Sachin Pal

Moneycontrol Research

Highlights:

- The building materials retailer’s stock has corrected 75 percent

- Profitability in H1 was subdued due to multiple factors

- Working capital has deteriorated in the past 1 year

- Change in business strategy to impact margin

- Valuations still rich at 24 times FY19 estimated earnings

-------------------------------------------------

Home improvement and building products retailer -- Shankara Building Products -- had a phenomenal run last year. The company received a tremendous investor response at the time of its initial public offer (IPO) in April last year and the stock turned out to be a multi-bagger in a short span of time. However, much has changed since then. Recent developments, related to its business outlook, has resulted in a market capitalisation (mcap) erosion of over Rs 3,000 crore as the stock price has seen a steep (nearly 70 percent) correction from its 52-week high. We look at the business fundamentals as well as industry dynamics to check if the business makes a case for investment at this point in time?

Health topline growth but margin take a hit

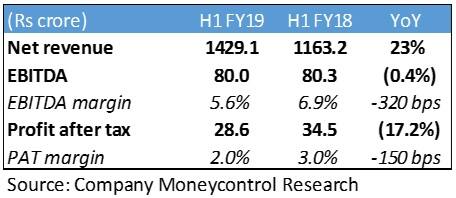

During April-September, the company reported healthy topline growth (up 23 percent year-on-year). This was aided by strong revenue growth across retail and enterprise segments. Lower processing margin and inventory losses resulted in a subdued operational performance. Profit after tax came in 17 percent lower due to higher depreciation and increase in interest expenses.

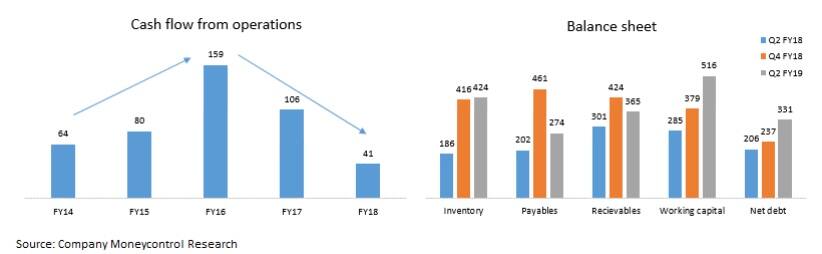

Increase in working capital is a big concern

While the profit and loss (P&L) appears to be fine, the real problem lies in the balance sheet and cash flow statements. Cash flows appear to have peaked out before the IPO and have been on a significant decline ever since. Between Q2 FY18 and Q2 FY19, working capital (inventory + payables – receivables) has almost doubled to Rs 516 crore. Increase in capital requirements has been financed through long and short term debt, which has ballooned from Rs 206 crore to Rs 331 crore over the same period.

In H1 FY19, the company reported a 37 percent jump in retail sales to Rs 745 crore. Increase in retail share should ideally result in an improvement in working capital days, but this does not seem to be the case with Shankara.

Also, the company has intangibles assets worth Rs 22.5 crore on its balance sheet. This amount needs to be amortised over the next few years and is nearly equivalent to two quarter profits.

Targeting retail expansion at the cost of margin

In a conference call after the Q2 result, the management said the company is targeting market share gains in the retail segment through competitive pricing. Going forward, it has guided at 20-25 percent growth in retail sales (versus 37 percent in H1 FY19) with an operating profit margin of 6-8 percent (versus 10 percent in H1 FY19). Based on the guidance, profitability is set to take a big hit as this implies a lower sales growth along with a sharp contraction in operating margin.

Demand for building materials remain muted

Building material companies are operating under competitive industry dynamics. While demand from the infrastructure segment has been fairly robust, subdued demand from the real estate is impacting overall growth for the sector.

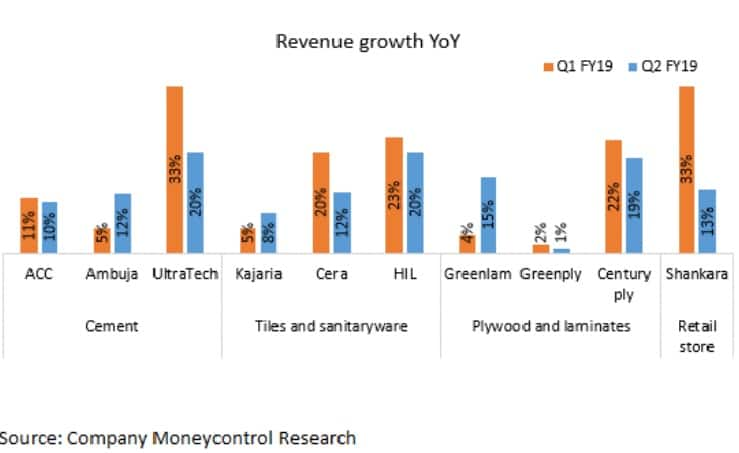

UltraTech Cement’s headline revenue growth of 23 percent was primarily aided by acquisition and ramp-up of the cement assets of JP Associates. In terms of topline, the selected players (see chart below) had a median revenue growth of 11 percent and 12 percent for the first two quarters, respectively. On the profitability front, margin continue to remain under pressure on the back of higher input prices. Sharp jump in crude oil and adverse currency movements had a significant impact on the bottomline of companies across sectors.

For Shankara, topline growth of 33 percent in Q1 was much ahead of the industry, although this was aided by a favourable base. However, sales growth in Q2 seemed in line with the industry.

So, what should investors do now?Overall demand for building materials is anticipated to be muted for the next two quarters due to growing concerns of economic slowdown as well as upcoming elections.

Assuming profit of Rs 50 crore for the full year (versus Rs 29 crore in H1 FY19), Shankara’s stock (CMP: Rs 521) still trades at a FY19 price-to-earnings multiple of 24 times. Despite a sharp correction, the stock does not appear cheap at current levels. The business seems to be going through a transition and is facing twin challenges in the form of declining profitability and worsening balance sheet. The earnings visibility remains bleak in the current market environment and balance sheet repairing will take at least 2-3 quarters. We would advise investors to wait on the sidelines until the company shows visible signs of an improvement on the operational front.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!