Neha Dave

Moneycontrol Research

HDFC Bank, one of the largest and most profitable private sector banks, posted yet another quarter of strong performance backed by healthy loan book growth. Though the headline number for the June quarter was slightly lower than street expectations, core operating numbers, excluding one-off investment, were strong. We see Q1 as a speed breaker, not a derailment, in the bank’s upward journey.

In the current scenario, where public sector banks are saddled with huge non-performing assets and constrained by lack of sufficient capital, we expect the bank to strengthen its corporate lending by gaining market share from public sector banks while maintaining its leadership position in the retail segment.

We see the bank churning profitable growth over the next few years as it enjoys dual moats (competitive advantage) on both the asset as well as liabilities side with high margin retail loans constituting 55 percent of its total loan and low-cost current and savings accounts (CASA) accounting for 42 percent of total deposits.

Quarter at a glance

HDFC Bank’s Q1 FY19 numbers were consistent, except for the marginal blip in topline growth. Net interest income (NII, difference between interest income and expense) increased 15 percent year-on-year driven by robust loan book growth, but was partially off-set by fall in net interest margin (NIM) to 4.2 percent, down 20 bps YoY.

Other income growth was muted at 9 percent YoY as strong growth in core fees income was partially negated by loss on revaluation and sale of investments. The 23 percent YoY growth in fees and commission income was underpinned by growth in fees on third-party distribution of financial products, processing fees and credit card charges. Despite having an option to spread the provisions for mark-to-market (MTM) investments losses equally over 4 quarters, the bank chose to recognise the entire MTM loss of Rs 391 crore in the quarter gone by.

Operating leverage improved significantly as the core cost-to-income declined to 40.1 percent as against 42.7 percent in Q1 last year, led by controlled branch network growth and digital initiatives. The bank continued to maintain its impeccable asset quality with gross and net non-performing assets at 1.33 percent and 0.41 percent, respectively, as at the end of June. Provision coverage ratio at 70 percent was healthy. If we include the floating provisions of Rs 1,451 crore, coverage is more than adequate at 118 percent of gross non-performing loans.

Overall, Q1 profit was mainly dragged down by treasury losses and margin compression.

The fall in margin doesn’t concern us much as we expect loan book to get repriced upwards as higher-cost deposits transmit to higher marginal cost of funds based lending rate (MCLR). If we exclude the MTM losses, profit before tax (PBT) growth would be 29.7 percent YoY, much better than the reported growth of 18 percent.

Robust loan book growth; size not a deterrent

Total advances increased 22 percent YoY to Rs 708,649 crore as of June 30. Within total advances, retail loans witnessed 22 percent YoY growth, while wholesale loan book constituting corporate lending grew 23 percent.

Deposits growth increased 20 percent YoY. Growth in time deposits was much stronger at 25 percent YoY compared to CASA deposits growth of 17 percent. As a result, CASA ratio dipped marginally to 41.7 percent as compared to 44 percent in the last quarter.

The bank’s performance is commendable as it continues to grow its loan book at almost double the system average despite the higher base. Last fiscal (FY18), its share in incremental deposit and credit growth stood at 20.2 percent and 12.8 percent, respectively, clearly showing how the bank is capturing market share when competitors are vacating the same on account of their weak capital position and burden of non-performing loans.

Capital adequacy at 14.6 percent remained well above the regulatory requirement of 11.03 percent. The bank now has all approvals for raising capital. Last week, parent Housing Development Finance Corporation (HDFC) infused Rs 8,500 crore in the bank. HDFC Bank will raise the remaining Rs 15,500 in the due course. The capital raising will be a key catalyst for future growth and will adequately equip it to garner higher market share.

Subsidiaries gaining scale

HDFC Bank’s subsidiaries - HDB Financial Services (NBFC) and HDFC Securities (retail broking) – have witnessed robust growth over the past few years.

HDB Financial Services

HDB, with a presence in asset and consumer finance and business loans, is rapidly gaining scale. It is now present in 831 cities though 1,100 branches. HDB functions independently and caters to customer segment distinct to that of the bank.

Its loan book stood at Rs 44,469 crore as at the end of March and has grown at a compounded annual growth rate (CAGR) of 35 percent in the last 4 years. Profit more than quadrupled during the same period to Rs 952 crore. Though loan growth in Q1 was subdued at 8 percent YoY, we expect this subsidiary to gain further scale over the medium term due to immense growth potential in the sector and adequate capital support from the bank.

Value unlocking through the initial public offering of HDB is still some time away. Given its current size, we have assigned a value to HDB to arriving at its fair value for the HDFC Bank stock.

HDFC Securities

HDFC Securities is predominantly a retail broking entity with around 6.5 lakh active customers. Additionally, it distributes mutual funds and insurance, which contributes around 12 percent to total revenue. There is a significant room for growth for this subsidiary as well, as the number of active customers is only around 5 percent of HDFC Bank’s customer base. As such, we see steady growth in new customer additions, buoyant capital markets, and financialisation of savings aiding strong earnings growth over the next few years.

Valuation reasonable considering significant moat; earnings growth sustainableThe stock is up 16 percent year to date, while the Nifty is up by only 5 percent. Despite the outperformance, the stock is reasonably valued. It currently trades FY20e price-to-book ratio of 3.6 which is in line with its historical range. We have seen small and mid-size private banks with higher earnings growth getting sharply re-rated and enjoying premium valuation. As such, the valuation gap compared to some of these private banks has narrowed and looks relatively reasonable.

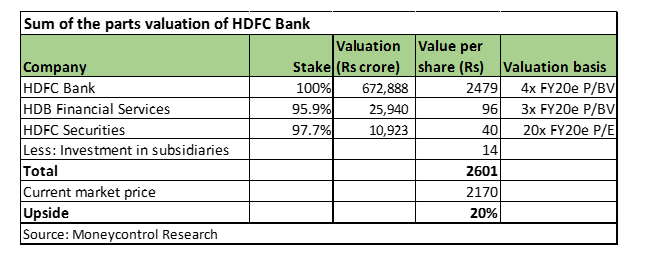

The equally strong performance of the bank’s subsidiaries - HDB Financial Services and HDFC Securities - also lends comfort. So far, the subsidiaries have aided bank’s earnings with dividends. They currently contribute around 5 percent to HDFC Bank’s valuation.

We have used sum of the parts valuation to arrive at fair value of the stock, which is 20 percent above the current market price. With markets staring at multiple headwinds in the near term, risk averse investors looking at a high quality business with decent and predictable earnings growth should look to buy into the stock.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!