Neha DaveMoneycontrol Research

Aavas Financier’s initial public offering (IPO) of Rs 1,744 opens for subscription on September 25. The company plans to raise Rs 400 crore of fresh capital, in addition to an offer for sale from some of the existing shareholders amounting to Rs 1,334 crore.

The IPO comes at an opportune time with increased government focus on the affordable housing segment, the key segment that the non- banking finance company (NBFC) operates in. Affordable housing finance companies (HFCs) have been witnessing exponential loan book growth.

We see affordable HFCs as a structural growth story and a pure-play affordable housing lender like Aavas whips up our interest.

NBFC stocks, especially of HFCs, came under significant pressure since September 21 following funding concerns. We don’t see the current situation catapulting into a systemic concern. But the current scenario definitely calls for separating the wheat from the chaff.

Below are the reasons why we believe Aavas is an outlier in the overcrowded affordable housing space making it a worthy consideration.

About the company

Aavas was incorporated as a wholly owned subsidiary of AU Financier (now AU Small Finance Bank). In April 2016, AU divested a majority stake in favour of Kedaara Capital and Partner Group to fulfil the requirement for converting itself to a small finance bank.

Aavas provides small ticket housing loans in rural and semi-urban areas. The company is focused on the low cost and affordable housing segment, targeting self-employed and salaried customers in the informal segment, who otherwise have limited access to formal lending channels in the absence of proper income documents and/or limited credit history.

Aavas’s loan assets stood at Rs 4,359 crore as on June 30, 2018. While Rajasthan remained the largest contributor, at 46 percent of the loan portfolio, operations have been gradually expanded and now cover eight states.

What do we like about Aavas?

Diversified funding mix and positive ALM profile

Aavas has a diverse funding mix with bank borrowings constituting 65 percent of total funding. Though mutual funds are a source of funds, it is worth noting that the company mainly relies on long-term funding through non-convertible debentures (NCDs) and has no borrowing through commercial paper (CPs) as at end June 2018. Average tenor of outstanding borrowing is 134 months.

Securitisation and assignments is also a funding source given a significant proportion of the portfolio qualifies for priority sector lending. A chunk of its borrowings are long-term loans from banks and refinance from National Housing Bank (NHB). As on March 31, 2018, nearly 41 percent of its on-book liabilities had maturity beyond 5 years, far higher than the industry average of 23 -24 percent. Consequently, the company has a positive asset-liability gap (there are more assets than liabilities across time buckets as on June 30, 2018).

In simple terms, this means Aavas has a negligible risk of rollover of short-term debt which is a big concern faced by NBFCs in today's constrained liquidity environment.

Granularity of asset book

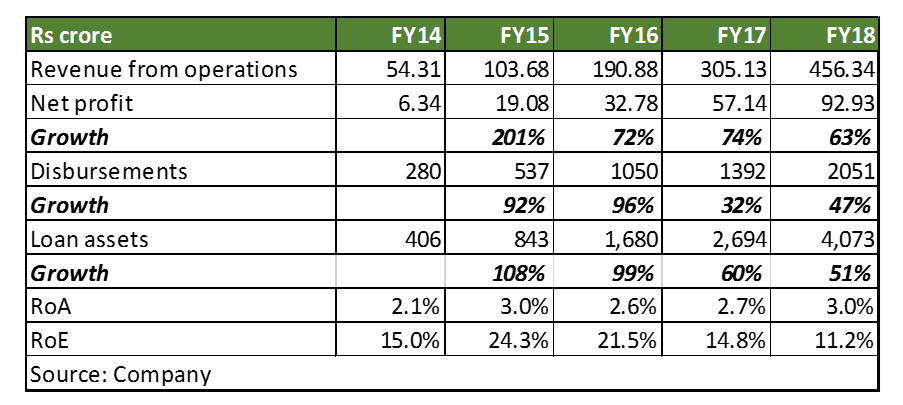

Aavas’ loan book grew at a robust compounded average growth rate (CAGR) of 78 percent over FY14-18 to Rs 4,070 crore. The encouraging part is that this growth has been volume driven and less reliant on expansion of average ticket size. Aavas’ average ticket size is around Rs 8.5 lakh and management intends to maintain it around the similar level (Rs 8-10 lakh).

Another comforting part about Aavas’ loan portfolio is it has zero exposure to developer finance, under construction properties or land financing. Further, the company avoids lending to customers directly linked to agriculture and dairy activities as their cash flows are highly volatile.

Such superior credit underwriting policies have helped Aavas build a relatively low-risk loan book.

Strong asset quality

Aavas enjoys good asset quality with gross NPA of 0.5 percent as at the end of June due to stringent underwriting norms, strong collection infrastructure and detailed analytics. However, its portfolio vulnerability remains high given 64 percent of loans are to self-employed customers as cash flows of borrowers in these segments are highly volatile.

Despite this, we expect low credit losses given the secured nature of lending with a moderate loan-to-value ratio at origination (around 50 percent), most of the properties being self-occupied and the fact the company is covered under the Securitisation and Reconstruction of Financial Assets and Enforcement of Securities Interest (SARFAESI) Act.

Profitable growth

Despite the high growth, Aavas has been able to maintain superior profitability with a return on average assets of 3.0 percent in FY18 supported by good net interest margins and low credit costs.

Aavas’ target customers being self-employed individuals help in keeping the yields higher than peers and result in elevated net interest margins (NIMs).

The operating expenses are slightly on a higher side with the cost-to-assets ratio at around 4 percent. This can be attributed to an end-to-end in-house model of operations covering sourcing to collection activities as it does not employ any direct selling agents (DSAs). But we can expect operating efficiency kicking in with growth in the loan book.

Going ahead, rising cost of funds is likely to depress net interest margins (NIMs) which should be partially offset by an improvement in operating efficiency and increased scale of operations. Hence overall, we don’t see much downside to earnings.

Aavas has more than adequate capital which will increase further with the current issue of Rs 400 crore. Due to excess capital, return on equity (RoE) is depressed to 11.2 percent. We expect leverage to improve in the medium to long term thereby increasing RoE.

Well-placed in high growth focused segment

We expect affordable housing segment to continue to grow at a high rate backed by the several government initiatives (interest subvention scheme, tax incentives, Housing for All by 2022, infrastructure status accorded to affordable housing, PMAY) along with regulatory push (priority sector status, lower risk weights on small ticket size loans).

Affordable housing financing business requires a deep feet-on-street and a considerably evolved risk assessment process, stringent underwriting norms, agile monitoring and superior collection mechanisms. With the usage of technology and analytics, Aavas has succeeded in creating all of these and building a superior franchise with significant competitive advantage.

Valuation undemanding considering high earnings growth potential

At the upper end of the price band i.e at Rs 821 per share, Aavas is valued at 4.05 times trailing book on post money basis and 3.4 times FY20e book value. For an HFC with strong earnings growth potential and ability to generate return on assets (RoA) between 2.5 - 3 percent, the valuation seems quite reasonable.

On a relative basis also, valuations look undemanding when compared to well-established financial lenders operating in retail lending space (Gruh Finance, Bandhan Bank). In the near term, we expect strong earnings growth to drive the stock price. In the medium to long term, we expect valuation multiple to expand with scaling up of the franchise.

Given the high growth potential, experienced management along with a well-capitalised balance sheet, Aavas is well poised for the next leg of growth. It is a good long-term bet available at a reasonable price. We recommend investors to subscribe to the IPO.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!