The Insolvency and Bankruptcy Code, 2016 will soon complete two years of operation. So far, the Code's performance has been evaluated from three perspectives in popular discourse: jurisprudence in individual cases, outcomes of cases (resolution vs liquidation) and absolute recoveries for creditors in large cases. These perspectives offer valuable insights on the working of the Code at the ground level. However, a baseline of pre-defined parameters against which the Code can be measured on an ongoing basis, is equally critical.

In this article, we construct a baseline for a wholesome evaluation of the Code's performance. The Report of the Bankruptcy Law Reforms Committee, as the birthplace of the code, defined three specific objectives underlying the Code. One, low time to resolution. Two, low loss in recovery and three, higher levels of financing across debt instruments.

We use these objectives as parameters for measuring the Code's performance, using data from the Insolvency and Bankruptcy Board of India (IBBI); and the FRG Insolvency Cases data-set which contains hand-coded information from the final orders of the National Company Law Tribunal (NCLT) that either admit or dismiss an insolvency petition filed under the Code.

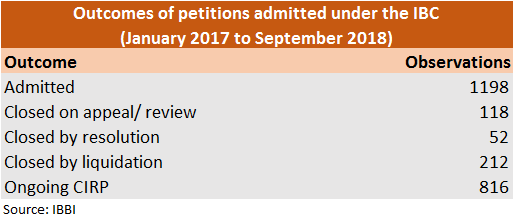

Out of the 264 cases that have seen an outcome post admission, about 80 percent have been liquidated and the rest resolved. While these numbers may, at first blush, indicate a liquidation bias, the text of the Code is agnostic to the outcome. It merely defines the timelines and processes to be followed. However, it must be noted that the Supreme Court, in the Arcelor Mittal case, read the regulations enacted by the IBBI under the Code as favouring a resolution over a liquidation. For the time being, we do not factor this development in our baseline.

Objective 1: Low time to resolutionData on three timelines is imperative to ascertain the overall time taken for resolving or liquidating distressed assets: (a) the date of filing of a petition to the date of its disposal by the NCLT; (b) the date of admission of an insolvency petition to the date on which the resolution plan is approved or liquidation is ordered, by the NCLT; and (c) the date on which a resolution plan is approved or liquidation is ordered to the date on which such resolution or liquidation is completed. While the Code specifies outer timelines for (a) and (b), it leaves open the span of the repayment schedule under a resolution plan to the creditors' committee. The regulations issued under the Code also envisage an outer timeline of two years for completing liquidation. However, there is no public data on the liquidation process. Hence, we limit our assessment to whether the timelines in (a) and (b) are being met.

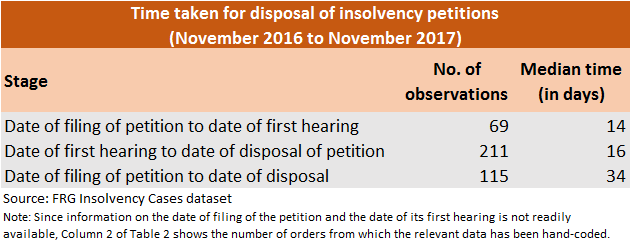

The Code specifies that insolvency petitions must be disposed of within 14 days from the date on which they are filed before the NCLT. While the Supreme Court interpreted this provision to be directory and not mandatory, we use the 14-day period as a benchmark for the purpose of our measurement.

Table 2 shows that 50 percent of the cases studied took up to 34 days for disposal from the date on which they are filed. Also, 50 percent of the cases studied took up to 14 days to reach the stage of the first hearing.

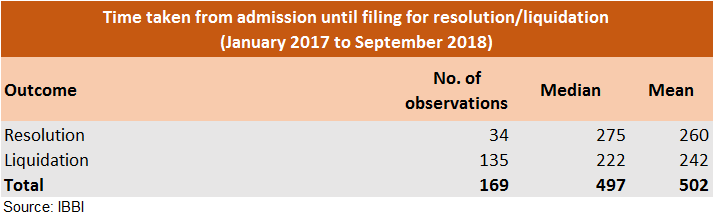

The Code prescribes a 180-day timeline for arriving at a resolution (which is extendable to 270 days with the approval of the NCLT) failing which the case has to go for liquidation. The Supreme Court has interpreted this timeline to be mandatory. The average (mean) time for resolution and liquidation outcomes are slightly within the 270-day outer timeline. Thus, it is clear that the 180-days timeline is being extended for a large number of cases. The law requires such extensions to be granted for reasons to be recorded by the NCLT in writing, and the Supreme Court has underscored the importance of this requirement in subsequent case-law. Deeper research is needed to understand the nature of cases for which an extension in the timeline is routinely granted by the NCLT, and the reasons for which such extension are allowed.

For the cases which are undergoing resolution (as on September 2018), the data published by IBBI shows that 30 percent of cases have already exceeded the 270 day timeline. A strict interpretation of the law would require the liquidation of such debtors. However, the sanctity of these timelines have, to a large extent, been diluted by the judgement of the Supreme Court in the Arcelor Mittal case, where it held that the time taken in litigation over an application ought to be excluded when computing the 180 days or 270 days’ timeline mandated under the IBC. Be it due to the dilution of timelines on account of exemptions arising out of ongoing litigations or the general aversion to liquidation as an outcome, these cases are categorised as those in which the resolution is still ongoing.

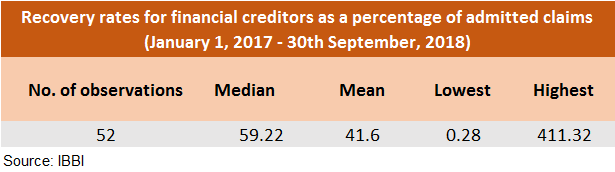

Objective 2: Low loss in recoveryThere is no ideal or benchmark recovery rate for an insolvency regime to be termed successful. However, the World Bank's Ease of Doing Business Survey of 2015 observed that the debt recovery rate in India hovered around 20 cents to the dollar, and OECD countries had a recovery rate of 72 to the dollar.

Table 4 shows the recovery rates for financial creditors computed on an absolute basis, that is, the value of the resolution plan against the value of the admitted claims of financial creditors. These are first estimates of the recovery rates for financial creditors. However, the numbers must be discounted by the costs associated with the resolution and other factors such as the time span for repayment and the conditionalities, if any, attached to the repayment schedule. Having said this, a plain comparison with the World Bank’s 20 percent recovery rate shows that the numbers are perceptibly higher.

The recovery rates for operational creditors are not as easily and credibly discernible, and more effort needs to be concentrated on that front.

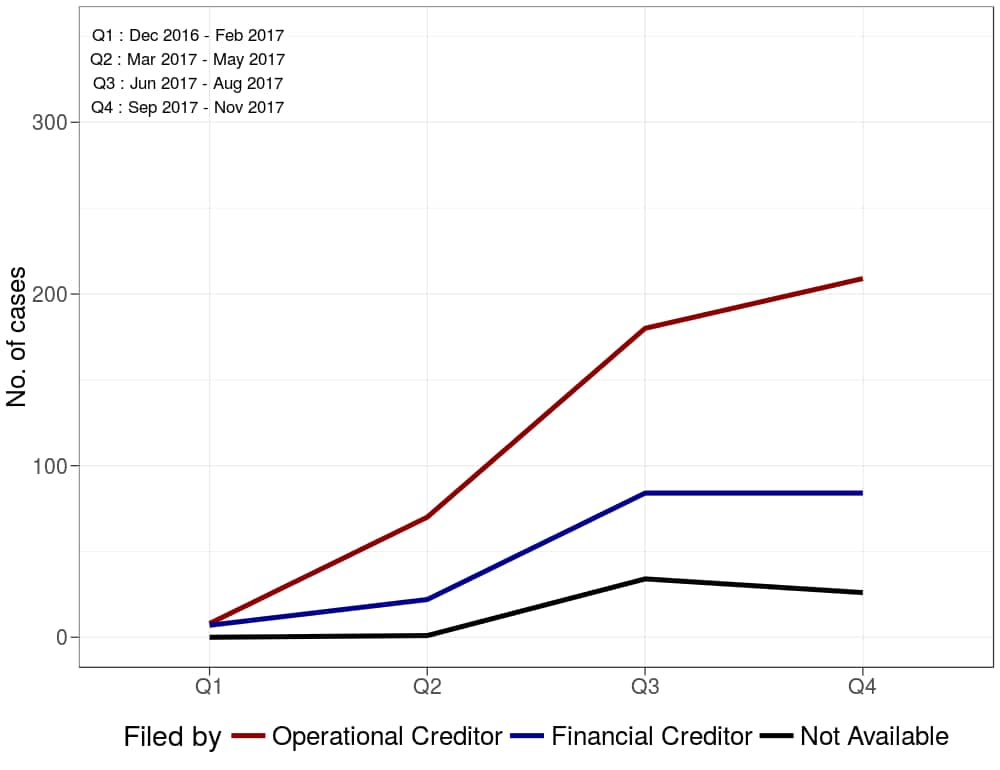

Objective 3: Impact of the law on credit marketsIt is too soon to observe changes in financing patterns across debt instruments. However, on the basis of publicly available data, we use the kinds of creditors using the Code as a proxy indicator of financing patterns. The idea is that if a particular set of creditors finds the Code effective for enforcing their claims, it will likely positively impact the cost of that credit channel.

The chart clearly shows that operational creditors have triggered the Code extensively (and in higher proportion) to financial creditors. These creditors, comprising largely vendors and employees, are unsecured creditors who hitherto had no effective remedy for recovering their dues, except civil suits and the initiation of winding up proceedings before the court against the debtor.

ConclusionTo sum up, there are three takeaways from this analysis of two years of the Code.

First, that the timelines set by the Code are being reasonably met with transgressions that are arguably minor.

Second, that the absolute recovery rates for financial creditors are higher than the number that was ascribed to India in 2015. With the availability of sufficient data on actual recoveries on a NPV basis under resolution plans, a more meaningful analysis of the performance of the Code would also be possible.

Third, operational creditors find the Code an effective tool for realising their claims.

In the context of measuring outcomes, the role of the institutions under the Code — the NCLT, the NCLAT (which is the appellate tribunal in which, anecdotes suggest that considerable time is spent by parties appealing against the orders of the NCLT), the regulator and the insolvency professional agencies — in disseminating information cannot be understated. While the IBBI has taken significant steps in this direction, the tribunals and other institutions must be more forthcoming with ease of accessing the data. In short, a more robust assessment of the Code's performance in the future will warrant equally robust information systems.

(The authors are researchers at the Finance Research Group at IGIDR. This article summarises parts of the presentation made at the annual INSOL India Bankruptcy Conference held in New Delhi on November 13, 2018.)

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.