A personal loan could be effective to meet various financial needs during a cash crunch. Availing a personal loan has become convenient with the advent of complete digital processes. You can apply for a personal loan and get approvals within a few minutes using your mobile phone.

With the availability of a wide range of options from banks and non-banking financial companies (NBFCs) it could be difficult to choose the best personal loan as per your needs. Let’s consider the key factors you should keep in mind while selecting the best personal loan offer.

Key factors to consider before finalising a loan offer

Understand your financial needs: Before diving into the various personal loan options, it is important to understand your financial needs. Why do you need the loan? Is it for paying off an existing loan, a major purchase or an emergency? Knowing your purpose will help you in choosing the loan amount and repayment schedule. For instance, if you’re looking for debt consolidation, you’ll need a personal loan that offers a lower interest rate than your existing debts. On the other hand, you would need quick approval and disbursal in the event of an emergency.

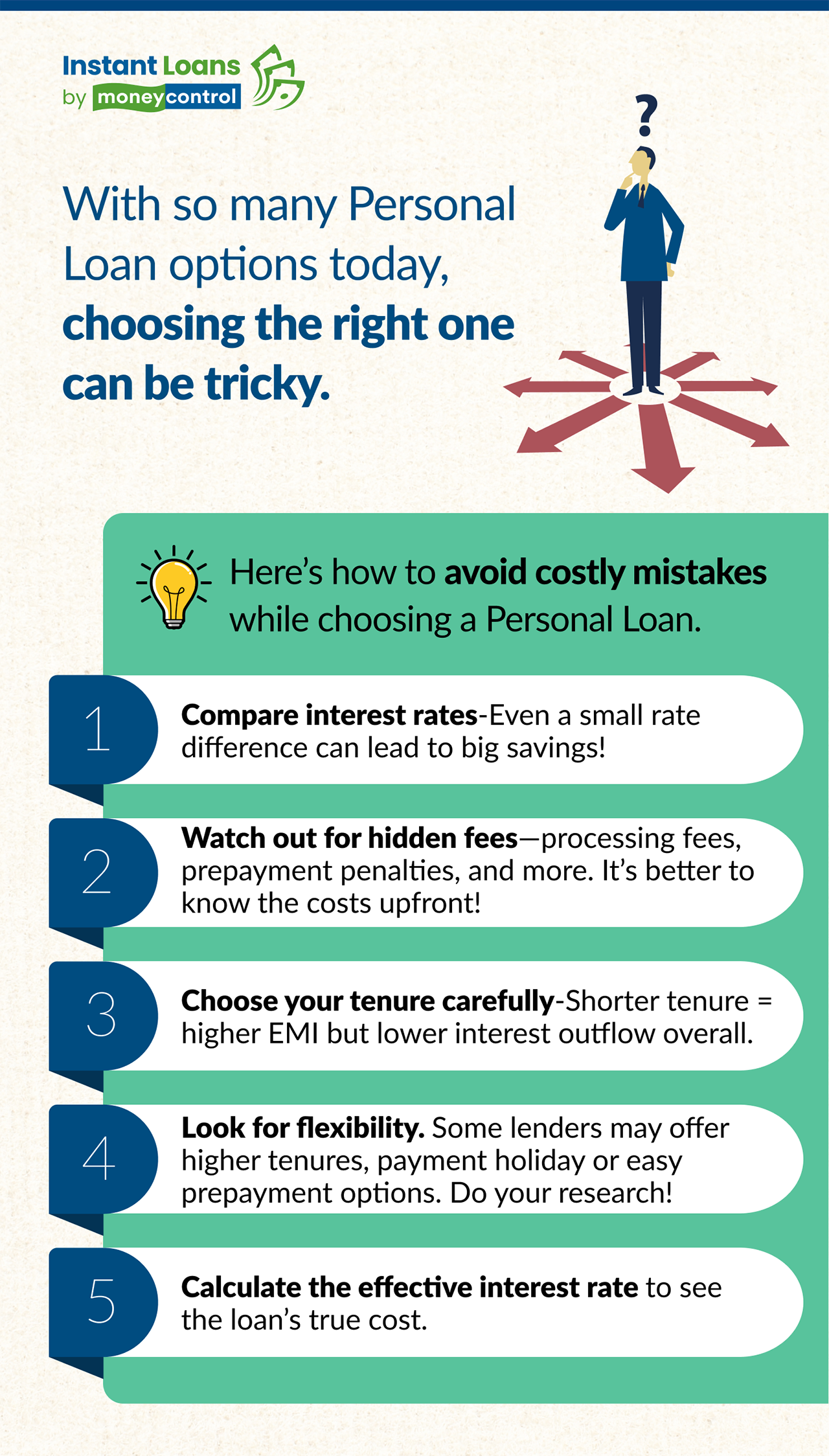

Compare interest rates: One of the most important things to consider while choosing the best personal loan is the interest rate. To ensure hassle-free loan repayment, you need to identify the best personal loan interest rate as it could turn into a financial burden later. Interest rates can vary significantly depending on the lender and even a marginal difference can save you a substantial amount. For example, if you borrow ₹10,00,000 over five years, the difference between a 10% and an 11% interest rate might seem minor, but it can result in a difference of several thousand rupees in terms of interest payments.

Check the available loan tenures: The loan tenure, or the period over which you’ll repay the loan, is another important factor. Usually, lenders offer personal loans for tenures ranging from 12 months to 60 months. While a longer tenure may result in lower equated monthly instalments (EMIs), the interest component will be higher. On the other hand, a shorter tenure will result in higher EMIs but total outgo towards interest charges will go down.

Check fees and charges: Apart from the interest rate, there are other fees and charges associated with a personal loan. Processing fees, late payment charges and prepayment penalties are a few examples. You need to factor in these costs while choosing the best lender for a personal loan. For instance, some banks charge a processing fee of 1% to 2% of the loan amount, which might add up to a significant amount while others levy a fixed amount for the same.

Go through loan eligibility criteria: Every bank has its own eligibility criteria for personal loans. This usually includes your credit score, income level, employment status and age. Make sure you meet these requirements by double-checking them before applying. A good credit score (above 700) can help you secure the best personal loan, including a lower personal loan interest rate.

Check time for loan disbursement: How quickly the loan is disbursed is another factor to consider. Some banks offer instant approval and disbursement, while others may take a few days.

Use a personal loan calculator: A personal loan EMI calculator is a very useful tool that can help you understand the financial implications of your loan. By entering the loan amount, interest rate and tenure, you can see how your monthly payments could vary. Moreover, using the personal loan calculator feature can help you compare different offers from various banks, making it easier to choose the best bank for a personal loan.

Enquire about the customer service: The quality of customer service a lender offers can make a huge difference. Consider how easy it is to reach a lender’s customer service team, the availability of online support, and the clarity of their communication. A lender that offers excellent customer service will make the process of managing your personal loan much smoother.

Read the terms and conditions: Make sure you read the loan’s terms and conditions in its entirety. It may contain important information that generally borrowers don’t check in detail, such as how interest is determined, what happens if you miss a payment, or what happens if you want to close the loan ahead of the tenure.

Mistakes you need to avoid while applying for personal loan

Not evaluating your options: This can be a costly mistake since the interest rates offered by lenders can vary significantly. Also, if you are in need of funds urgently look for lenders that provide quick disbursal.

Ignoring the fine print: Make sure you know the terms and conditions associated with the loan you are availing. The least you should be aware of is the interest rate, fees, repayment terms and foreclosure options.

Borrow more than you need: Availing a higher loan just because it is offered can be troublesome if they stretch your repayment budget. It can result in missing payments and eventually damaging your credit score.

Applying for a personal loan via Moneycontrol could be a suitable option for those looking for a 100% digital loan approval process. It offers instant personal loan approval for up to Rs 15 lakh via top lending partners. The application process is simple:

Start by providing basic information to check your personal loan eligibility.

Next, confirm your identity by completing the KYC process.

Taking a personal loan is a big financial decision that you should make after considering all aspects of your financial needs. Evaluate all the options available in the market rather than relying on the first option you come across. With the availability of online personal loan apps, getting a loan is easy and quick. Manage it responsibly to make the most of it.

Summary

Choosing the best personal loan can be tough with so many options available. It's important to understand your needs, compare interest rates, and review loan terms carefully. Don't forget to consider your repayment budget, fees, and eligibility criteria before applying.

Disclaimer

This piece/article was written by an external partner and does not reflect the work of Moneycontrol's editorial team. It may include references to products and services offered by Moneycontrol.

100% Digital

100% Digital Quick Disbursal

Quick Disbursal Low Interest Rates

Low Interest Rates