Newly listed companies from the financial sector appear to have caught the fancy of investors. While the three companies we are referring to namely, AU Small Finance Bank, CDSL and Hudco, were highly recommended by us at the time of the IPO, the recent surge in their stock prices has made us turn cautious. On the other hand, there are some other companies in the sector that have produced tepid results but are attractively valued, to our minds, especially when compared to the irrational exuberance that has hit the recent IPO candidates. When will investors start respecting valuations?

Where is the froth?The recently listed companies undoubtedly bring their own unique moats to investors. AU ran a successful small lending business and under the umbrella of a bank it will still grow at a brisker pace despite the small compression in margins. Hudco, the government-owned lender to housing and urban infrastructure projects, has ample avenues for growing the loan book even within the rather de-risked business model where exposure is confined to entities backed by the government.

The uniqueness of CDSL’s business model is obvious: An efficient depository in a duopoly market that is now exploring multiple avenues of growth.

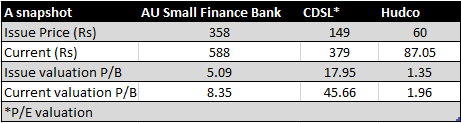

However, somewhere while appreciating the strengths of the businesses, investors have taken their eyes off valuations. From the offer price, AU, CDSL and Hudco had rallied to the extent of 102 percent, 226 percent and 70 percent, respectively. While the correction wasn’t unexpected, even after the recent decline, the valuation at the current level doesn’t lend comfort.

Consider this, at the current level, on the basis of trailing multiples, AU Small Finance Bank is costlier than Bajaj Finance, an entity which is over six times its size and has impeccable track record. For CDSL, the current valuation is 53 percent costlier than its parent, BSE. For Hudco, at the current price, while the downside might be limited, upside is contingent on future earnings traction.

The value that we may be missing.Now, consider the recent earnings of some of the smaller banks – DCB Bank, Karnataka Bank and South Indian Bank.

DCB BankDCB Bank has been a steady performer. In the quarter gone by earnings grew by 39 percent aided partially by treasury gains.

Asset quality was a tad disappointing with sequential growth of 12 percent in gross NPL (non-performing loans). The bank has a mortgage-heavy book with a very small corporate book.

While valuation at 2.4X FY17 adjusted book looks fully priced, we focus on a differentiated matrix to look at banks for the next few years.

With the increasing irrelevance of state-owned banks in the banking business (both in credit as well as deposits), their savvy private counterparts are steadily and swiftly garnering market share and hence, unless weighed down by asset quality woes, these banks are likely to be long-term survivors in the transformation that the Indian banking space will witness.

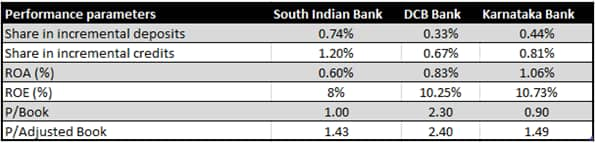

While DCB has a minuscule 0.18 percent share in total bank credit and a similar share in advances, its share in incremental deposits and advances last year have been 0.33 percent and 0.67 percent, respectively. This lends comfort. Hence, notwithstanding the 94 percent run-up in the stock in the past one year, we would be waiting for opportunities to accumulate DCB for an earnings growth trajectory in mid-twenties.

Karnataka Bank – the inorganic growth target?In contrast, the cheap valuation of Karnataka Bank still doesn’t quite get us excited other than the possibility of the inorganic buzz that keeps coming up. In the current scenario we do not consider the same as a high probability event.

In the quarter ended June 2017, while the reported profit went up by 10 percent, asset quality showed no signs of improvement and the bank has a poor coverage ratio. The reported valuation at 0.9X FY 17 book looks extremely undemanding but if one prudently adjusts for the asset quality including the restructured assets, the valuation takes a completely different colour - 1.5X FY17 adjusted book. However, on the key matrix that we track, namely, the share in incremental business, Karnataka Bank doesn’t fare too well.

Karnataka Bank has a minuscule share in overall bank deposits and credit at 0.53 percent and 0.50 percent, respectively and while in incremental credit its share is 0.81 percent, in incremental deposits it is only 0.44 percent. With the share of corporate book at 48 percent, may be a big one time clean up can provide good entry opportunity.

We have turned more constructive on South Indian Bank that also reported its numbers in recent times. The muted bottomline performance was on account of a steep increase in provision. Asset quality also worsened with a 48 percent sequential rise in gross NPA. However, with the bank recognising the entire stress of its watchlist in this quarter, incremental pain would be limited.

On the key performance parameter of share in business, there are reasons to feel comfortable. While South Indian Bank, like its peers discussed above, has a small 0.62 percent share in banking system’s credit and deposits, its share in incremental banking system’s deposits stood at 0.74% and in incremental credit it was at an impressive 1.2 percent.

The reported valuation at 1X FY17 book looks extremely reasonable even in the context of the rather unimpressive return ratios. However, even if we adjust for the entire stress in its book, the valuation at 1.43X adjusted trailing book leaves enough room for rerating once the cycle turns and the legacy woes are behind.

We caution our investors not to be carried away by irrational exuberance, keep a hawk eye on valuation and evaluate every idea on its individual merit for a rewarding investment experience.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.