The Indian market had a bumpy ride during the decade 2009-19 as a host of global and domestic factors put the market on shaky ground.

BSE Sensex rose 136 percent while Nifty saw a gain of 134 percent in the last ten years. BSE Midcap and Smallcap indices have seen a rise of 123 percent and 136 percent, respectively, in the same period.

Data shows that over the calendar years 2009-2019, the Indian market delivered the second-best growth rate in returns after the US in the pecking order of world markets.

However, in dollar terms, Japan and Taiwan markets’ performance was better than India’s, given the underlying rupee depreciation against the US dollar.

As per Motilal Oswal Financial Services, over CY09-19, Nifty delivered an 8.9 percent return CAGR, mirroring the Nifty earnings per share (EPS) CAGR of 8.2 percent over that period.

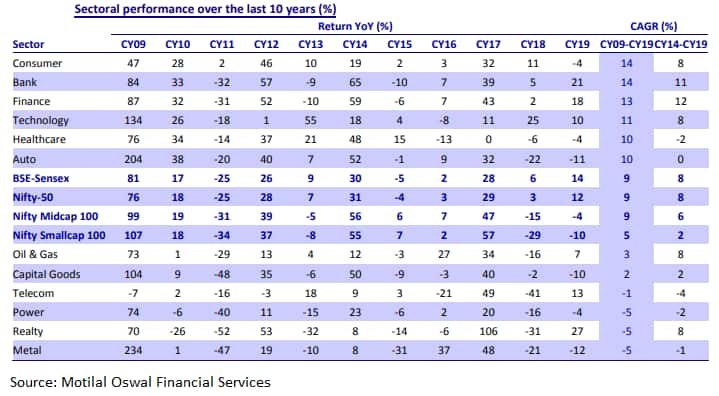

Even these tepid returns were driven by a few select sectors like BFSI, consumer, IT, pharma and automobiles, while the rest of the sectors belonging to the investment side of the economy (capital goods, cement, real estate, power) and commodities (metals, oil & gas) underperformed massively.

This has created a significant divergence in the valuations of these sectors which exacerbated in the last three years.

At this juncture, it seems pertinent to ponder if the trend will continue in the current decade as well.

Most experts and analysts are positive on the Indian market for the long term and are of the view that the consumer sector will extend its growth story in the current decade.

Let's take a look at how some of the experts expect the new decade to be for the Indian market.

Expert: Paras Bothra, President of Equity Research, Ashika Group"The growth story of the last decade could be summed up as the story of consumption. In fact, the consumption story in India is core to economic growth and likely to continue driven by demographic changes and rising middle-class population. So, consumer discretionary, consumer durables, auto and financial space will continue to grow at attractive rates for the next decade too," said Paras Bothra, President of Equity Research at Ashika Group.

Within the consumption sector, however, there would be disruption driven by digital initiatives and artificial intelligence. Besides, climate change will also play its part in bringing in new farming techniques and water infrastructure, said Bothra.

Demand for clean energy, electric vehicles will lead to disruption in the auto sector. An aging worldwide population over the next decade will throw a plethora of opportunities for healthcare companies. Also for a growing country like India long-term potential of the sectors should be looked at in the context of per-capita consumption which remains quite low in comparison to developed countries, hence a long way to go.

Moreover, for banks, growth is tied to the growth in the economy and the quantum of incremental GDP growth, both of which require massive funding in the next decade. Banks and financial institutions would be in a sweet spot to fund the growth of India Inc.

For metal, while the demand drivers certainly don’t look robust at this point in time, the sector is unlikely to repeat the past decade’s performance.

The real estate sector has battled various challenges in the last decade (high inventory, low demand and heavy leverage) and with the formalization of the sector (RERA), organized players will continue to grow on the back of demand for affordable housing projects.

The telecom sector has probably seen its lows and the year 2020 has already marked at a revival for the players with revision in the tariff structure.

The demand for power sector has better drivers in the next decade than the previous one driven by an increase in penetration of consumer durables, demand for clean energy and electric vehicles.

Moreover, for capex heavy business, value creation depends on the return on equity higher than the cost of capital for a sustainable period of time and for the sectors mentioned above, leaving apart certain well managed, low-cost producers, scale, etc., majority of the companies falls short of these criteria and hence underperformance.

The best way is to participate in the upswing with respect to changing business dynamics and wild operating profit swings because of leverage and attempting to capitalize at the peak of the cycle.

To put things in perspective is the mean return from Indian equities as an asset class for long-term has been in the range of 12 percent to 16 percent and the outperformance can be construed as a couple of basis points above the averages.

Expert: Narendra Solanki, Head of Fundamental Research (Investment Services) - AVP Equity Research, Anand Rathi Shares & Stock BrokersWhat we should keep in mind is that markets operate in cycles, and also keep in mind what were the precursor events few years prior to any start of a decade which helps you in adjusting your expectations for future returns.

As far as the next decade is concerned, firstly, we think growth would definitely be there and the Indian economy is poised to grow at least around 7 percent CAGR and with long-term inflation of 4 percent its nominal growth could be around 10 percent-13 percent range.

Secondly, our view is that the Indian economy is currently under transformation and one can already see some disruption led by technology under process. Now, our current listed space is not able to capture this new space as there are very few companies listed right now.

Keeping these two points in mind we think it is justified as of now to start with a lower adjusted CAGR number which could be more realistic and have room for upwards revision down the line.

Coming to the sectors, consumer, financials, technology and healthcare should continue to do better, including autos.

Even we look forward to one theme which is fast emerging in various sectors which are mired by lack of transparency due to the nature of business and higher cash transactions.

We believe the current wave of disruptions on the consumer payments side should also add to earnings by way of higher transparency and compliance in sectors like road toll Infra, Healthcare, Power distribution, Realty, etc. to name a few.

Metals, real estate, power and telecom are the sectors that are highly exposed to policymaking, global macro, political risks, etc. So, these continue to remain volatile and in between, you could see good returns.

From the long-term perspective, we definitely are going to see them grow in terms of volumes and expansion but in valuation terms too much depends on macro market structure and stability. So, investors could have them at lower allocations if at all and then gradually build up as things improve.

A CAGR of anything around 12-15 percent should be decent for the coming decade from above-discussed sectors keeping in mind that we start off with already low inflation and moderate base in terms of valuations and few even at somewhat higher base and also if you see long term G-Sec rates and compare it than even at these rates one outperforms by handsome margins.

Expert: Naveen Kulkarni, Head of Research, Reliance SecuritiesThe consumer sector will continue to perform in the next decade also but more likely at a slower pace than the previous decade.

Banks should deliver similar performance as the previous decade. Technology and Healthcare are more likely to be mixed bags with certain stocks outperforming the market and some laggards.

Autos could still outperform the market considering the under penetration in the sector.

Metals are cyclical and predicting the performance for an entire decade poses a challenge. However, Real estate and Telecom are likely to deliver good returns in the next considering the peak of the industry challenges are behind and the market has seen immense consolidation.

The power sector has many challenges and there is tremendous value but more often than not the sector has proven to be a value trap. We believe the sector will continue to reel under pressure and may not perform up to the expectations.

We estimate the broader market to deliver nearly 11 percent return for the next decade.

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not that of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.