Filing of income-tax returns is mandatory. But did you know that even the dead have to file their income-tax returns? As per the income-tax rules of India, a deceased person’s income-tax returns must be filed for the year in which the person died. Although this is an old rule, not many of us know about it. And in a year where the deadly Coronavirus has claimed 118,534 lives in India, it’s important that we understand how to file tax returns for our departed loved ones. Here’s how you should file returns for the deceased.

Also read: Income tax return filing | Why you should pay your taxes now despite deadline extension

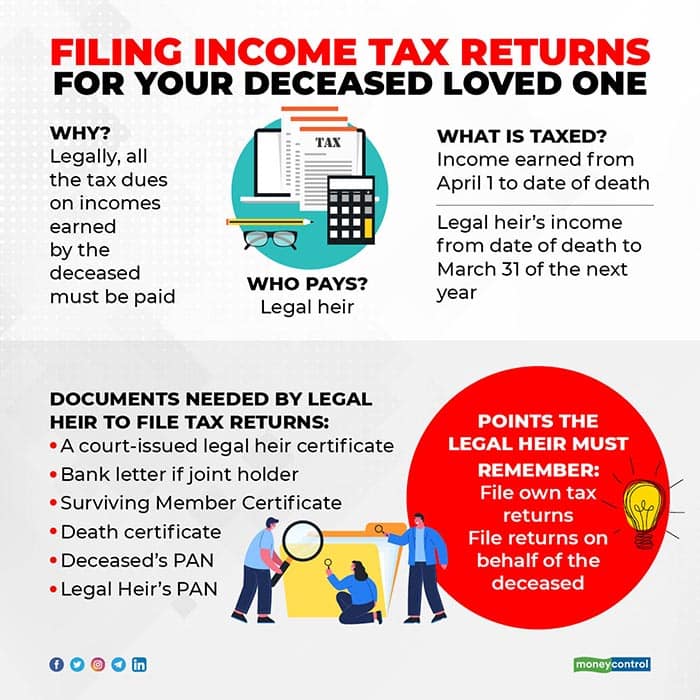

Two returns to be filed, not oneTo begin with, you need to file two income-tax returns. Let’s suppose a person died on October 7, 2020. One return is for the income earned from the start of the financial year (April 1, 2020) to the date of death (October 7, 2020). And the second income-tax return must be filed for income earned by the deceased from the date of her death (October 7, 2020) to the end of the financial year (March 31, 2021). Irrespective of whether the departed one had made a will, the legal heir has to file the first return and the executor has to file the second return. The executor files the second return because she executes the will of the deceased and is in charge of paying off liabilities, if any, of the deceased such as taxes, loans and so on. “A PAN for the estate of the deceased too needs to be obtained,” says Ameet Patel, partner at Manohar Chowdhury & Associates.

Also watch: How to make a willThe legal heir, meanwhile, also has to file his own tax returns for his own income. That is separate.

But you cannot just log in to the income-tax filing website and try and file the tax returns. These days with our permanent account number (PAN) and Aadhaar numbers linked to our various investments, it’s easy for the tax authorities to know if the person in whose name the returns are filed is actually dead, since you need Aadhaar to get the death certificate. Karan Batra, founder and CEO of Chartered Club shares the tale of someone who tried to file income-tax returns on behalf of his deceased father. “He got a notice that since the person is dead, how could the income tax return be filed? The Aadhaar number is mentioned while procuring the death certificate, while the income tax details too are linked with Aadhaar,” he said.

The logic is: if the person is dead, he cannot file his own income-tax returns. “He filed the return in his father’s name, which is not the correct way to file the return,” says Patel.

That’s why the returns need to be filed in the name of the legal heir and the executor.

Also read: 7 tasks to complete for settling money matters after the demise of a loved one

Legal heir must register on income-tax payment portalBefore the legal heir files the tax returns on behalf of the deceased, she must get herself registered on the income-tax website. Experts say that the procedure can get a bit lengthy. New-Delhi resident Karan Sood had a hard time understanding the procedure for filing a return as a legal heir for his father, who passed away in February 2017. Nudged by a compliance notification that popped up in his father’s email account due to fixed deposits being traced by the income tax department, he decided to follow up through chartered accountants and even some income tax officials. “My mother was registered as a legal heir through an online procedure executed on the income tax e-filing portal. It was rejected once and upon re-filing was accepted after a few weeks,” says Sood.

Also read: Despite having nominees, death claims can be delayed by banks

However, by the time he could understand the procedure and wrap up the paper work, the extended deadline for filing the tax returns for his now deceased father had elapsed. For the assessment year 2017-18 (financial year 2016-17) he could have filed the return by July 31, 2017 without penalty and March 31, 2018 with penalty. Beyond March 31, 2018, the tax return for the income earned in 2016-17 cannot be filed.

He was left with no option, but to merely calculate the tax payable along with the late payment interest and penalty. He has preserved the receipt for the same. He suggests that an offline procedure to file the tax returns of the deceased during an extended window should be provided as the procedural delays and state of ignorance leaves the family with hardly any time to file the returns, especially during times of grief.

Though he had to pay a balance tax amount of Rs 30,000 including the penalty and interest, there is no way to claim the refund for the tax deducted at source on the fixed deposit, through which the income tax department originally traced non-filing of income tax return. That’s because to be able to claim a refund, you need to first file income-tax returns. And you cannot file tax-returns after due date.

To reduce the woes of the survivors, recently courts have ruled: if the deceased has a joint account with the legal heir “…then a letter from the bank stating that the person has been a joint account holder with the deceased, serves as a nomination for legal heir,” says Patel.

Escape from filing returnIn Sood’s case his father’s income was reflected in his Form 26AS due to tax deduction for fixed deposits. But if there is no such taxable income or refund to be claimed, then you need not go through the cumbersome procedure. “If there is no income in the name of the deceased then there is no need to file the return. Even the return as an executor to the estate is not needed if all the assets have been transferred to the legal heir. However, sometimes shares aren’t transferred, bank accounts are not closed and estate is not transferred. That is when the second return needs to be filed for the estate of the deceased person,” Patel explains.

Similarly, all the due taxes need to be paid by the legal heir.

Another word of caution is that if you have any tax refunds pending in the name of the deceased, then do not close all the bank accounts in the deceased’s name, especially the one notified as the primary account in the income tax records. If there is a joint account of the deceased with the legal heir, the same too shouldn’t be immediately closed for easier documentation and procedural issues.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.