Highlights

LTI Mindtree (LTIM, CMP: Rs 4727, Market Cap: Rs 139,990 crore, Rating: Overweight) had a disappointing quarter as two project cancellations in the BFSI vertical impacted revenue as well as margin. However, order wins were steady. The company has a decent pipeline of efficiency-led cost takeout deals. As these deals ramp up, the company expects to return to the growth path in Q1. It will be focusing on growth rather than margin gains, although the latter remains a medium-term target. In the past three months, the stock is down 25 percent against a 9 percent decline in the IT Index and a 4 percent gain in the Nifty. The valuation is gradually turning reasonable for a staggered accumulation.

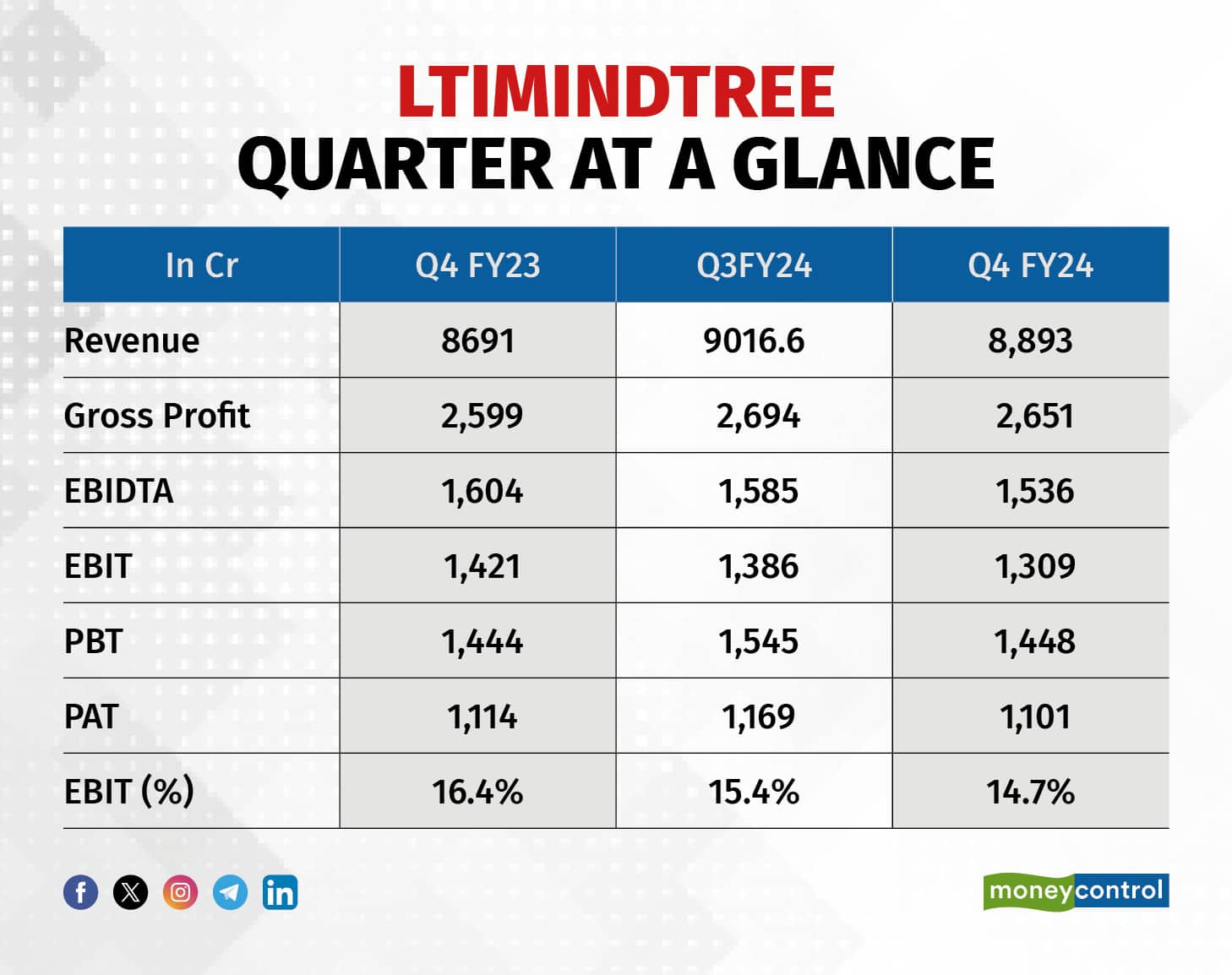

Challenging quarter due to project cancellations

Source: Company

Source: Company

Revenue miss primarily due to one-offs

The company saw two project cancellations in the BFSI (banking, financial service & insurance) vertical as the client reprioritised spending. The revenue for the quarter at $1069.4 million exhibited a sequential decline of 1.3 percent both in reported currency as well as constant Currency (CC). In terms of industry, besides BFSI, manufacturing showed a sequential decline in Q4 due to higher pass-through revenue in the preceding quarter. All the three geographies of North America, Europe, and the Rest of the World were soft during the quarter.

Source: Company

For FY24, revenue at $4.3 billon showed a growth of 4.4 percent in reported currency and 4.2 percent in Constant Currency.

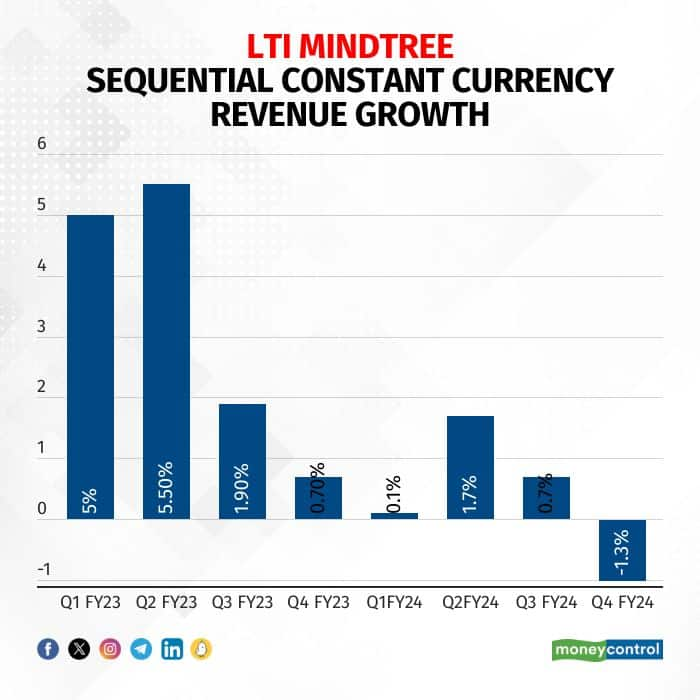

Guiding to a better Q1

The nature of the deals has changed from discretionary to long-term efficiency, leading to a divergence in the order wins and revenue growth so far. However, LTIM has seen quite a few large deal ramp-ups and expect revenue to be back on the growth path from Q1. Overall, FY24 was marred by lower discretionary spend and a decline in growth among its top 40 customers.

Source: Company

Source: Company

For FY24, order bookings at $5.6 billion were up 15 percent. The company alluded to having a good pipeline of cost takeout deals.

Project cancellation impacted margin, improvement target pushed out

LTIM reported a sequential decline of 70 basis points in operating margin, thanks to the 80 basis points hit coming from project cancellation and another 60 basis points from higher sales & marketing expenses and depreciation. These were partially offset by a positive impact of 70 basis points from the reversal of furloughs.

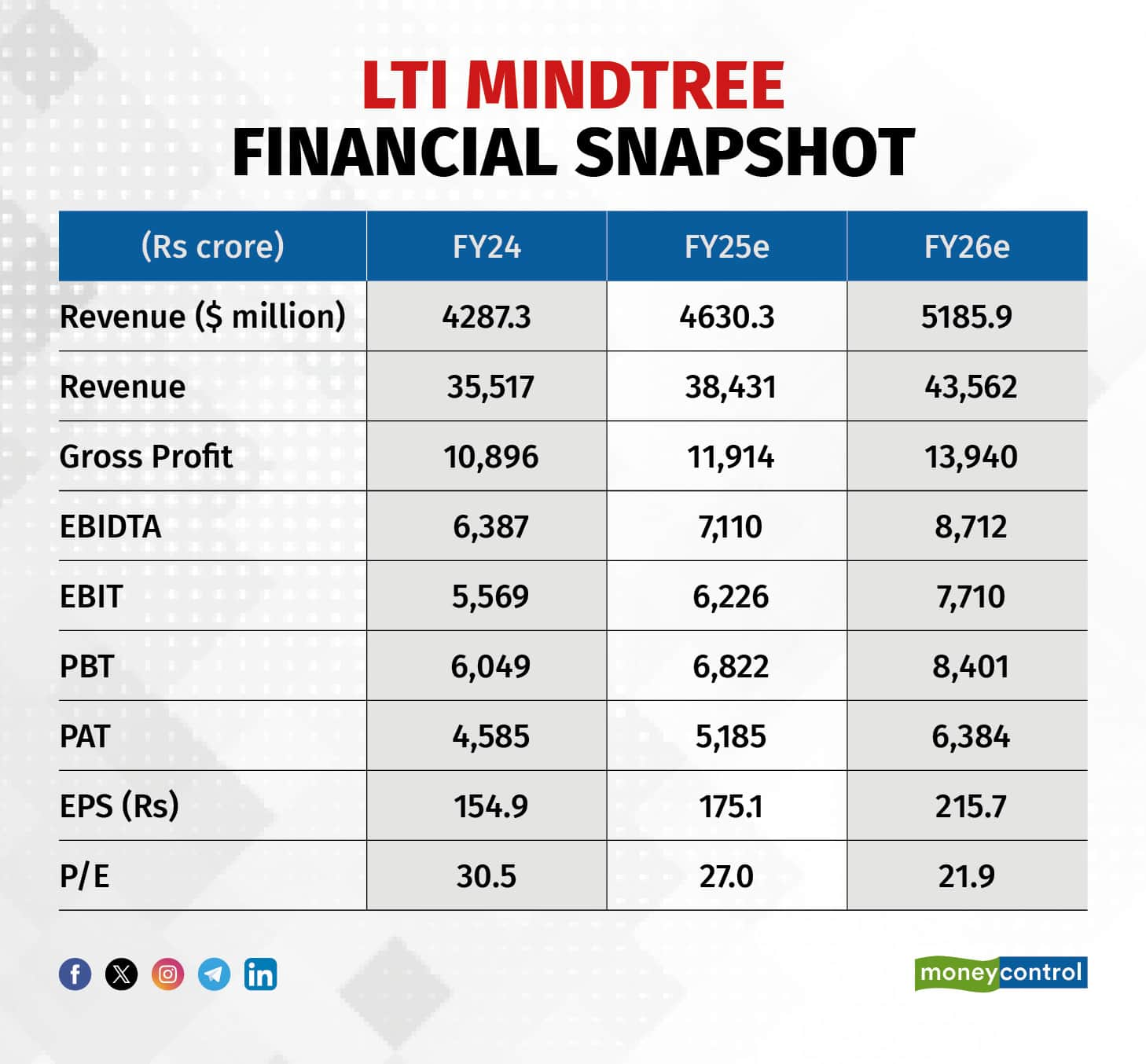

As revenue picks up, in the absence of one-off, margins should gradually improve. However, the company would like to invest in the business for growth and is, therefore, pushing back achieving the intended margin band of 17-18 percent by a few more quarters.

The supply-side challenges are waning with attrition stabilising around 14.4 percent. While the company added freshers in the quarter, net headcount addition declined. Given the elevated utilisation of 85 percent, we expect LTIM to start building up a bench to capture future growth.

Thanks to the stock’s underperformance following tepid result and outlook post Q3, the valuation is now beginning to turn reasonable. Despite the big miss in the current quarter, we see limited stock downside and recommend a gradual accumulation.

Source: Company, Moneycontrol Research

Source: Company, Moneycontrol Research

Key risks: Severe macro challenges impacting technology budgets and orders

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.