Sachin Pal

Moneycontrol Research

Cera Sanitaryware posted decent Q1 earnings in a challenging operating environment, with healthy double-digit topline growth. Operating profit, however, came in weaker on account of a softer product mix and increased cost pressures. Business continues to show resilience in a tough operating environment as most industry players are reporting a decline in profits. The management sees demand reviving on the back of industry reforms and government policies.

Result snapshot

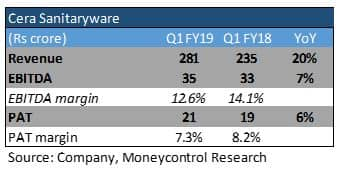

Revenue increased 20 percent year-on-year to Rs 281 crore. Earnings before interest, tax, depreciation and amortisation (EBITDA) increased by just 7 percent amid rising cost pressures. Profit after tax grew 6 percent to Rs 21 crore due to a 150 basis points contraction in operating margin.

Rising raw material prices and input costs are impacting margins across the building materials industry. Natural gas is a major constituent of the tiles manufacturing process, but forms a small constituent in sanitaryware production. Gas-related expenses constitute around 1.5 percent of Cera’s total revenue. The same increased from Rs 17.50 per cubic meter in Q1 FY18 to Rs 22.50 per cubic meter in Q1 this fiscal. The price increase impacted margin by 0.80 percent in the quarter gone by.

The usual price hikes in FY18 were skipped on account of industry and market disruptions. However, the management has taken selective price hikes of 2-5 percent in May-June to mitigate cost pressures. The full effect of these hikes will be realised from Q2 due to a lag effect.

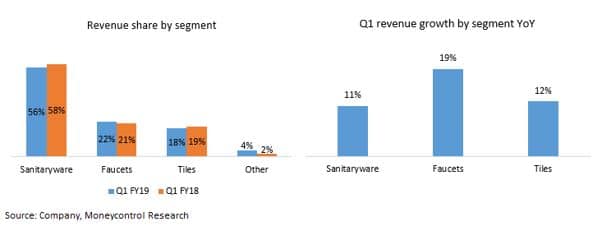

On a segmental basis, sanitaryware revenue grew around 11 percent, faucets 19 percent and tiles 12 percent. While the sanitaryware segment is operating at near optimum capacity utilisation, faucets and tiles are operating around 75 percent levels.

Cera is a leader in sanitaryware market with a share of around 23-24 percent. The same in faucets stands around 4 percent. Its share in the tiles segment is negligible as it contributes a small portion to revenue.

The management expects 15-18 percent revenue growth in FY19 led by double-digit growth in faucets and tiles. Growth in faucets will be higher due to shorter replacement cycle, while that of tiles will be driven by shift to high margin glazed vitrified tiles. Sanitaryware is expected to grow in high single-digits. It has guided at a 100-150 bps margin improvement for FY19 on account of product premiumisation and price hikes.

Outlook and recommendationBuilding material products have witnessed subdued demand due to sluggish real estate activity both on the commercial as well as residential front. FY18, in particular, turned out to be a challenging year as the sector was impacted by a number of factors including demonetisation, rollout of the Goods & Service Tax, and implementation of Real Estate Regulatory Authority (RERA). New construction activity (after the implementation of RERA) is slowly gathering momentum which will in turn propel demand for building products.

We remain optimistic on the company's long term prospects as the company has a strong brand recall, well diversified product mix and an established distribution network. Its superior operational execution among its peers is reflected in its margin, high return ratios and cash-rich balance sheet. We therefore advise long-term investors to accumulate this stock.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.