Amit Gupta

The Nifty staged a strong recovery in the May expiry week on the back of closure of short positions particularly backed by the banking heavyweights.

The ongoing trend of selective participation by few heavyweights continued while market breadth remained negative in four of the last five sessions.

The volatility has so far remained subdued in the recent period despite intermediate declines seen in the previous weeks which indicates towards increasing buying interest at lower levels that can lead to more consolidation in the June series.

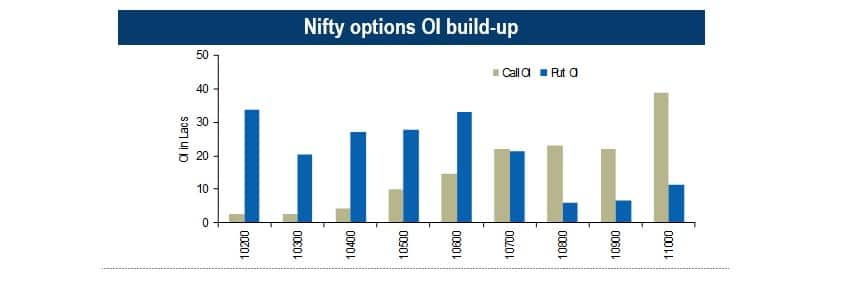

Looking at the option concentration for the June series, the major Put base is placed at 10,200 strike due to Leap options.

However, 10,600 strikes saw highest incremental option addition in the last 15 sessions along with 10,500 Put strike indicating limited downsides from current levels.

At the same time, no immediate major Call option base has still been formed till now. The highest Call base is still placed at 11000 strikes.

The Nifty futures open interest at inception was marginally lower compared to the last series amid continued subdued roll spread. At the same time, Bank Nifty open interest stayed on the higher side.

Current open interest in the Bank Nifty is the highest seen at the time of inception in the last one year. Fresh highs in the banking index can be seen if Bank Nifty is able to sustain above 27,000.

Among stocks, cement and technology saw relatively low rollover while FMCG and banking saw high rollover of positions indicating the ongoing positive bias in these stocks will continue.

Bank Nifty: Short covering trend may magnify

The index ended the May series on an optimistic note with aggressive short covering seen on the May series F&O expiry day where the index witnessed a sharp up move and closed well above 27,000 levels.

Private sector banks were the leaders where Kotak Mahindra Bank and HDFC Bank rose nearly 4 percent each along with the participation from the PSU pack.

The Bank Nifty started the June series with the highest number of shares in open interest compared to the past few months whereas the discount in the index has widened indicating rollover of short positions.

Unless we see the aggressive closure of these short positions, the upside in the index is likely to continue as short traders will look to exit in the fall.

As the index moved above 26,500, Call writers shifted their positions to 27,000 and 27,200 strikes whereas Put positions have also shifted higher to 26,500 and 26,600 strikes indicating major supports.

Volatility is likely to be higher, ahead of the RBI’s monetary policy that is lined up next week. In the absence of any negativity, the index is well placed to move towards 27,200.

The current price ratio of Bank Nifty/Nifty has moved to 2.49 from 2.45 levels. We feel the current leg of outperformance is likely to continue on the back of the short covering trend in private sector banks.

EM equities continue to trade near support zone

The weakness continued in emerging market (EM) equities as select EM currencies like Mexican Peso, Brazilian Real, Argentine Peso & South African rand continued to trade weak (propelled by sticky dollar index reading of 94).

The risk environment continued to remain fluid as the decline in EM equity and bond continued. The MSCI EM Index fell over 1.5 percent during the week but this weakness was also seen in MSCI World Index, which also declined by a similar magnitude.

Italy’s fractured mandate that gave anti-EU parties a chance to form the government was the key reason for the decline. US trade spat with China, Europe and Nafta further elevated the worries.

Till now, FII outflows have continued from most EMs. Outflows were seen from Taiwan ($592 million) Thailand ($472 million), Malaysia ($262 million), & Brazil ($210 million) while Korea was the outlier seeing inflows of over $381 million.

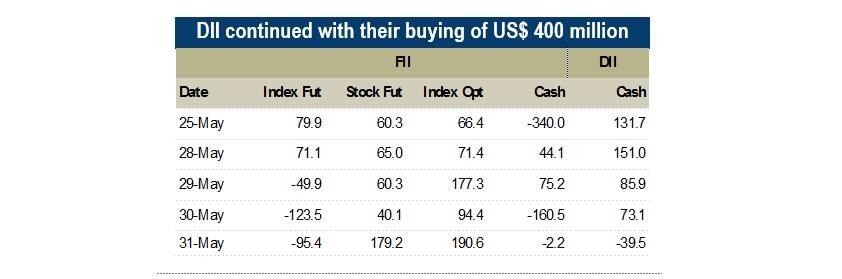

In the Indian markets, FIIs’ bearish bias continued. During the week, they created fresh shorts totalling over $117 million in index futures segment.

In the cash segment also, FIIs sold over $383 million. However, DII inflows of over $400 million ensured declines in the Nifty were limited.

Cool-off in rates, not only contained the dollar surge but also helped equities to consolidate without much of a decline. Italy’s political stand out, US trade tensions and the upcoming data from the US including the non-farm payroll (due today) will set the course for the risk assets.

Key variables that could support fresh FII allocation into EMs will include (a) stability in EM forex space (b) Dollar Index starts declining (c) US 10-year yields staying below 3 percent and (d) MSCI EM Index reverting from the current support zone.

Disclaimer: The author is Head of Derivative from ICICIdirect. The views and investment tips expressed by investment expert on moneycontrol.com are his own and not that of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.