Starting from this month, mutual funds have started disclosing crucial data that helps you assess how much risks your debt funds can take.

Contrary to the popular belief that liquid schemes carry the lowest credit and interest rate risks (along with overnight schemes) and hence they should be placed in cell A-I depicting the same, they have been placed in B-I PRCM. Liquid schemes of fund houses such as ICICI, HDFC, Axis, Kotak and SBI MF are in B-I PRCM. Liquid schemes of IDFC, Quantum, PPFAS, Trust AMC are in PRCM cell A-I.

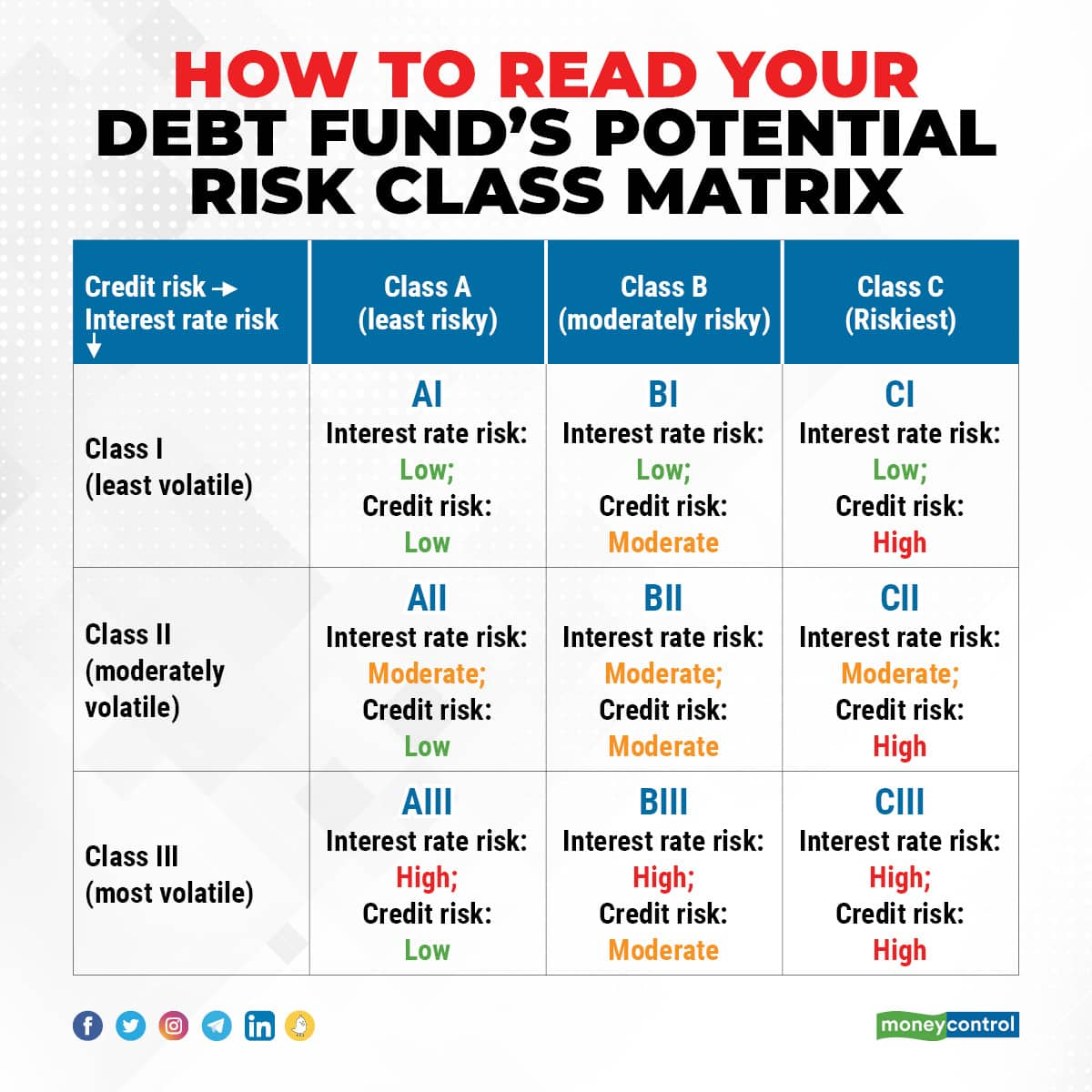

In simple terms, a scheme that comes with a risk matrix rating of A-I is said to be less risky than the one that comes with B-I rating. Here’s more clarity on the matter.

Checking the scheme’s risk boundariesAside from revamping the existing risk-o-meter guidelines, SEBI also introduced a Potential Risk Class Matrix (PRCM) for debt schemes. Just like a scheme objective, which is set first at the time of its launch and cannot be changed, unless unitholders’ mandate is sought, a PRCM is also part of its fundamental attribute. The risk-o-meter is somewhat like a report card that comes out every month based on the scheme’s portfolio.

A scheme’s PRCM defines the maximum level of risk a fund can take. There is the fund’s credit risk (measured by credit risk value; Class A to C in ascending order of risk) and interest rate risk (measured by the scheme’s modified duration; Class I to III, in ascending order of risk). A scheme’s PRCM of AI means the scheme is least risky; a reading of CIII makes it the riskiest (see graphic).

Same category, different risksSo what explains two liquid funds with different risk boundaries?

Commercial papers and certificate of deposits enjoy high short-term rating. However, in the long term, the issuer’s rating may be AA or below. “For investments made by mutual funds in instruments having short-term ratings, the credit risk value shall be based on the lowest long-term rating of an instrument of the same issuer (in order to follow a conservative approach) across credit rating agencies,” said a SEBI circular dated June 7, 2021 that rolled out the PRCM framework.

Put simply, if the fund manager wants to invest in a paper with lower credit rating of the issuer for the long term, then he has to account for the same in the PRCM. Though B-I need not be an alarm bell as such, it is prudent disclosure that the fund manager may take risk to generate some extra returns over those offered by ‘high-quality’ bonds.

But some fund houses do not want to take credit risk at all. Sandeep Bagla, Chief Executive Officer, Trust Mutual Fund says, “Long-term ratings have been as important as short-term ratings when we choose bonds for our portfolios since inception, to ensure the quality of our debt portfolios. The methodology prescribed by the market regulator makes it mandatory to consider long-term ratings on the bonds.”

Credit risk schemes and are placed in the C-III segment, which captures highest credit and interest rate risks. However, IDFC credit risk fund is placed in B-III cell, depicting high interest rate risk and moderate credit risk. Though many schemes have been running portfolios with durations of less than three years, fund houses still want to place their credit risk schemes in high interest rate risk zone. This allows the fund manager to invest in bonds with longer maturity as and when there is an opportunity.

Banking & PSU debt funds delivered attractive yields with relatively less risk compared to corporate debt schemes. However, things have changed since March 2021. Many of these schemes held perpetual bonds issued by banks and SEBI restricted the exposure to these bonds and also changed the way they are valued. Many fund houses have opted to place their schemes in the A-III and B-III cells.

Trust Banking & PSU Debt Fund, launched in February 2021, is placed in the A-III PRCM cell. “Though we may not be keen to take exposure to long duration portfolios currently, in the long term, such duration portfolios may be attractive. And PRCM placement of schemes factors in that possibility,” says Bagla.

Since a scheme’s PRCM is its fundamental attribute, any change in it comes with a mandatory exit window for investors in case they feel uncomfortable.

What should you do?Thanks to a dynamic risk-o-meter and the newly-introduced PRCM, it’s easier to understand your debt fund now. “Going solely on the basis of past returns may not really help,” says Joydeep Sen, Corporate Trainer-Debt. Sen adds that while the IL&FS fiasco may be behind us, it pays to be watchful where your debt fund invests in.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.