With the festive season in full swing, as the country unlocks amidst the COVID-19 pandemic, e-commerce companies such as Flipkart and Amazon, and other retail stores are enticing shoppers with lucrative deals. The Indian economy is steadily moving towards normalcy and banks are seeing the early signs of a revival in consumer confidence and demand. So, to woo customers, most banks such as Kotak Mahindra Bank, HDFC Bank, ICICI Bank, State Bank of India (SBI) and Bank of Baroda have partnered with leading retail chains and established e-commerce websites with offers for debit and credit cardholders. Banks have introduced various discount and cash-back offers for their customers. But, a popular scheme catching the attention of buyers is the 'no-cost EMI.'

What is a no-cost EMI?No-cost EMI schemes are loan offers in which the buyer of a product or service just pays the selling price of the product in equal instalments. Gaurav Gupta, co-founder and CEO of MyLoanCare.in says, “In this scheme, there is a subvention of the interest component by the manufacturer or merchant, either in the form of an upfront discount or as a cashback to the buyer. That subvention is only for the period which is originally contracted as per the agreement made during purchase.”

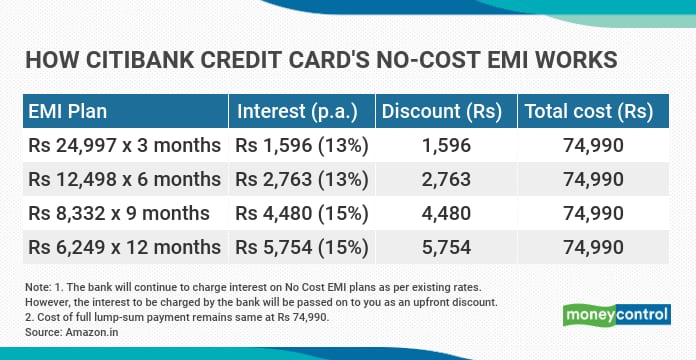

How does the scheme work?Suppose, you purchase a laptop for Rs 74,990 and opt for a ‘no-cost EMI’ scheme of 12 months’ tenure on your Citibank card. The total amount to be paid will be the price of the product, split equally across the EMI tenure, i.e., Rs 6,249 for 12 months. Generally, your bank will charge you interest. However, this interest charge has been provided to you as an upfront discount at the time of your purchase (as illustrated), effectively giving you the benefit of a no-cost EMI. So, when you take the no-cost EMI option as shown in the table, you end up paying Rs 5,754 as interest, which is included in the monthly instalment.

Says Gaurav, “If you hadn’t opted for the no-cost EMI scheme, you may have got a discount from the seller’s partnering bank, on the product or some sort of cashback. In a no-cost EMI scheme, you lose out on cash discounts being offered.” Also, you have the option of negotiating with a retailer and demanding an upfront discount instead of taking a no-cost EMI. This option is not available while shopping on e-commerce portals.

Are there any additional costs?When you opt for ‘no-cost EMI’ schemes, depending on the product and the offer, you may not get certain upfront cash discounts associated with them when you purchase it from retailers. “Also, you may end-up paying additional costs such as goods and service tax (GST) on each instalment, as well as processing charges,” says Adhil Shetty, CEO of BankBazaar.com. For instance, HDFC Bank and Kotak Mahindra Bank charge a processing fee of Rs 199, which will be billed in the first repayment instalment for the no-cost EMI transaction. The GST on the purchases will be over and above the product price every month in your card statement.

How do I avoid a debt trap with the 'no-cost EMI' scheme?As attractive as the scheme may appear, it can turn out to be a debt trap for borrowers and buyers. If you default on your credit card dues, which include this instalment, then you may end up paying penalty charges to the bank and additional interest charges (2-3.5 per cent per month), as applicable on the outstanding balance of the card. Skipping even a single EMI will mean that you lose the discount at the time of purchase, in addition to facing more charges.

"No-cost EMI schemes are nothing but a reinvented version of zero-interest schemes that were introduced by retailers a few years back and were clamped down by the RBI for their non-transparent terms and hidden charges. The purchase price tends to be higher in these schemes than what you may pay for an instant cash purchase,” says Gaurav. So, in essence, you are trading a discount for the no-cost EMI scheme.

“Like any other loan, buying a product on no-cost EMI needs to be repaid on time, in full. In case that does not happen, it can affect your credit score and bar you from taking further credit,” says Shetty.

“This festive season, if you plan to shop for a high amount, compare the prices among retail outlets to figure out if they offer an upfront discount and if the total cost is lower than that on e-commerce websites,” Harshil Morjaria, a certified financial planner at ValueCurve Financial Solutions. If this discount can bring down the actual purchase price and you can afford a one-time outgo without stretching your cash flows, you would be better off with a one-time payment. On the other hand, if you need the product, but your constricted cash flows make it unaffordable as a single lump-sum, you can opt for the no-cost EMI scheme.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.