Your salary slip not only tells you of what you earn but also the tax you end up paying.

Basic pay, Employees' Provident Fund (EPF), National Pension System (NPS) and allowances are not treated the same under the new and old tax regimes, and the difference can change your tax bill.

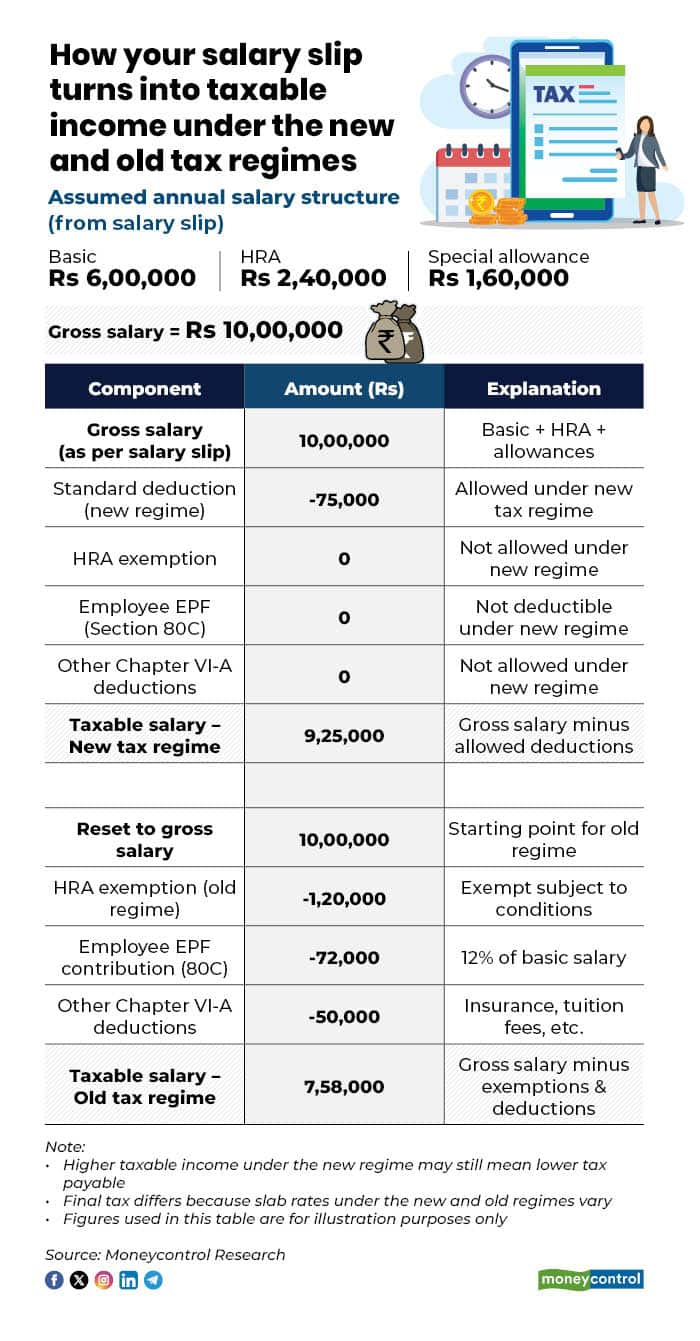

You must look beyond the net salary and break down each component in your salary slip to see what is taxable, what is exempt and what no longer gets a benefit under the new regime.

Chartered accountant Suresh Surana said, "Under the new tax regime, income tax is levied on the total taxable income, i.e. in the given case, computed under the head 'salaries' and not on the net pay reflected in the salary slip."

All salary components such as basic, HRA and special allowance form part of gross salary, from which only specifically permitted deductions (such as the standard deduction, where applicable) are allowed, he said.

Employee contributions to EPF are not deductible under the new regime and employer EPF contributions are taxable only if they exceed the prescribed threshold — if such contribution exceeds 12 percent of salary subject to the aggregate limit for NPS, recognised provident fund and superannuation fund of Rs 7.5 lakhs.

On the other hand, under the old tax regime, exemptions such as HRA and deductions like EPF under Section 80C may be claimed, subject to conditions, Surana said.

Accordingly, taxable income must be determined by analysing the salary structure and applicable provisions rather than relying on the net pay shown on the salary slip.

To determine how much income is taxable under the new and old tax regimes, separate gross salary components, exemptions and allowable deductions in accordance with the provisions of the income-tax law.

Step 1: Identify gross salary

Gross salary comprises all monetary components reflected under earnings in the salary slip, such as basic salary, HRA, special allowance and any other taxable allowance. This represents the starting point for computation under both tax regimes.

Step 2: Compute taxable salary under the new-tax regime

Under the new tax regime, most exemptions and deductions are not available.

All salary components, including HRA and allowances, are fully taxable.

Only specifically permitted deductions such as the standard deduction are allowed.

Employee contributions to EPF and most deductions under Chapter VI-A are not deductible.

Taxable income is determined by reducing only the permitted deductions from gross salary.

Step 3: Taxable salary under the old-tax regime

Under the old tax regime, the salary slip is analysed to identify:

Exempt components, such as HRA (subject to prescribed conditions)

Eligible deductions, including employee EPF contribution under section 80C and other Chapter VI-A deductions.

Taxable income under the old regime is arrived at by reducing eligible exemptions and deductions from gross salary, subject to statutory limits and conditions.

Step 4: Compare the two regimes

The difference in taxable income between the two regimes arises from the availability of exemptions and deductions under the old regime, most of which are not available under the new regime. Taxpayers must compute taxable income under both regimes using the salary slip, then determine which regime yields lower tax liability.

Thus, taxable income is determined by starting with gross salary as per the salary slip and applying regime-specific exemptions and deductions, rather than relying on the net pay shown on the salary slip.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.