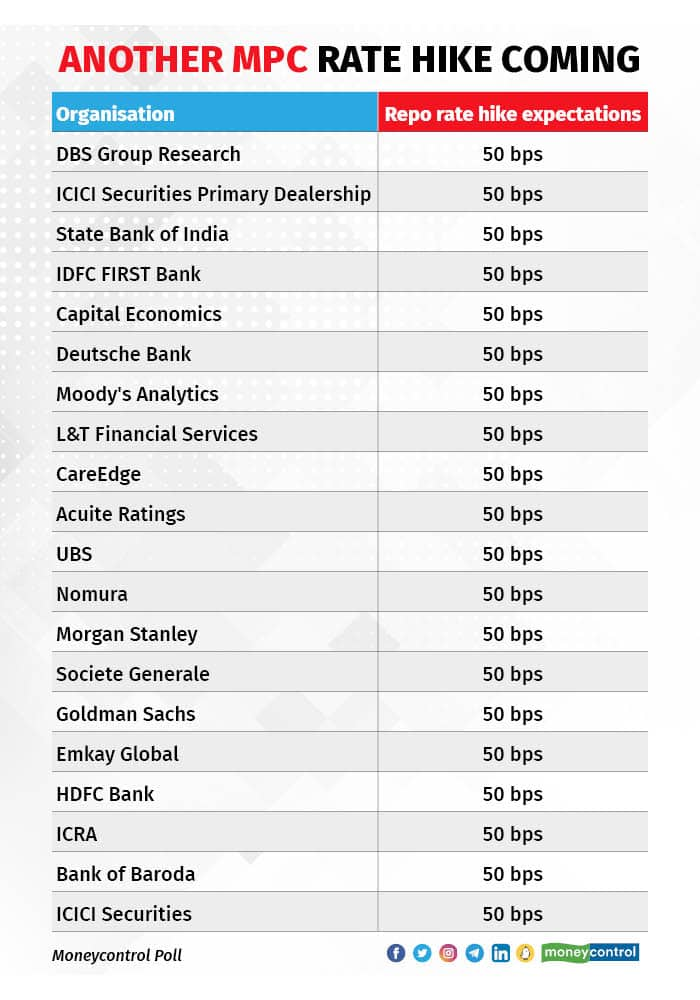

The Reserve Bank of India’s rate-setting panel is likely to increase the key policy rate by 50 basis points (bps) at its meeting this week as inflation continues to be the dominant theme in deliberations, shows a Moneycontrol poll of 20 economists.

The Monetary Policy Committee (MPC) begins its three-day meeting on September 28 and will announce the outcome on September 30.

If it happens, a 50 bps increase in the repo rate this week would be the fourth consecutive one since May. That would take the repo rate, at which the RBI lends short-term funds to banks, to 5.90 percent – the highest level since April 2019 – from 5.40 percent currently.

The MPC has increased the policy repo rate by 140 basis points since May to quell inflationary pressure. One bps equals one-hundredth of a percentage point.

The central bank is striving to keep a lid on soaring prices. India’s headline retail inflation rate, as measured by the Consumer Price Index, returned to the 7 percent territory in August from 6.71 percent in July.

In the backdrop of high inflation, all 20 economists polled by Moneycontrol estimated a rate increase of 50 bps.

“With the MPC more confident about growth than inflation, the central bank’s hawkish policy bias will continue this week,” said Radhika Rao, executive director and senior economist at DBS Group Research. “We revise our rate hike call for the upcoming meeting to 50 bps from 35 bps previously, taking the repo to 5.9 percent.”

Economists were, however, divided on whether the MPC will continue with the stance of withdrawal of accommodation or change it to ‘neutral’ amid the prevalent liquidity conditions in the banking system. Liquidity has tightened significantly in the past few sessions, causing the interbank call rate to jump above the repo rate.

Considering that liquidity did slip into a deficit for some time, the RBI may announce measures, including open market operations, for liquidity management, said Sonal Badhan, an economist at Bank of Baroda.

Also read: RBI may hold more repo auctions to ease liquidity, say bankers ahead of policy meetSticky inflationEconomists polled by Moneycontrol said there are two major reasons for the MPC to go in for aggressive rate hikes. Inflation, they said, has remained stubbornly above the 6 percent mark, warranting aggressive rate action. The RBI would want to bring back inflation within its tolerance band at the earliest, which could justify rate hikes at this stage.

Retail inflation has stayed above the medium-term target of 4 percent for 35 consecutive months and outside the RBI’s 2-6 percent tolerance range for eight straight months. The RBI is deemed to have failed its mandate when average inflation is outside the 2-6 percent tolerance range for three consecutive quarters. As such, the RBI is now on the brink of failing to meet its inflation mandate.

Barclays’ chief India economist Rahul Bajoria said that falling commodity prices might offer some relief, but tighter global financial conditions and high inflation will lead the MPC to stick to its frontloaded tightening cycle.

While there are early signs of stabilising growth momentum, above-target inflation and an evolving external backdrop leave little scope for the RBI to pause its policy-tightening cycle, Bajoria added.

Santanu Sengupta, India economist at Goldman Sachs, said lower production of wheat and rice due to weather-related shocks is likely to drive cereal inflation higher. The brokerage has revised its October-December food inflation forecast higher to 6.8 percent from 5.5 percent earlier. Headline inflation, Sengupta added, could also be above the RBI's inflation forecast in October-December.

Aggressive FedThe other key reason for the MPC to consider a 50 bps rate hike would be the aggressive policy-tightening path by the US Federal Reserve. The Fed raised interest rates by 75 bps to 3-3.25 percent on September 21 and signalled cumulative rate hikes worth 125 bps in 2022 alone amid persistently high inflation.

Tighter policy rates and fears of a recession have led to a stronger dollar as investors shun risky assets for safe-haven investments.

“Despite raising the policy rate by 75 bps, the Fed’s rather hawkish forward guidance has led to an increased yield for the Government of India bond and sharp depreciation of the rupee,” said Kunal Kundu, India economist at Societe Generale. “While the quantum of the Fed rate hike was generally expected, the central bank’s expectation of a higher terminal rate and weaker growth has roiled the market – it seems to be perceiving this grim outlook as the central bank attempting to engineer a recession to combat inflation.”

If so, this puts the RBI in an “uncomfortable” position, given the continuing price pressures, added Kundu.

IDFC FIRST Bank’s India economist Gaura Sen Gupta concurred with Kundu’s view.

“Looking ahead, while inflation determines the policy rate trajectory, the ability of a central bank to persist with tightening will depend on growth,” said Sen Gupta. “The latter is where we expect RBI policy response to diverge from the Fed.”

In addition to September’s rate hike, economists expect the MPC to continue with more rate hikes in upcoming policies, anticipating sticky price pressures. However, while the MPC is expected to frontload rate hikes, it is unlikely to match the Fed in terms of policy-tightening, according to economists polled. They expect the repo rate to be at 6-6.50 percent by March.

Also read: Fed delivers third-straight big hike, sees more increases aheadFactored inAccording to money market participants, the bond market and the forex market have priced in a 50 bps rate hike by the MPC this week.

The bond market, experts said, could take cues from RBI governor Shaktikanta Das’ comments and the tone of comments of other MPC members, apart from the expected rate hike. In the last policy in August, Das had said that a 50 bps-rate hike had become the "new normal," for central banks.

Additionally, the news flow regarding inclusion of local bonds in global indices, the debt supply calendar for the second half of the fiscal year, and movement in oil prices and US Treasury yields will be key watch points, they added.

“The bond market is still divided on where the terminal repo rate will be by March. Initially, expectations were between 5.75 -6.00 percent and now it is expected that the terminal repo rate can reach as high as 6.50 percent, if not more, before this fiscal,” said Venkatakrishnan Srinivasan, founder of Rockfort Fincap, a Mumbai-based debt advisory firm.

Hence, the market can only decide the future course of action after the RBI governor’s post-policy speech about our economy and inflation trajectory, added Srinivasan.

As far as the forex market is concerned, the rupee rate will be determined by global factors like dollar strength, Fed actions and foreign inflows, said currency experts. The rupee has been on a weakening spree of late against the dollar and had dropped to another record low of 81.95 on September 28, as per Bloomberg data. The RBI typically intervenes in the forex market to prevent exchange rate volatility.

“The dollar index might stay buoyed, aided by surging US Treasury yields, hawkish comments from Fed officials and safe-haven buying amid a looming recession,” said Jigar Trivedi, senior analyst – currency and research at Reliance Securities. “The MPC will deliver at least a 50 bps rate hike this week given the recent fall in the rupee.”

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.