YOU ARE HERE:HomeNewsBusinessPersonal Finance Personal Loan Prepayment: Key points to consider before paying off your loan earlier

Personal Loan Prepayment: Key points to consider before paying off your loan earlier

20 January, 2025 | 16:12 IST

Personal loans, like many other credit instruments, could be helpful in meeting financial needs for several purposes like home renovation, managing unexpected medical expenses or paying off an existing debt. While obtaining a personal loan is relatively straightforward, maintaining financial stability requires careful management and repayment. One key decision a borrower often faces is whether or not to opt for personal loan prepayment.

Personal loan prepayment refers to the act of paying off a loan before its scheduled end date. Borrowers often consider prepaying their loans to reduce the overall interest burden, free up their credit lines or to get rid of loans when they have enough money in hand. While the benefits of prepayment are apparent, it is essential to understand the financial implications involved.

Interest savings: One of the major reasons to prepay a personal loan is the potential to save on interest payments. Personal loans may come with higher interest rates compared to loans such as a housing loan or a car loan. By prepaying, you reduce the principal amount outstanding, which consequently reduces the total interest you will pay over the tenure of the loan.

Improved credit score: Personal loan prepayment can positively impact your credit score. A lower credit utilisation ratio, which results from reduced loan balances, can improve your credit profile. Also, timely prepayments show financial responsibility, which can further boost your credit score.

Financial freedom: Prepaying your personal loan can relieve you from monthly EMI obligations. This can be beneficial if you have other high-interest debts or unexpected expenses that need immediate attention. Completing loan repayments can also help reduce financial stress.

Personal loan prepayment penalty and other charges

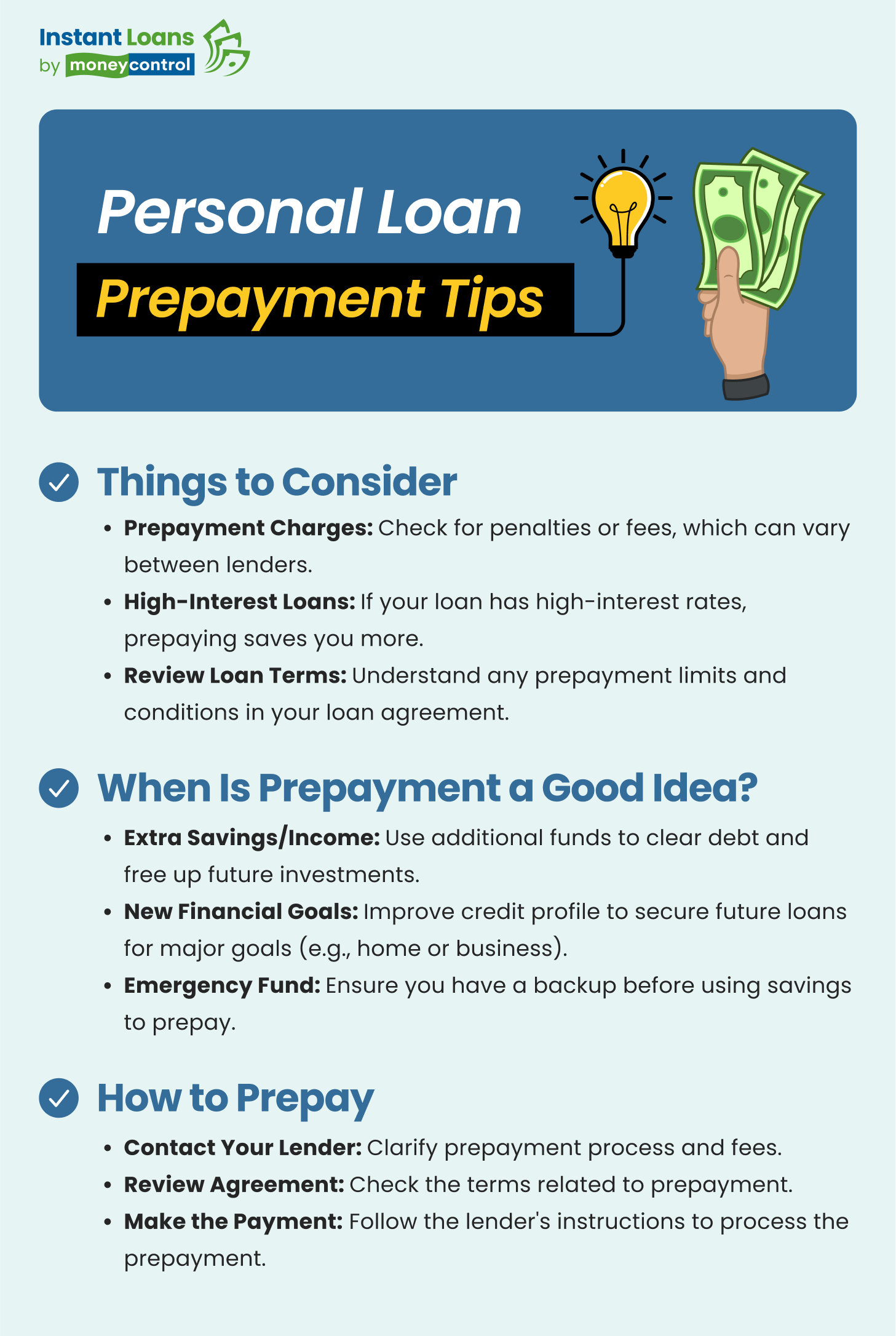

The personal loan prepayment benefits notwithstanding, it is important to be aware of the charges or penalties. Many lenders often charge prepayment fees for a partial prepayment or a full prepayment of a personal loan. The personal loan prepayment charges can vary depending on the lender and the loan agreement. Lenders levy prepayment charges to compensate for their loss of future interest income. The personal loan prepayment charge is often a percentage of the prepayment amount or the remaining principal. The charge may vary based on the time when you make the prepayment. The charges may be as low as nil to as high as 7% of the principal due. It’s important to review your loan agreement to understand the exact charges applicable.

Personal loan prepayment is not always the right choice for everyone. Here are some scenarios when prepayment could be a suitable option:

You have taken a loan with high-interest rates: If your personal loan has a high-interest rate, prepaying it can lead to substantial savings. The higher the interest rate, the more you will benefit from reducing the principal amount early. In such cases, the savings from prepayment can outweigh the charges or penalties incurred.

Your income has increased income or you have some extra savings: If you get extra income or accumulate some savings, prepaying your loan could be a wise decision. Extra funds can be used to pay off the loan, thereby freeing up your monthly budget for investments.

You have set new financial goals: If you have some specific financial goals on your mind, such as buying a home or starting a business, personal loan prepayment can improve your credit profile and increase your chances of securing additional credit.

Factors to consider before personal loan prepayment

Before personal loan prepayment, consider these factors:

Personal loan prepayment charges: Evaluate the personal loan prepayment charges, and compare these costs with the potential interest savings to determine whether prepayment is beneficial.

Prepayment period limitations: Depending on the lender’s policies there might be a lock-in period associated with the prepayment of your personal loan. There might also be a limit on the number of times you can do prepayments in a year.

Emergency fund: Ensure that you have an adequate emergency fund before using your savings to prepay the loan. Financial security should always be a priority, and having an emergency fund can protect you from unforeseen expenses.

Alternative investments: Assess whether your money might be better invested elsewhere. If you can earn a higher return on investments compared to the interest savings from personal loan prepayment, it may be more advantageous to invest your additional funds rather than spending it on prepaying the loan.

Making the most of your personal loan prepayment

If you decide to proceed with prepayment of your personal loan, follow these steps:

Contact your lender: Reach out to your lender to understand the prepayment process and confirm the personal loan prepayment charges or penalties involved. Obtain a detailed breakdown of the outstanding principal and any applicable fees.

Review your loan agreement: Carefully review your loan agreement to ensure compliance with Personal Loan Prepayment terms.

Make the payment: Arrange for the personal loan prepayment through the lender’s specified channels. Ensure that the payment is processed correctly and that you receive confirmation of the updated loan balance.

You can access and evaluate suitable personal loan offers on online platforms like Moneycontrol, which provide instant loans with a streamlined process. You can enjoy a hassle-free experience with no paperwork, low processing fees, and instant disbursal to your bank account. You can get your loan in just three easy steps — enter your details, complete KYC and set up EMI repayment.

Moneycontrol has currently partnered with four lenders to offer instant loans up to Rs 15 lakh, allowing you to choose between personal and business loans based on your employment status. Interest rates start at 12% per annum, and there are no hidden charges.

Overall, deciding whether to prepay a personal loan involves careful consideration of various factors, including potential savings, prepayment charges, and your overall financial situation. By understanding the benefits and costs associated with personal loan prepayment, you can make an informed decision that aligns with your financial goals.

Summary

Prepaying a personal loan can save you money and offer financial freedom, but it's essential to weigh the benefits against the costs. Careful planning and understanding of the process can help you make an informed choice.

Disclaimer

This piece/article was written by an external partner and does not reflect the work of Moneycontrol's editorial team. It may include references to products and services offered by Moneycontrol.

100% Digital

100% Digital Quick Disbursal

Quick Disbursal Low Interest Rates

Low Interest Rates