Highlights - Tewoo Group’s debt recast proposal has been rejected by investors - Largest default by a state-owned company in China - Recently, Peking University also missed interest payments - Three regional banks have collapsed since May

-------------------------------------------------

Chinese commodities trader Tewoo Group has become the first Chinese state-owned company in two decades to default on its US dollar -denominated bonds. While the government is taking measures to alleviate the debt market stress through fundraising and interest rate cuts, delinquencies continue to rise as China is witnessing its worst economic slowdown in nearly three decades. Tewoo’s default signals that corporate stress has aggravated further and the Chinese government is finding it difficult to contain credit risk in a weakening economy.

Company backgroundBased out of Tianjin, Tewoo is a material circulation company. It is a bulk trader of commodities such as metals (ferrous & nonferrous), energy, minerals and chemicals. Besides commodity trading, the company has presence in other areas such as infrastructure, logistics, real estate, autos and financial services.

In 2017, it had a turnover of $66.6 billion with profits of $122 million and was ranked 129th in the Fortune Global 500 list & 28th in the Chinese enterprises list. The company employs more than 19,000 professionals and has operations across the US, Germany, Japan and Singapore.

Funding crunch linked to business associateTewoo’s financial challenges are closely linked to Bohai Steel Group, a business associate which has filed for liquidation due to high leverage. Bohai’s bankruptcy in 2018 triggered systemic risk in Tianjin’s financial market and Tewoo has been facing serious liquidity challenges in recent months. The group’s financial difficulties came to the fore in April when it approached lenders for a debt recast and sold copper at below market rates market to ease the cash crunch. Consequently, Fitch Ratings downgraded the company by six notches in one go.

In the last week of November, Tewoo had proposed its lenders take a huge haircut on the bonds or accept delayed repayment at reduced coupon rates. The 14-day deadline for accepting the proposal expired earlier this week and only 57 percent of the investors had accepted proposal. Less than 100 percent acceptance is termed as a failure and this means that the company will miss interest payments due 16 December on $1.25 billion worth of bonds.

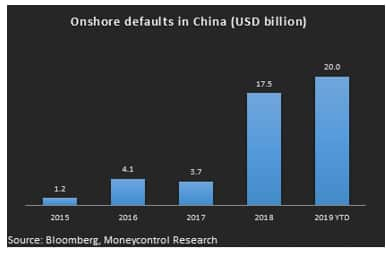

Banks suffer as NPAs riseTewoo’s liabilities are pegged around $36 billion including $2 billion of foreign debt. While the amount is small compared to China’s overall economy, the quantum of bad debt is mounting. Last week, another Chinese state-owned conglomerate Peking University Founder Group skipped payments on $284 million bonds. In total, Chinese corporate borrowers have defaulted on nearly $20 billion this year. The pace of defaults has picked up in recent weeks and fears of contagion are rising as around 15 defaults have been reported since the start of November. The list covers a broad spectrum of industries from real estate to metal to manufacturing and automobiles. The liquidity crunch, which was earlier restricted to private companies, has now spilled over to state-owned enterprises (SOEs) and even universities. In fact, the non-performing asset ratio for private Chinese companies has surged to an all-time-high of 4.5 percent in 2019.

The stress on corporate debt has resulted in three regional bank failures in recent months. The collapse of Baoshang Bank in May 2019, a small regional bank with $90 billion in assets, was the first bank failure in over 20 years. A couple of months later Bank of Jinzhou was bailed out by three state-controlled asset managers. Last month, Hengfeng Bank joined the list raising concerns over the financial stability of the entire banking system in China.

Investments in state-backed or state-owned companies are considered safe-havens as these are backed by the full faith and credit of the government. So, Tewoo’s case can be termed as a sovereign default and failure to repay foreign investors’ money can have major repercussions on the influx of fresh capital into the Chinese economy. Emerging markets such as China are dependent on foreign investors for their funding requirements and capital outflows can result in currency depreciation and further weaken the financial system. The situation is similar to the IL&FS default in the domestic market – which triggered the liquidity crisis in India and resulted in an intense slowdown in the country’s growth rate.

China’s situation remains tricky. The trade war with the US is hurting businesses and macro-economic conditions are deteriorating across the globe. Corporates across the world are facing an uphill task of maintaining their profitability and managing their interest payments. As per S&P Global, foreign denominated debt maturities for Chinese companies stands at $90 billion and $100 billion in 2020 and 2021 respectively. In addition, these companies need to repay around $700 billion in local debt each year – for 2020 and 2021. Investors should remain risk-averse and keep a close watch on such major developments in bond and credit markets – which influence both the flows and returns of equity markets.

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.