The cement industry continues to face a challenging environment in the backdrop of a sharp rise in petcoke and fuel costs, a depreciating rupee and muted pricing in a competitive market. These factors continue to undermine profitability of most industry players. However, the continued improvement in volumes across regions appears promising as it indicates that the much-awaited pricing power could return once capacity utilisation moves higher from current levels. In this backdrop, we analysed the Q2 FY19 performance of some of the large and mid-sized companies in the sector to check which ones are worthy for long term investment at this juncture.

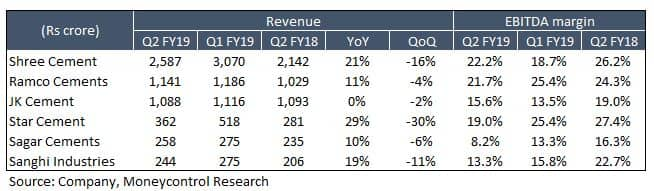

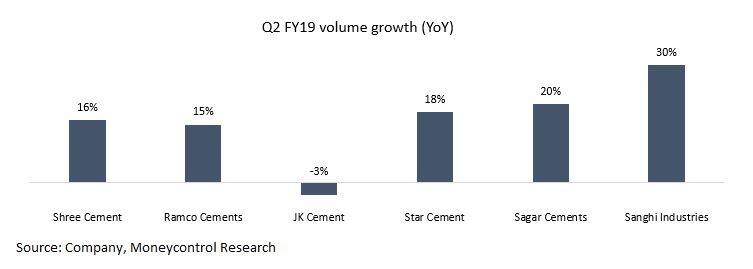

Quarterly earnings snapshot Shree Cement’s revenue increased 21 percent year-on-year (YoY) to Rs 2,587 crore as strong market demand in eastern region drove volumes higher (16 percent). Higher prices in northern markets aided improvement in realisations (2 percent YoY and 4 percent quarter-on-quarter). Surge in petcoke prices, forex losses (Rs 84 crore) along with its exposure to cash strapped IL&FS (loss of Rs 178 crore) resulted in bottomline falling into the red during Q2 FY19.

Ramco Cements’ volume growth of 15 percent was driven by healthy demand from the eastern and southern markets. This was slightly offset by low offtake from Kerala on account of heavy rains. Topline grew 11 percent as realisations remained muted. Margin came in at 21.7 percent as compared to 24.3 percent QoQ.

Ramco Cements’ volume growth of 15 percent was driven by healthy demand from the eastern and southern markets. This was slightly offset by low offtake from Kerala on account of heavy rains. Topline grew 11 percent as realisations remained muted. Margin came in at 21.7 percent as compared to 24.3 percent QoQ.

JK Cement’s revenues came in flat as the company continues to rationalise its sales mix. The 3 percent contraction in grey cement volumes was driven by change in business strategy to reduce exposure to the low margin non-trade segment. Higher contribution from trade sales aided sequential improvement in realisations and margin.

Also Read: 3 Point Analysis | Cement Sector Q2

Star Cement, the largest producer in the northeast, reported robust topline growth for the September quarter. Volume growth of 18 percent and stable realisations drove significant jump in topline. Total volumes in Q2 stood at 0.56 million tonne compared to 0.47 million tonne YoY. Raw material costs spiked up as the company had to source clinker externally due to an extended plant shutdown for maintenance. Freight expenses also increased as related subsidies (around Rs 300 per tonne) expired in January.

Hyderabad-based Sagar Cements had an operationally weak Q2 as the business was adversely impacted by plant shut down for maintenance and upgradation activities. Strong demand in its key operating markets -- Andhra Pradesh and Telangana -- drove the 20 percent increase in cement volumes. Realisations, however, dipped 9-10 percent amid high competitive intensity in the Deccan region.

Sanghi industries’ 30 percent volume growth was aided by a favourable base last year. Topline was lower owing to softer realisations (down 8 percent YoY and 4 percent QoQ). Higher slag prices and low availability kept input costs at elevated levels. Adverse shipping conditions during the monsoon season also impacted cement sales in Mumbai. Progress on capacity expansion remains on track and the management is targeting double its cement capacity by 2020.

Outlook and recommendationDemand in the cement sector continues to remain strong as most companies have reported a near double-digit volume growth in H1 FY19. Industry majors expect demand momentum to continue in H2 as well and expects a volume growth of 8-10 percent in FY19. However, the ongoing liquidity squeeze could result in some demand weakness from the infrastructure and housing segments.

Despite higher costs, cement realisation pass-through continues to be limited compared to cost inflation. Competitive intensity remains high as the industry leaders like UltraTech Cement, Ambuja Cements and Dalmia Bharat continue to operate at 70-75 percent capacity utilisation and are more focused on shoring up volumes.

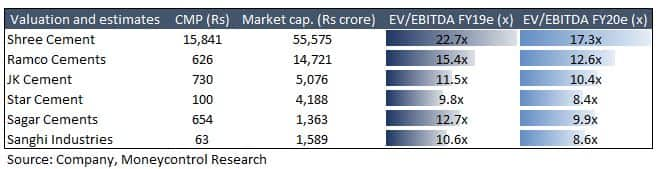

The industry is traversing through a challenging landscape and the anticipated upcycle in the sector does not seem likely in the near term. In the current environment, we prefer companies with strong market positioning and strict cost focus. Among the larger cement companies, Chennai-based Ramco Cements is best positioned to capture market growth. The company derives a large chunk of its revenue and profits from Tamil Nadu and Kerala. The flood situation in Kerala might impact volumes for the next two quarters. We advise investors to accumulate this stock on dips (FY20 estimated EV/EBITDA: 12.6 times) as this short term blip should result in a demand boost from reconstruction activity in the state.

Among the midcap cement companies, Star Cement (FY20 estimated EV/EBITDA: 8.4 times) with its unique geographical positioning is well positioned to overcome near term cost pressures. The quarterly performance was lacklustre, but the company has a strong presence in northeast and is expected to benefit significantly from industrial development in this region.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.