. These cards are backed by a fixed deposit of as low as Rs 15,000. Depending on the bank, the credit limit of a secured credit card usually ranges between 80 and 90 per cent of the fixed deposit amount.

For instance, if you have a fixed deposit of Rs 15,000 with Kotak Mahindra Bank, you can apply for Kotak 811 #DreamDifferent with a credit limit of up to 80 per cent of the fixed deposit. The bank allows you to choose a credit limit of your own choice. In this illustration, you can get a credit limit of up to Rs 12,000.

The fixed deposit should be of the same bank while applying for a credit card. Each bank has its own minimum amount for providing credit cards against fixed deposits. “You have to meet that minimum limit either through one of your fixed deposits or by clubbing more than one deposit with the bank,” says Gaurav Gupta, Co-founder and CEO of MyLoanCare.

“The secured credit card against fixed deposits gives customers quick and easy access to credit, while they continue to earn interest on their fixed deposit,” says Ambuj Chandna, President of Consumer Assets at Kotak Mahindra Bank.

Depending on the banks, you get up to 50 days’ interest-free credit period on all spending done using this credit card. In case of non-payment of credit card bill before due date, the banks charge interest rate which goes up to 36 per cent per annum.

The secured credit card against fixed deposit is an ideal choice for people with low income, poor credit history, an irregular income, no income proof, senior citizens and home makers. “As secured card transactions are also reported to the credit bureaus, their disciplined use can help you in building or improving credit score and, thereby, boost your loan eligibility in future,” says Sahil Arora, Director of Paisabazaar.com.

The credit cards availed against fixed deposits are secured, so some banks charge lower interest compared to regular credit cards. For instance, the interest rate on ICICI Bank Instant Platinum (secured credit card) is 2.49 per cent a month. However, the rate of interest on regular credit cards of ICICI Bank start from 3.40 per cent a month.

Most of the banks do not charge joining or annual renewal fees from the customers for secured credit cards. On regular credit cards the banks charge annual fees between Rs 500 to Rs 5,000 from the customers, depending on the variant of the credit card.

What does not workThe main drawback of secured credit cards is if you fail to repay your credit card dues with interest over the months, then the bank can take over your fixed deposits to recover the credit amount. Also, the fixed deposit gets attached to the credit card; you cannot, therefore, prematurely withdraw, even for an emergency. “Apart from losing your fixed deposit, your credit score will also get impacted due to non-repayment of dues,” says Arora.

Your secured credit card is linked with the maturity of fixed deposit. So, after your FD matures, you may no longer able to use the linked credit card for transactions. You will have to apply for a new credit card after the FD matures.

“The other drawback of secured credit cards is the lack of diverse choices that one gets in the case of regular credit cards,” says Gupta. Banks offer only one type of secured credit cards, while they offer multiple variants of unsecured or regular credit cards exclusively aimed at different customer segments and spending habits.

Moneycontrol’s takeIf you do not get a credit card through normal means, especially if you are in your first or second job, then getting a secured credit card through an FD is fine. Just make sure that you do not touch the FD money till maturity. In the long run though, getting a regular credit card or not having one tied to your FD always works better and gives you more flexibility. Ofcourse, you need to be a disciplined spender.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.