“The pace at which circulars are issued by regulators in India, fintechs are super confused—(wondering) if they should be hiring computer science engineers or compliance officers.” When Pravin Jadhav tweeted that message with a tearful smiley face on September 30, it was only half in jest.

The founder of Raise Financial Services, which operates stockbroking platform Dhan, was ruing the onslaught of circulars from the Reserve Bank of India, the banking regulator. Fintechs have been at the receiving end of those diktats.

For a while back in 2021, the question that was often asked, despite the sharp disparity in their size, was: will fintechs be a threat to banks? Today, the RBI has left no one in doubt about the answer, going by the slew of circulars that it has issued to rein in fintechs.

Indeed, the lay of the land was very visible at the Global Fintech fest in Mumbai’s Bandra Kurla Complex, which RBI governor Shaktikanta Das addressed on September 21. The mega fintech event was a prestigious affair, on par with global events in terms of its scale. The central bank governor’s attendance underlined that prestige.

But, despite it being the Global ‘Fintech’ Fest, the first two rows were reserved for marquee private and public sector bank heads, representatives from the RBI, as well as the top management of the National Payments Corporation of India (NPCI). The fintech bosses were lurking somewhere in the background, unseen and unheard.

The optics said it all.

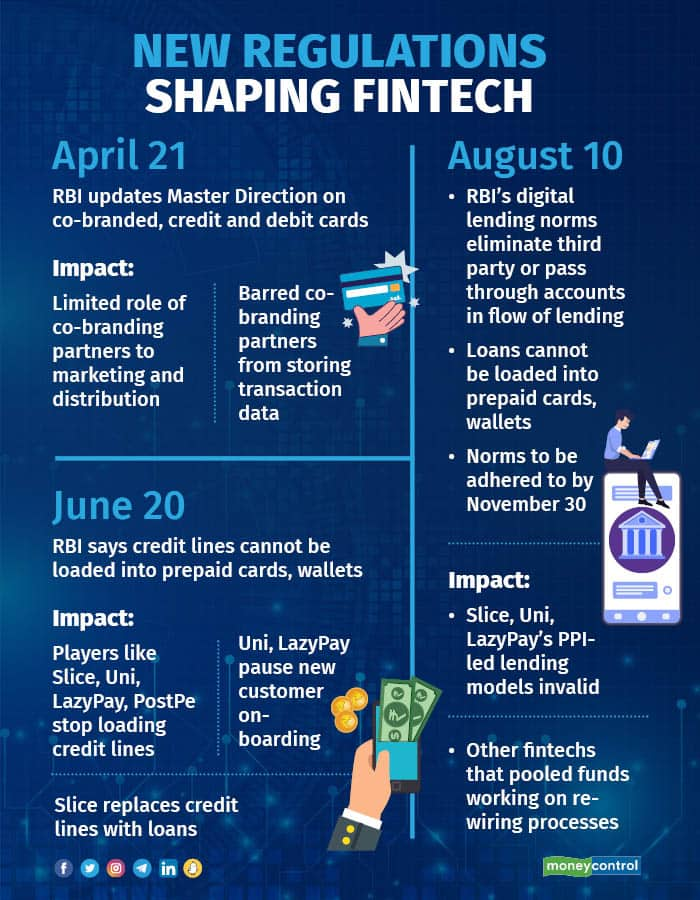

Background: A shift in the landscapeThe first indication from the RBI that the ground beneath fintechs’ feet was going to shift was a change in the Master Directions for co-branded credit and debit cards. The change limited the role of co-branding entities to marketing and distribution of credit or prepaid cards, casting a shadow over the viability of the business models of card issuing fintechs such as Slice, Uni, OneCard, BharatPe's PostPe and PayU’s LazyPay.

Not long after, in a surprise notification sent directly to fintechs, the RBI said that loading a credit line into prepaid cards was prohibited. Following this change, Uni and LazyPay paused new customer onboarding, while Slice replaced free-to-use credit lines with short-term loans on demand.

And then came the big one. On August 10, new guidelines on digital lending mandated that all loan disbursals and repayments had to happen to and from bank accounts of the regulated entity lending money and collecting repayments. The transactions could not pass through a pool account or any third party.

Following the announcement, State Bank of Mauritius Bank India, which had partnered with many fintechs for their prepaid cards and wallets, asked them to stop onboarding new customers. Uni also stopped disbursing credit to existing customers after the norms came out.

The RBI has also made it mandatory for online payment aggregators to operate with a licence, adhering to a set of norms. The licence regime will also be extended to offline payment aggregators in the coming months.

The fusillade of circulars has knocked the fintech industry off its feet, forcing it to scramble for compliance.

“There have been a number of new guidelines for the sector that impact our product development. For now, we will simply look to close the year stabilising existing products and driving up compliance in accordance with the digital lending guidelines. With frequent changes and re-wiring of products, there is a customer impact, which we are sensitive to. The RBI has made it clear we have to stay in our respective lanes and do what we are authorised to do,” said a top executive at a lending fintech company.

RBI Governor Das said as much at the Global Fintech Fest. “The fintech road ahead will witness ever-growing traffic in addition to the large number of existing players who are already there. It is, therefore, imperative that every player on this road follows the traffic rules for their own safety and the safety of others,” the Governor said.

A change in approachThe exclusion of pass-through accounts including prepaid wallets and cards and even payment aggregators in the flow of lending struck down the core models of fintechs such as Slice and Uni, which had raised millions in funds over the past year. Slice raised a total of $270 million in the last two rounds, and Uni last raised $70 million in December 2021.

The changes have left these fintechs with no business model in the midst of a tough funding year. And they have created a sense of fear among founders of other fintechs and left them wondering if there could be more such shocks that could get them into trouble too.

It’s a far cry from last year. In 2021, Indian fintechs appeared to be on a golden run as funds poured in. They used the venture capital aggressively to market products, as well as provide cashbacks and rewards to gain customers. A lot of the funding was used for catchy advertisements and ad campaigns during the Indian Premier League (IPL) T20 cricket tournament, as well as team sponsorships.

Companies with unregulated business models, flashing VC money, and adding customers at a fast pace in a sensitive area such as financial services seems to have been one of the things that caught the regulator’s eye. Fintechs seem to have read the tea leaves now.

“We have cut down our burn rate. We don’t want to spend on marketing ourselves a lot anymore. We also don’t want to suddenly be noticed as growing too fast,” a fintech founder candidly told Moneycontrol.

According to data by Venture Intelligence, the amount raised by fintechs in the first nine months of 2022 stood at $4.8 billion, down 8 percent as compared to $5.2 billion in the first nine months of 2021. It also took more rounds to raise the funds in 2022, indicating smaller round sizes. In all, 195 fintech deals were executed in the first nine months of 2022, versus 164 rounds in the same period last year.

Overall private equity and venture capital funding to Indian startups slowed more than 20 percent in the first 9 months of 2022, per data from Venture Intelligence.

This shift reflects a change in the approach by fintechs over the past year, when growth took precedence over everything else. What has added to the mix is the global rout that made investors cautious and more focused on profitability and unit economics. After the past few months, they have also become more cognisant of the changing regulatory environment.

“Banks and the RBI have a very strong legacy relationship and there is a well-oiled protocol on how that works. Whereas, with respect to fintechs, there is a very steep learning curve, which is going to come with a little more time and patience. So, we will see a little bit of a power struggle between the banks and the fintechs,” Ashish Fafadia, Partner at Blume Ventures, which has invested in fintechs such as Slice, Turtlemint, Smallcase etc, told Moneycontrol.

Fintechs do feel that things have changed for the better since the regulator has been engaging much more with them, separately as well as through representative bodies. The frequency of interactions has increased since the beginning of this year. The RBI setting up a separate fintech department helped the cause further.

But, a lot of these conversations seem to be one-way — the regulator listens to the fintechs, but does not reveal what it plans to do. As for how the digital lending norms came into being, the RBI revealed its thinking only with final regulatory announcements.

Many ecosystem players have noted that in the larger universe of the RBI’s responsibilities, fintechs remain a speck, something that does not merit a lot of its energy.

“The general vibe at the RBI is that fintechs are using loopholes. So, there is some brand building that fintechs have to do to show they are actually adding value to the ecosystem and not just not trying to create valuation using loopholes,” said a founder. “The RBI does not see these digital initiatives as a big gain to the ecosystem. Because, if fintechs don’t do it, the traditional players will eventually do it.”

According to Subhash Chandra Garg, former Finance Secretary, "The tussle is between the regulator, which favours banks to be the final and effective lender, whereas the fintech world, aided and abetted by NBFCs, is interested in becoming the real face of lending. Banks may not be very good in delivering tech-based credit solutions. But, the regulatory regime will slow down fintech adoption in the credit space. "

In that backdrop, if something seems risky to the consumer, the regulator is okay with striking it down without any discussion.

“There is a massive difference in the way the regulator interacts with banks and fintechs. With banks, they engage and respond. With fintechs they just listen and move on,” revealed a banker.

No way around regulationsMost players in the ecosystem believe that the RBI’s concerns around how customers may be misled by a card form factor are genuine. For instance, a number of customers took to Twitter earlier this year to say that they were not aware that their Slice cards were not credit cards, and that they were in fact taking a loan while using a card. The worry was also that customers would not be aware of which entity was the actual lender, which in most cases is an NBFC or a bank and not the fintech itself.

“It was also the bravado with which a number of founders were doing it. They were often talking about how credit cards are bad,” said the founder of a lending platform.

As soon as these startups were pushed to focus on profitability, they had to do away with the high-burn, interest-free option of repaying in three parts and charge interest rates that were higher than those levied by credit cards, in some cases. On top of this, there are processing fees and each transaction is counted as a fresh loan, unlike in the case of credit cards.

However, the potential of fintech-led lending remains immense. According to the Chiratae and EY report, lending AUMs in Indian fintech have the potential to grow from $38 billion currently to $515 billion by 2030.

"Money does not lend itself. It requires intermediaries and this technological innovation is very much essential for credit to expand. If we say that fintechs should become subservient to banks, who are the real lenders, then the innovation needs to come from the banks themselves. But, the banks are not in a position to do that," Garg explained.

Fintechs themselves are to blame for the mistrust, if any, towards the ecosystem, said Jaikrishnan G, Partner and Head of Financial Services Consulting at Grant Thornton Bharat. “Because important aspects of compliance were squarely overlooked. Only when the regulator starts taking action and enforces norms are you worried about complying.”

Fafadia subscribes to the view that the regulator was right to step in, and that the intention was not to slow things down. But, a balanced approach is what is needed to help the ecosystem grow further, he noted.

Now, neobanking platforms such as Jupiter, Fi, Freo, Open, RazorpayX and Niyo are waiting to see how the RBI views their operating sphere.

“There are provisions within RBI regulations that will empower them to take a company-by-company view. Over a period of time, it will come down to that. The ecosystem stands to benefit once that starts happening,” said Fafadia.

In the long run, the new norms may be the best thing to happen to the fintechs, their customers, their partners and the entire ecosystem. And some day they may thank the RBI for its tough love.

Together, they can; but will they?Experts believe that this year will separate the stronger and resilient business models from the ones that lack a real proposition. This is aided by the combination of the slowdown in funding and increased regulatory scrutiny.

“Going forward, it will be about innovating within the regulatory parameters. Companies will stand out if they solve real world pain points,” said Ramkumar Thirumurthi, co-founder and COO of B2B embedded financial solutions platform Actyv.ai.

Bank and fintech partnerships, too, will be more important than ever, for both parties. The narrative can no longer be about banks versus fintechs, but about banks and fintechs that embrace partnerships on one side and those unwilling to join hands on the other side.

For banks, too, fintech tie-ups help in growing their reach, in lending to the underserved, and in gaining tech capabilities they do not possess. Fintechs, on the other hand, cannot replace large institutions such as banks and function alone.

“Fintechs that had basic propositions of just faster underwriting and disbursals are unlikely to survive. That proposition is no longer valid. The ones bringing in more product innovations, personalised loans, repayment options and other services that improve the quality of financial services will strengthen further,” added Jaikrishnan.

Over the past year, lending emerged as the only means for fintechs to generate revenue even if their core offering was different. Going forward, fintechs may need to charge users for other offerings such as neobanking capabilities, payments etc, to stay viable, say experts.

The upside is that both the Government and the RBI are in favour of further digitisation. In Garg's view, there will soon be a realisation that banks cannot achieve the reach that tech-first fintechs can propel on their own.

“There will be a realisation on the part of the banks, government, as well as RBI, that this is not working out. If they are able to overcome that resistance, between the real ambition and the way to get there, then there will be a revision. We will then probably have a transition towards more fintech-led arrangements. But it is difficult to say how long that will take,” he said.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.