Manish Kothari

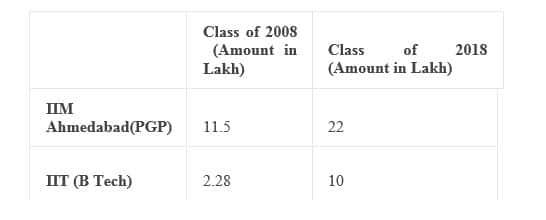

A continuous rise in education costs in India has been a worrying point for most parents. Relying solely on an education loan burdens the child financially, resulting in lesser room for the child’s individual savings in the initial stages of their career. To avoid lack of funds becoming a hindrance to their child’s education aspirations and professional journey, parents must save for their child’s education as early as possible. For example, fees in one of India’s most premier institutions the Indian Institute of Management,

Ahmedabad has doubled in the last 10 years.

The best way to tackle increase in the cost of higher education is through investments in mutual funds through systematic investment plans (SIPs). The latter allows wealth generation through systematic regular investments on pre-determined dates over a period of time to achieve the desired corpus when the period ends.

Here is how to go about funding your child’s education through SIPs:

Start investing early: When parents start investing early through SIPs they allow more time for their money to grow. Also, the monthly outgo in the form of SIPs is lower than for those investing late for the same amount of corpus. For instance, if one wishes to accumulate a corpus of Rs 50 lakh when your child reaches 18 years of age, with the assumed rate of return being 12%. If one starts investing when the child is eight years old, one would have just 10 years to build this corpus with a monthly SIP of Rs 21,000. However, if the investment starts when your child is three-year old, you would have an investment horizon of 15 years which will lead to a monthly SIP of just Rs 10,000.

Calculate the corpus required: Parents need to calculate the corpus amount before investing, based on current possible career options. However, make sure that while calculating this amount, existing as well as the expected inflation rate is taken into account. Do not commit the mistake of calculating the education corpus based on just present education costs as this is likely to lead to an insufficient corpus. Calculating the corpus helps in analysing the monthly payout through SIPs till the time your child reaches 18 years of age. Make use of SIP calculators available online to know how much amount one would need to pay monthly to accumulate the required amount of corpus.

Go for zero commission direct plans: Direct plans enable investors to buy mutual funds directly from fund houses without the involvement of financial intermediaries and without incurring expenses associated with them. Their lower expense ratio, higher net asset values (NAVs) and greater returns make it a better option than regular plans. Even first time investors looking to start SIPs to fund their child’s education can choose to purchase direct plans through online marketplaces that can guide you and provide free advisory services.

Build portfolio according to risk appetite: Parents need to select the right funds for their investments. Every investor has a different risk appetite which anchors their decision while building their portfolio. Ideally, one's core portfolio should include a few top multicap funds as these funds can invest in shares of large, mid and small sized companies, and are thus able to align themselves as per changes in market conditions. Including a couple of midcap funds can boost the growth rate of your education corpus. However, if the risk appetite for equities is low, consider sticking to largecap funds. Select funds that have consistently beaten their benchmark indices and peer funds over the last 3-5 years.

Increase the SIP amount whenever possible: After deciding on the SIP amount, make sure to review it periodically and increase it whenever one has additional funds to do so, by using the step-up facility. Ideally, you should increase the SIP amount every year as one's income goes up. This contributes in the long run as one would be able to accumulate a larger corpus since the SIP amount keep increasing by a definite percentage every year, or whenever one has funds to increase it. Many fund houses are offering the option of half yearly or yearly top-ups to investors at the time of filing their SIP enrolment forms.

Track the funds’ performance periodically: Make sure to keep track of the chosen funds’ periodic performance. Exit funds which have been underperforming consistently for about 2-3 years, have changed their management style or fund managers. Regularly compare one's existing fund’s performance with the benchmark and other funds in its category to evaluate performance. If it is performing satisfactorily, hold on to it, otherwise one must consider switching to some other better performing fund to prevent any damage to your corpus creation process. Merely investing in mutual funds and not tracking them may lead to failure in accumulation of the desired corpus due to various reasons.

Separate them from other investments: Another important aspect to keep in mind while managing a child’s higher education funding is to separate this goal and its investment from other investments. Make sure one doesn’t compromise on this goal to fulfil any other goal. Keep investing through SIPs regularly for the set horizon of 10-15 years (as per your child’s age) in order to build the desired amount of corpus. Even if one invests for other goals such as child’s wedding or one's retirement, do not disturb the SIPs of any other investments. Make sure you don’t skip any SIP and pay them regularly for the entire time period.

Take term life insurance: Term life insurance provides an assured amount to your family in case of your untimely demise. This ensures that the financial needs of the family and child aren’t left uncovered. The insured amount helps in continuation of SIPs for building the child’s higher education corpus. Besides investing in SIPs for your child’s higher education corpus, make sure one avails a term insurance as well to ensure SIPs continue even after your demise.

The writer is Director & Head of Mutual Funds at paisabazaar.com

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!