Non-Resident Indians (NRIs) with earnings abroad and in some cases in India often find it challenging to repatriate money to their home account in India. To overcome these hassles, banks in India offer Non-Resident External (NRE) Account and Non-Resident Ordinary (NRO) Account. These bank accounts can be opened by NRIs, Persons of Indian Origin (PIOs) and Overseas Citizens of India (OCI).

Why do we have NRE and NRO accounts?As per the Foreign Exchange Management Act (FEMA) guidelines, an NRI cannot have a local savings account in his or her name in India. You must convert all your savings (money earned abroad) into an NRE or NRO account. “Continuing to use the local savings account in India can attract hefty penalties. You need to inform your bank in case travelling abroad for an indefinite period to convert a savings account to NRE or NRO account as per usage,” says Chandrakanth Bhat, Founder, NRI Money Clinic.

Opening an NRE or NRO account helps NRIs in multiple ways. For instance, you can transfer your foreign earnings to India in case you have family over here who is dependent on you. Also, income from India through any investments can be retained here.

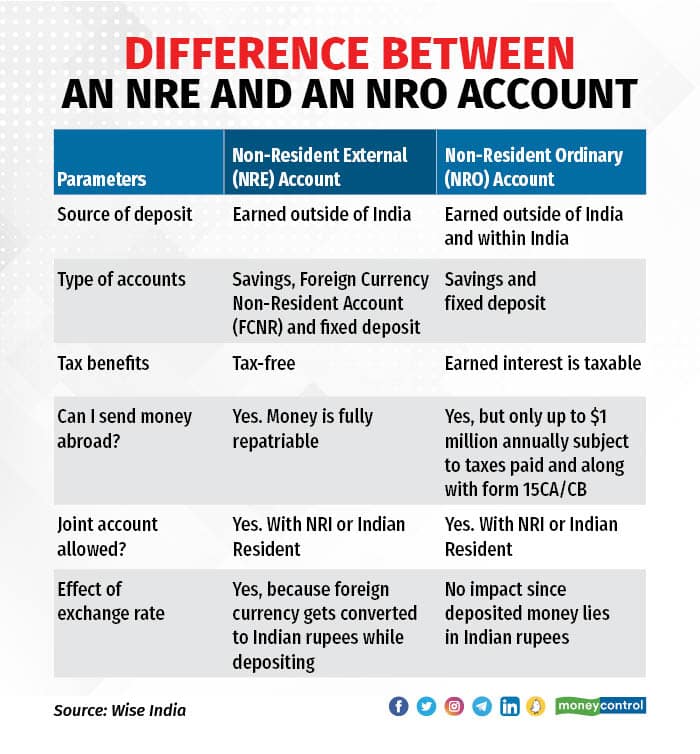

What is a Non-Resident Ordinary Rupee (NRO) Account?NRO accounts help you manage Indian rupee income sources like rent, dividends, or any other income such as profits that come to you by a sale of property or investments, here in India. It could be a saving account or a fixed deposit account. Here, both non-resident and resident Indians can be joint account holders. The account also allows you to receive income from foreign currency converted to Indian rupees and in Indian rupees as well. The money lies in Indian rupees in the NRO account.

“The NRO account can be debited for the purpose of local payments, transfers to other NRO accounts or remittance of current income abroad,” says Kartik Jain, Head - Product & Platforms, Consumer Banking Group at DBS Bank India.

However, NRIs should give prominence to NRE accounts to remit income abroad because repatriation of money in NRE accounts doesn’t require any permission and has no limits. The NRO account has a restriction of repatriating not more than 1 million US dollars, per financial year, inclusive of taxes. You also need to submit form 15CA/CB, which is a chartered accountant’s certificate confirming the tax payments as due.

“Any gift in rupees or a loan by a resident Indian to an NRI within the remittance limits prescribed can be credited to the NRO account,” says Virat Diwanji, Group President and Head – Consumer Bank and Member, Group Management Council, Kotak Mahindra Bank.

There are certain drawbacks to holding NRO accounts. The interest you earn in the NRO account is subject to tax deducted at source (TDS), whereas interest earned on NRE accounts is tax-free.

You can also link your NRO account to make investments in India.

What is an NRE Account?The NRE account is an Indian rupee-denominated account. It could be savings, Foreign Currency Non-Resident Account (FCNR) and a fixed deposit account. You can deposit your earnings from overseas or transfer funds from one NRE to another NRE account and in certain cases, from NRO to NRE account along with form 15CA/CB. The foreign currency deposited into the NRE account gets converted into Indian rupees.

An NRE account comes with many benefits. Bhat says, “Most important benefit is the principal and interest income are fully repatriable, that means you can move it out of India, as per your will and you don't need anyone's permission to repatriate this money.” He adds that interest income on deposits earned in an NRE account is tax-free. You can also link your NRE account to make investments in India.

From an overseas bank account in developed countries like the US, the UK and Canada, you can do a SWIFT transfer into the NRE or NRO account you hold. Whereas Gulf countries like Kuwait, Oman, Qatar, Saudi Arabia and UAE also rely on exchange houses besides SWIFT to remit funds to your NRE or NRO accounts. SWIFT is a messaging network banks use for quick money transfer instructions. “You need to give justifications to your overseas bank for moving the money to India,” says Diwanji.

“Documents required depend on the purpose of remittance and charges are based on type and amount of transfer,” adds Satheesh Krishnamurthy - EVP & Head – Private, Premium Banking & Third-Party Products, Axis Bank. For instance, money sent as family maintenance typically requires no documents, whereas, for equity investments, certain declarations may be required.

There are no charges by the banks for inward remittances in India. But the overseas bank will charge you for this transfer through SWIFT. NRIs can also deposit foreign currency brought to India during their visit to NRE accounts.

Also read: Transferring funds abroad or using cards overseas? Be aware of hidden charges on forexAs an NRI can I transfer funds from my NRO account to NRE account?The ideal way to remit funds is through an NRE account, which is fully repatriable. Yes, you can also transfer money from your NRO account to NRE account. “It is a legitimate route that an NRI can move money to the home country,” says Diwanji.

There are multiple reasons to transfer money to an NRE account. You might need to transfer your income in Indian currency and withdraw to meet investments and expenses in your preferred currency abroad. You might want to keep an NRO account only for collecting the Indian income and manage all investments in an NRE account that allows you the flexibility of full repatriation when you need the funds. “You need to submit the request along with Form 15CA/CB,” adds Krishnamurthy. The USD 1 million per year limit applies for NRO to NRE transfers too.

Choosing between NRE and NRO account for your investments“By nature, NRE account is suitable as the amount lying unutilised in your NRE savings account earns interest, which is tax-free and if savings are placed in a fixed deposit then NRE FD interest is also tax-free,” says Kalpesh Ashar, Founder, Full Circle Financial Planners and Advisors. Additionally, if the investments are done in capital markets, the repatriation back to a foreign country is easy without any permission through NRE account rather than NRO account.

Which is the best bank for opening NRE/NRO accounts?Jain suggests that banks with good digital systems and online presence should be chosen over those that are weak on such issues. “As an NRI customer, you spend most of the time overseas. Digital accessibility of your account is therefore important,” says Jain. Check a bank’s ease of account opening and operations.

Further, in India, the bank should offer you a relationship manager and a branch should be located in your vicinity for various services.

“While evaluating you should look for banks that offer a full suite of digital options in order to take care of remittances within and outside India, bill payments, debit/credit card facilities, loans, insurance, investments, etc,” says Krishnamurthy.

As you are depositing your finances in these accounts, also look for security and fraud protection from banks.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.