The strong momentum built up in the market in July, due to in line-to-better-than-expected June quarter earnings, continued in August as well. The Sensex and Nifty rallied more than 9 percent each to scale new highs of 38,989.65 and 11,760.20, respectively, in the current week. The BSE Midcap and Smallcap indices jumped over 8 percent and 6 percent in two months, respectively.

Apart from earnings, improved foreign institutional inflow, consistent support from domestic institutional investors and easing global trade tensions lifted market sentiment. Experts believe the momentum is likely to continue for the next few months.

"We remain constructive on Indian equities going forward. We essentially derive our confidence from the pick-up in industrial activity and robust consumer demand aided by strong rural growth, which has now begun to reflect in Q1 FY19 earnings," said Pankaj Pandey, Head of Research at ICICIdirect.com.

Sampath Reddy, Chief Investment Officer, Bajaj Allianz Life Insurance, feels earnings growth (and not P/E expansion) will drive the market rally going forward. "We see earnings growth of over 15 percent CAGR in FY19 and FY20. If this pans out as expected, we may even see a compression in market P/E multiple, which seems relatively elevated at current levels."

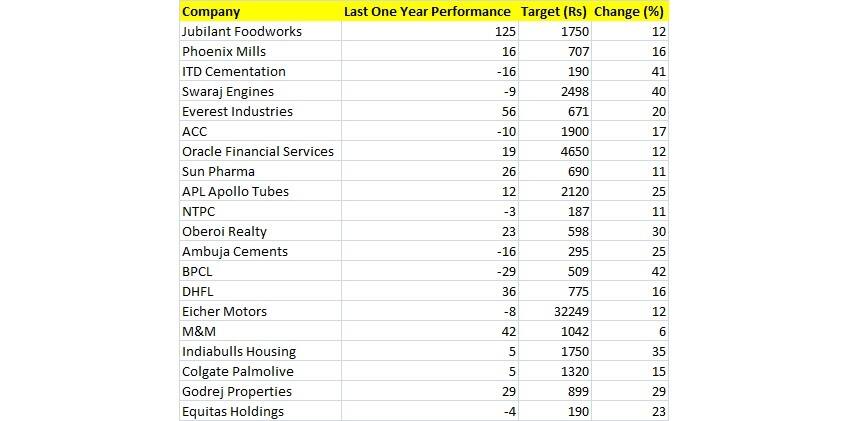

Here is a list of 20 stocks upgraded by brokerages in August. These stocks could return up to 40 percent in the next one year:

Brokerage: UBS

Jubilant Foodworks: Buy | Target: Rs 1,750 | Return: 12%

Global brokerage firm UBS has upgraded the stock rating to Neutral from Sell and also raised target price to Rs 1,750 from Rs 950, implying potential upside of 13 percent.

Revenue and same-store-sales growth momentum can be maintained by the company and Jubilant is unlikely to lose the battle against its competitors in the long run.

We see limited upside till return on invested capital (RoIC) improvements begin to show.

Brokerage: Kotak Securities

Phoenix Mills: Buy | Target: Rs 707 | Return: 16%

Revenue growth going forward is likely to be led by rental renewals and improvement in commercial and hospitality revenues. We maintain estimates and expect revenues to grow at a CAGR of 7.4 percent between FY18-20.

Operating margins improved during the quarter on YoY basis but were impacted by fit outs going on at HSP which led to lower CAM charges. Going forward, we expect operating margins of 48.7/49.5 percent for FY19/20 respectively.

We maintain estimates and expect net profits to grow at a CAGR of 14.5 percent between FY18-20.

We continue to remain positive on the company and maintain price target of Rs 707 based on sum of the parts valuation on FY20 estimates. Owing to adequate upside from current levels, we upgrade the stock to Buy from Accumulate earlier.

Brokerage: Anand Rathi

ITD Cementation: Buy | Target: Rs 190 | Return: 41%

Strong, 25 percent, Q1 FY19 revenue growth was a sign of the shape of things to come for ITD Cementation. Q2FY19 is even better with even stronger revenue growth, implying execution is gathering pace with each passing quarter.

The quarter could have been better on order additions, but a healthy L1 status and a buoyant opportunity landscape suggest better days ahead.

With its strong order backlog (and good progress in new orders), a buoyant opportunity landscape and a healthy balance sheet, the future looks bright. The fall in the stock price (around 17 percent in three months, around 29 percent in six) renders it attractive. Thus, we upgrade it to a Buy.

We value it at a PE of 16x FY20 to arrive at a target price of Rs 190. Risk would be any slower-than-expected execution.

Swaraj Engines: Buy | Target: Rs 2,498 | Return: 40%

We expect that triggers for tractor growth and expected strong growth in FY19 would throw up prospects for Swaraj Engines to post strong earnings growth. Due to the recent drop in the stock price we upgrade rating to a Buy.

Against the backdrop of the 11 percent, CAGR in volumes over FY18-20 to 1,14,106, units, we expect revenue to grow 10 percent to Rs 930 crore and lead to an 11 percent CAGR in EBITDA. With the company’s lean cost structure and strong balance sheet, we value the stock at 30x FY20e EPS of `83.3 and arrive at a target price of Rs 2,498.

Risk would be constrained volume growth in M&M tractors would cut into volume and earnings growth.

Everest Industries: Buy | Target: Rs 671 | Return: 20%

The sound performance of its BP division and its de-leveraging led Everest to report its highest-ever quarterly PAT. Its Steel Building division’s roller-coaster performance, though, will continue to be a matter of concern.

We believe that Everest will benefit from rising demand because of its widest range of roofing products, its continuous focus on launching variants with value-added features and its greater operating efficiency. We upgrade rating to a Buy, with a target price of Rs 671.

Risks would be rise in input costs, currency fluctuations.

Brokerage: Dolat Capital

Oracle Financial Services: Accumulate | Target: Rs 4,650 | Return: 12%

Despite the decline in new license revenue, OFSS has seen healthy deal signings in the new license sales in Q1FY19; bookings have grown 40 percent YoY to USD 28 million as on Q1FY19 led by the new OBP deal win. The management indicated of one more large OBP deal in the pipeline and expects license revenue to cross $ 100 million for full year FY19 (over 13 percent YoY growth in bookings) we have estimated license revenue growth of 14 percent YoY in FY19.

We upgrade earnings estimates by 9 percent for FY20/FY21. We upgrade OFSS to an Accumulate (Reduce earlier) rating and rollover to a Sep’19 target price of Rs 4,650 (Rs 4,250 earlier) based on 21.5x one-year forward PER.

Brokerage: ICICI Securities

Sun Pharma: Buy | Target: Rs 690 | Return: 11%

Q1 numbers were upbeat on the earnings front while momentum in speciality pipeline ramp-up also looks promising. Going ahead, the management expects near term margins to get impacted due to frontloading of cost of specialty launches. This optical move is the culmination of the management’s long going endeavour for a drift from generics to specialty in the backdrop of US headwinds. This, we believe, is the key differentiator vis-à-vis peers.

The management has reiterated double digit growth guidance for FY19 with slew of specialty launches in the US besides Halol decongestion. We upgrade the stock to Buy as we believe the management is hitting the right chord with sustained planning and investments in the specialty portfolio. Target price is Rs 690 based on 26x FY20E EPS of Rs 25.1 and Rs 38 NPV for Tildrakizumab.

Godrej Properties: Buy | Target: Rs 899 | Return: 29%

We have upgraded the stock to Buy from Add and maintained target price at Rs 899 per shares after Q1 earnings.

Bandra-Kurla Complex commercial project contributed majority of revenue in Q1FY19 and sales volumes were driven by new launches.

Earnings were muted on implementation of IndAS 115 accounting standard.

Equitas Holdings: Buy | Target: Rs 190 | Return: 23%

We have upgraded the stock to Buy from Add with increased target price at Rs 190 from Rs 180 per share.

Earnings upgrades are driven by asset growth. We have changed FY18-20 loan growth CAGR from 25.1 percent to 35.8 percent and upgraded earnings estimates by 3-12 percent for FY19-20.

Brokerage: IIFL Private Wealth

APL Apollo Tubes: Buy | Target: Rs 2,120 | Return: 25%

APL Apollo reported strong set of numbers during Q1 FY19 driven by robust pickup in volumes. The company registered 45 percent topline growth in Q1 FY19 backed by around 14 percent YoY growth in overall volume and around 28 percent YoY increase in realisation across product portfolio.

Going forward, volume growth is likely to remain strong driven by higher underlying product demand and benefits arising from ramp-up of new capacities that would cater to new end-use segments. The rise in share of high margin products would translate into robust earnings growth. We upgrade rating to Buy with the target price of Rs 2,120.

NTPC: Buy | Target: Rs 187 | Return: 11%

NTPC reported Q1 FY19 performance largely inline with estimates with the standalone topline growing around 14 percent YoY. The growth was primarily aided by 8 percent growth in power generation and sharp jump in tariff (improved from an average of Rs 3.23 in FY18 to Rs 3.36 in Q1 FY19).

Going forward, the management has guided for the limited impact of coal shortages in the rest of FY19. NTPC’s total group capacity at the end of Q1 FY19 has reached to around 54GW and the company is targeting to add 5GW capacity each in FY19E and FY20E. With these additions, the overall capacity is poised to reach around 64GW by FY20E.

Going forward, new capacities coming on-stream and PLF improvement would be the key drivers of revenues and earnings for the Company. With recent correction in stock price, we upgrade rating to Buy with target price of Rs 187.

Brokerage: HDFC Securities

Oberoi Realty: Buy | Target: Rs 598 | Return: 30%

After a muted Q4FY18, ORL had an impressive start to FY19 clocking in 0.3 million sqft in pre-sales and Rs 620 crore in sales value. Revenue came in at Rs 890 crore in Q1FY19 (lower by Rs 1,130 crore due to IND AS 115). Since ORL's contracts don't have a termination clause, ORL can continue to follow percentage completion method for revenue recognition.

ORL will continue to assess internal thresholds for booking margins. While the Borivali project has met margin recognition in Q1FY19, for Mulund the entire pending margins will be recognised only later in FY19E. ORL’s recent QIP proceed of Rs 1,200 crore will be used as growth capital towards fresh land purchases (not too eager to indulge in JDAs).

With recent price correction we upgrade ORL to Buy from Neutral with Rs 598 per share target price.

Brokerage: Nomura

ACC: Buy | Target: Rs 1,900 | Return: 17%

We have upgraded the stock to Buy from Neutral and raised target price to Rs 1,900 from Rs 1,890 earlier.

After correction, valuations are no longer demanding. Cycle uptrend has begun and earnings recovery is on track.

Volume upside in ACC is limited, but it may surprise on realisations/costs.

Ambuja Cements: Buy | Target: Rs 295 | Return: 25%

We have upgraded the stock to Buy from Neutral earlier but slashed target price to Rs 295 from Rs 300 as post-correction valuations are attractive.

As demand growth continues, earnings outlook looks better. New capacity improved its volume outlook. We see synergy benefits to improve after master supply agreement.

DHFL: Buy | Target: Rs 775 | Return: 16%

Return on equity (ROE) improvement should drive re-rating for DHFL. We expect ROEs to improve to 15-16 percent despite dilution built in FY19F.

We have upgraded DHFL to Buy with target price of Rs 775 per share.

Indiabulls Housing: Buy | Target: Rs 1,750 | Return: 35%

We have upgraded the stock to Buy from Neutral and raised target price to Rs 1,750 from Rs 1,500 per share earlier. We also raised profit estimates by 3-7 percent.

We factored in lower provisioning & better growth under IndAS. We expect RoE of 27-29 percent on increased net worth.

Brokerage: Elara Capital

BPCL: Buy | Target: Rs 509 | Return: 42%

We upgrade BPCL to Buy from Reduce, as we believe the oil marketing companies (OMCs) would be able to pass on impact of higher crude prices on retail diesel/gasoline sales indicated from recent recovery in margins despite elevated crude prices presently at around $75 per barrel. We revised target price to Rs 509 from Rs 496, as we expect higher retail margins from Rs 2 per litre to Rs 2.2 per litre.

We increased FY19E EPS by 15 percent and FY20E EPS by 20 percent on higher retail margins.

Brokerage: Axis Capital

Eicher Motors: Buy | Target: Rs 32,249 | Return: 12%

Company's Q1 results are in-line with Royal Enfield's Margin at 32.3 percent & VECV's at 9.2 percent. Royal Enfield continued to post same-store-sales growth of 10 percent.

Competition is still couple of years away. Even after volume growth moderated, company is still a 25 percent earnings CAGR story.

We have upgraded the stock to Buy with a target price at Rs 32,249 per share.

M&M: Buy | Target: Rs 1,042 | Return: 6%

We have upgraded the stock to Buy from Hold and raised target price to Rs 1,042 from Rs 950 per share as Q1 earnings beat estimates by 5 percent driven by a strong margin.

Company is relatively most impacted among OEMs going into BS VI emission norms. Tractors are expected to hit a downcycle possibly in FY21.

Till FY20, company can continue the strong ride. We have raised FY19/20 earnings estimates to 13/15 percent.

Brokerage: Credit Suisse

Colgate Palmolive: Outperform | Target: 1,320 | Return: 15%

We have upgraded the stock to Outperform from Neutral with increased target price at Rs 1,320 from Rs 1,150 per share earlier.

Market share loss is likely to stem as Patanjali's impact reduced. We expect company's market share to stop dropping in the next two quarters.

Margin will be lower in FY19 but will recover in FY20. We have increased FY20/21 earnings estimate by 1-4 percent.

Disclaimer: The views and investment tips expressed by brokerage houses on Moneycontrol are their own, and not that of the website or its management. Moneycontrol advises users to check with certified experts before taking any investment decisions.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.