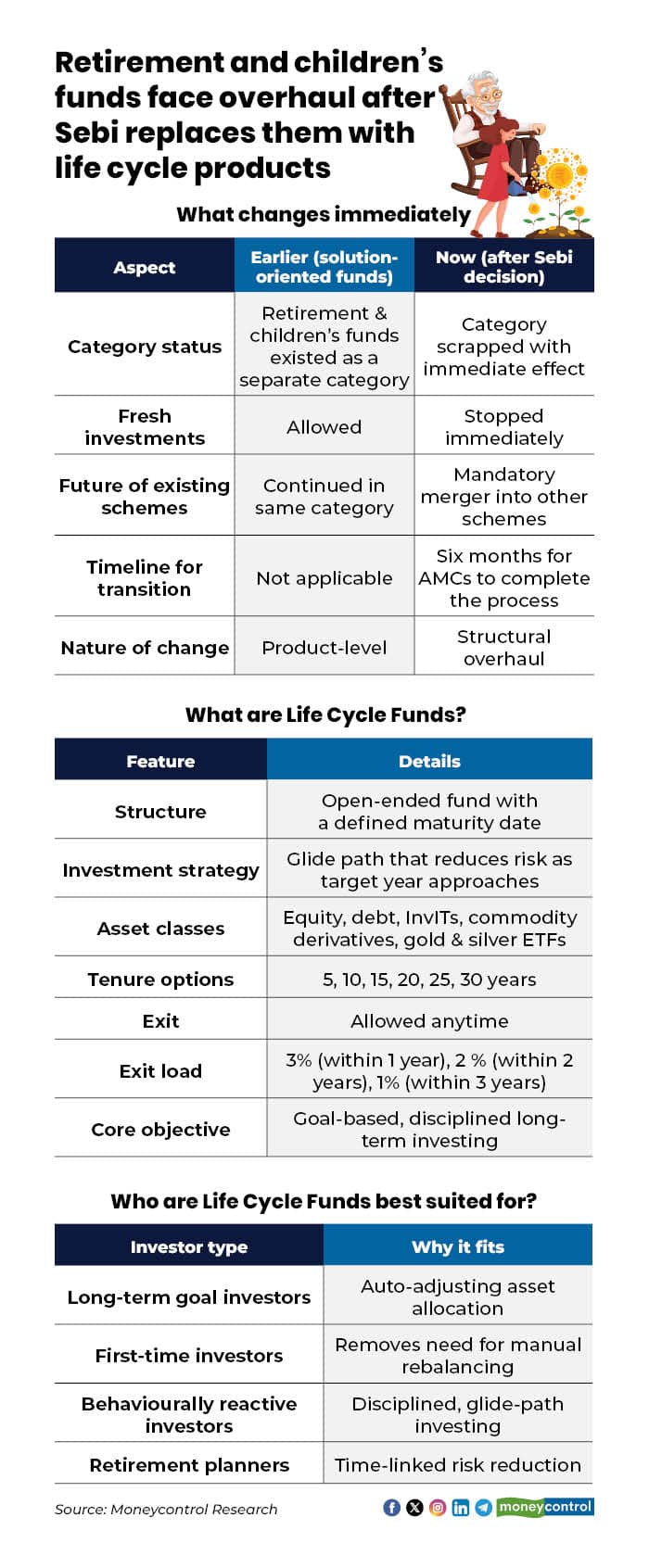

Securities and Exchange Board of India (Sebi) has scrapped the solution-oriented category (retirement + children’s funds) with immediate effect and replaced it with a new class of mutual fund schemes called Life Cycle Funds, signalling a structural overhaul in how goal-based products will be offered to investors.

The old scheme has to be merged with the new schemes that have similar asset allocation and risk profiles, subject to Sebi’s approval. The shift is structural, not cosmetic, and AMCs have been given a defined transition window. But what does this mean for existing solution -oriented investors? Should investors in existing schemes stop fresh subscriptions immediately, since they will not remain in their current form and will have to follow a time-bound transition? Here is a lowdown on how it impacts existing investors:

What are Life Cycle Funds?

The new scheme, called Life Cycle Funds, will be open-ended with a set maturity date and a glide path for investing across various asset classes such as equities, debt, InvITs, exchange-traded commodity derivatives, and gold and silver ETFs.

Since it is open-ended, investors can exit at any time. However, those who exit within one year will pay a 3 percent exit load, which decreases to 2 percent if redeemed within two years, and to 1 percent if they exit within three years.

The move is aimed at promoting disciplined, long-term investing through a pre-defined asset allocation strategy that becomes more conservative as the target date approaches.

“Align with the new Life Cycle Fund framework, which features glidepath-based, tenure-defined investing across various asset classes. This is not just a rebranding; it marks the regulatory sunset of the old category,” said Sameer Mathur, MD and Founder of Roinet Solution.

For example, Life Cycle Funds can be organised with target maturities of 30 years, 25 years, 20 years, 15 years, 10 years, and 5 years. The structure aims to align investments with specific financial goals by automatically adjusting the portfolio mix over time.

Impact on existing schemes

The old schemes will not run till maturity on their own; instead, they will be merged into similar funds within a fixed six-month timeline. Investors do not have to take any action for the merger, but their fund’s strategy and risk level may change once the shift happens.

“It is a clean break-no gradual shift. Sebi has immediately eliminated the solution-oriented category. New Life Cycle Funds introduce smarter, life-stage-based risk adjustment. Existing schemes? Closed to new money right away, with a mandatory merger process ahead," said Akshat Garg, Head - Research & Product, Choice Wealth.

"No phasing out or run-to-maturity-they are getting merged into matching schemes (not necessarily Life Cycle Funds yet, but comparable ones). AMCs have six months to wrap it up, so think August-September 2026 deadline. No choice in the matter; it’s SEBI-approved or bust," added Garg.

This means the existing schemes will be merged with similar schemes (likely hybrid or multi-asset funds) after Sebi approval. AMCs have six months to align all schemes with the new categorisation framework.

“There is no provision for letting these schemes' run their course' until maturity because they were open-ended and not tenure-bound,” said Mathur.

What changes occur in asset allocation?

Life Cycle Funds aim to manage risk by following a glide path, which systematically reduces equity exposure over time across various asset classes.

Glide paths of existing schemes will not continue as is, because the category itself is being dissolved. Post-merger, the asset allocation will shift to align with the receiving scheme’s mandate, not the original retirement/children’s glide path.

“Life Cycle Funds, once launched, will have pre-defined tenures (5–30 years) and glide paths that automatically reduce equity exposure as maturity approaches. For investors, this means the risk-return profile of their current scheme will change once the merger is executed,” said Mathur.

“The choice of funds with different target dates makes them relevant for investors across age groups,” said Nilesh D Naik, Head of Investment Products, Share.Market.

Where will schemes be merged?

Investors will be mapped to schemes with similar risk profiles. Once Life Cycle Funds are launched, they will offer time-linked glide paths in which equity exposure reduces as the target year approaches, typically across 5–30-year options. Exit loads in a graded structure are expected to discourage early withdrawals and keep the investment aligned to long-term goals.

"A bit of friction: no new inflows into old schemes, and Life Cycle launches aren’t live yet, so money might slosh into hybrids or multi-asset funds temporarily. Smaller AMCs could feel portfolio squeezes, but the six-month runway and industry buy-in should keep chaos low," said Garg.

“Flows may temporarily slow as AMCs stop subscriptions and investors reassess options. Portfolio churn may rise as schemes prepare for mergers and align with new mandates. However, Sebi’s intent is to reduce overlap, simplify choices, and improve transparency, which should stabilise flows over time. The disruption is operational, not systemic,” Mathur added.

Taxation shift explained

For most investors, solution-oriented funds were treated like equity funds after the five-year lock-in, so long-term gains were taxed at 12.5 percent.

In Life Cycle Funds, taxation may move gradually from equity to debt treatment as the fund becomes more conservative closer to maturity, which can change the final tax outcome.

Nitin Agrawal, CEO, Mutual Funds, InCred Money, said, “Based on the current structure of Life cycle funds in terms of the underlying glide path, there is a drift in taxation from equity to debt as you move closer to maturity, when the debt allocation increases, making it a more debt-oriented product.”

What should investors do?

A practical approach is to review your existing retirement/children’s fund holdings, as their mandates will change after the merger. Check the receiving scheme’s risk profile; it may not match your original goal-based intent.

“If you still want a goal-linked, glide path-based product, consider switching (once available) to a Life Cycle Fund with a maturity aligned to your target year. Avoid knee-jerk exits; wait for AMC-specific merger details before acting,” said Mathur.

Garg further said, "If you are in already: Sit tight-rushing out triggers loads and taxes. Wait for your AMC’s merger note, eyeball the new scheme, and exit load-free if it’s off-goal. Planning to jump in? Hold off here; grab a hybrid interim and pounce on fresh Life Cycle launches soon. Patience pays—this is a step up for goal-based investing. Keep tabs on AMC emails."

“Such products may be very useful for investors who find it difficult to maintain investing discipline due to behavioural biases influencing their buy/sell decisions. Given that such funds are typically used for long-term investment and have a higher exit load in the initial years, investors need to ensure they do thorough due diligence before investing,” said Naik.

Disclaimer: The views and investment tips expressed by experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.