The market, after seeing the March nightmare (down 23 percent) due to COVID-19 crisis, managed to recover a bit in April following up move in global peers, and stimulus measures taken by central banks to support economies.

In April so far, indices have gained 9 percent each, and if we include gains of last week of March, then the recovery is at 25 percent since the lockdown.

The rally is on the hopes of another round of stimulus package from the government, sharp fall in oil prices, and partial opening up of the economy in developed nations.

The upside is capped though as the number of cases of COVID-19 is still on the rise globally and domestically, experts feel.

"Given the sharp correction of over 30 percent in the last 2 months, markets have more than discounted the March quarter results. The focus on the market is now on recovery of the economy from a virtually zero base of April 2020 as lockdown opens in the next few weeks," Sailesh Raj Bhan, Deputy CIO – Equity Investments, Nippon India Mutual Fund told Moneycontrol.

"As normalcy returns close to festival season, the economic activity can see significant come back in H2 of FY21. With interest rates, oil prices, inflation remaining muted and likelihood of a good monsoon, FY22 can be a materially positive year, possibly matching or exceeding FY20 and well ahead of FY21," he said.

The majority of experts started advising clients to accumulate quality stocks in a gradual manner with a long term view, while as the valuations suppressed, brokerages also initiated coverage on some good stocks with potential double-digit returns.

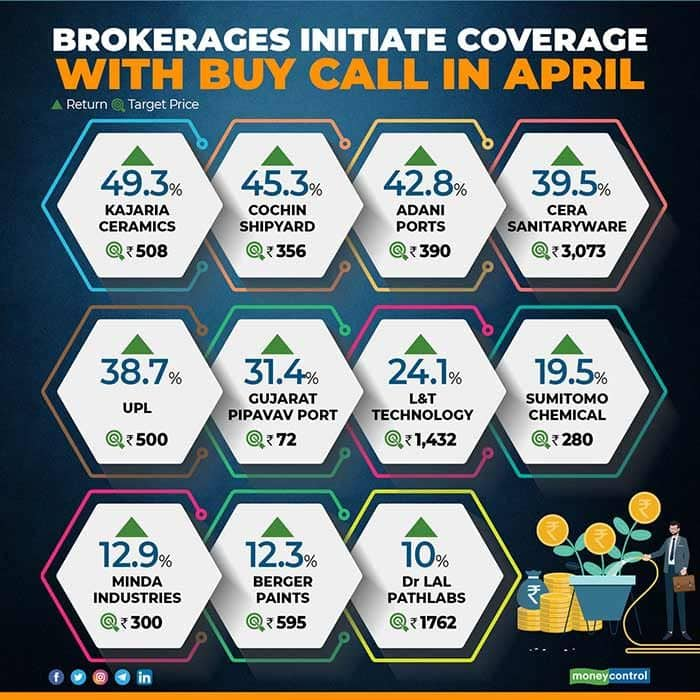

Here are 11 stocks where brokerages initiated coverage with a buy call and see 10-49 percent upside:

"We expect the animal nutrition business along with CRAMS opportunity to change the business mix in the medium to long term. In turn, this could translate into an improvement in the operational performance. Further, ECC's expertise in active manufacturing should benefit SCI given the latter largely depends on imports of key molecules. Thus, a reduction in import and likely improvement in captive consumption should aid gross margins and thereby OPM. Given that no major capex is lined up in the coming future, the company should generate decent FCF in the years to come," said ICICI Direct which initiated coverage on the stock with a buy rating and arrived at a target price of Rs 280.

Berger Paints: Buy | Target: Rs 595 | Return: 12.3 percent"Berger Paints is likely to report revenue, earnings CAGR of 11%, 32%, respectively, in FY19-22E supported by elevated margins (backed by benign raw material prices) and lower corporate tax. Further, with the dominance of limited players and intact long term growth drivers, the premium valuation of the company is justified due to its robust fundamentals (strong distribution, debt free status and consistent positive CFO)," said ICICI Direct which initiated coverage on the stock with a buy rating and a target price of Rs 595.

Minda Industries: Buy | Target: Rs 300 | Return: 12.9 percent"MIL is uniquely positioned in the domestic auto ancillary space as a provider of a wide variety of product solutions straddling established and growing opportunities. The company is also one of the few credible players in the high growth potential segments of airbags and alloy wheels. MIL possesses a steady state organic business riding on value migration i.e. higher kit value. We like MIL courtesy its progressive product profile, healthy capital efficiency and consistent positive CFO generation," said ICICI Direct which initiated coverage on MIL with a buy rating, valuing the stock at Rs 300.

Cera Sanitaryware: Buy | Target: Rs 3,073 | Return: 39.5 percent"Cera Sanitaryware (CRS) is expected to increase its revenue/PAT at 7 percent CAGR, over FY18-22 amid series of challenges including GST, demonetisation, overall lull in the economy and the current COVID-19 crisis. In the same period, EBIT margin is likely to improve to around 15 percent from 13.9 percent and return on capital employed (ROCE) is expected at around 19 percent. Like combating the difficult phase of GST and demonetisation, we expect CRS to overcome even the current challenging situation post COVID-19. As the company continues to outsource manufacturing, its capex requirement remains limited," said Centrum Broking which initiated coverage on the stock with a buy rating and target price of Rs 3,073.

Kajaria Ceramics: Buy | Target: Rs 508 | Return: 49.3 percent"Kajaria Ceramics' (KJC) prudent capital allocation, strong focus on balance sheet strengthening and sharp eye on EBITDA margins will assist in maintaining its leadership position and gear up for strong leaps as business cycle reverses. With healthy return ratios and margins, KJC will be the best bet in the industry. We value KJC at an average of 15-year long business cycle and past five years (to capture the recent earnings trend)," said Centrum Broking which initiated coverage on the stock with a buy rating and arrived at target price of Rs 508.

Adani Ports: Buy | Target: Rs 390 | Return: 42.8 percent"Adani Ports and Special Economic Zone (APSEZ) is rapidly consolidating its position with targeted investments and acquisitions aimed at expanding its hinterland coverage. APSEZ's front ended investments and strong partnerships have led to rapid cargo scale up with around 60 percent of the cargo being sticky," said Centrum Broking which initiated coverage on APSEZ with buy and a price target of Rs 390.

"While we expect 3.7 percent decline in cargo growth in FY21 for existing assets, we see APSEZ being well placed to capitalise on a likely growth recovery in FY22. Core EBITDA CAGR of 15.8 percent over FY20-22 and robust operating cash flows support capex and acquisition plans. While Net Debt/EBITDA should expand to 3.9x in FY21 due to KPCL acquisition, we expect it to revert to 3.1x by FY22," it added.

Gujarat Pipavav Port: Buy | Target: Rs 72 | Return: 31.4 percent"Gujarat Pipavav Port's (GPPL) container cargo growth has trailed industry due to loss of services caused by consolidation in the shipping industry. Realisations and margins meanwhile have sustained outside of impact of an adverse cargo mix. While we expect 8 percent decline in container cargo volumes in FY21 (13 percent growth in FY22 on a low base), cash flows should remain strong led by absence of debt or significant capex commitments," said Centrum Broking which initiated coverage with buy rating and DCF based price target of Rs 72 per share.

"The stock factors a prolonged growth slump with reverse DCF implying 0 percent CAGR in container cargo till September 2028 (end of the concession period – assuming no extension). GPPL’s strong credentials and historic dividend yield of 6.4 percent protects downside," it added.

UPL: Buy | Target: Rs 500 | Return: 38.7 percentEmkay Global initiated coverage on UPL with a buy rating and a target price of Rs 500 with overweight stance in sector EAP. "Market share gains, merger synergies and deleveraging should drive re-rating."

"UPL has been gaining market share over the last five years despite flat industry growth, driven by new products and geographic launches. With the acquisition of Arysta, UPL has been able to fill portfolio gaps in major geographies and is poised to gain market share," the brokerage said.

"EBITDA margins started to improve from Q3FY20 (466bps YoY) as merger synergies kicked in. With better margins, reduction in working capital days, UPL's net debt/EBITDA should improve to 2.2x in FY22E from 3.5x in FY20," it added.

Dr Lal PathLabs: Buy | Target: Rs 1,762 | Return: 10 percent"Dr Lal PathLabs' (DLPL) Revenue grew at a 16.2 percent CAGR (FY15-19), helped by strategic business model and wide network. Factoring in coronavirus impact for Q4FY20 and early FY21, we estimate revenue to grow at a 14.0 percent CAGR FY20-22E. EBITDA margin remained in the range of 24-26 percent over FY15-19. Given the fixed costs of 48-50 percent, we expect EBITDA margin to remain under pressure for FY21E (24.5 percent) and expand in FY22E (25.8 percent)," said Geojit Securities which initiated the coverage with a buy rating on the stock and a target price of Rs 1,762.

Company has solid balance sheet, with no debt and cash & cash equivalent of Rs 775 crore as on December 2019, it added.

Cochin Shipyard: Buy | Target: Rs 356 | Return: 45.3 percent"Due to its expertise in shipbuilding & ship repairing and strong, long lasting relations with its key clients, Cochin Shipyard (CSL) is benefitted to provide important warship products in the coming years. The order book size of these projects is at a healthy Rs 15,300 crore to be delivered over the next 2-3 years. This visibility is enough long term and will lead to a good growth in revenues and profitability. Considering its strong order book with IAC and ASWC projects at the helm in the shipbuilding business, expectations of more order wins through RFP bidding, we expect a significant escalation of topline, margins and bottomline from FY21 over an elongated period of 2-3 years," said LKP Securities which initiated the coverage with a buy rating and a target of Rs 356.

On profitability front too, the brokerage expects solid movement driven by higher contribution from competitively bid projects, positive operating leverage, zero LD provisions, higher contribution from the ship repairing projects & capacity expansion, superior efficiency ratios and balance sheet strength.

It anticipates stable return ratios with maintenance of healthy dividend payouts and yield.

L&T Technology Services: Buy | Target: Rs 1,432 | Return: 24.1 percent"L&T Technology Services (LTTS) is supported by a proficient management team and promoters, wherein LTTS enjoys a strong execution track record and its positioning in key markets which are poised to grow fast which will significantly ramp up the company’s operating profitability and hence we believe that LTTS is well positioned for long term sustainable growth. Furthermore, Company will invest in competency building and broadening LTTS presence within each of segments which will make the LTTS more attractive," said Arihant Capital Markets which initiated coverage on LTTS with a buy rating and arrived at a target price of Rs 1,432.

Disclaimer: The views and investment tips expressed by investment expert on Moneycontrol.com are his own and not that of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.