After a two-year delay, third-party motor insurance premium rates are set to go up, starting this month. The Ministry of Road Transport and Highways and the Insurance Regulatory and Development Authority of India (IRDAI) released the final third-party liability premium rates last week.

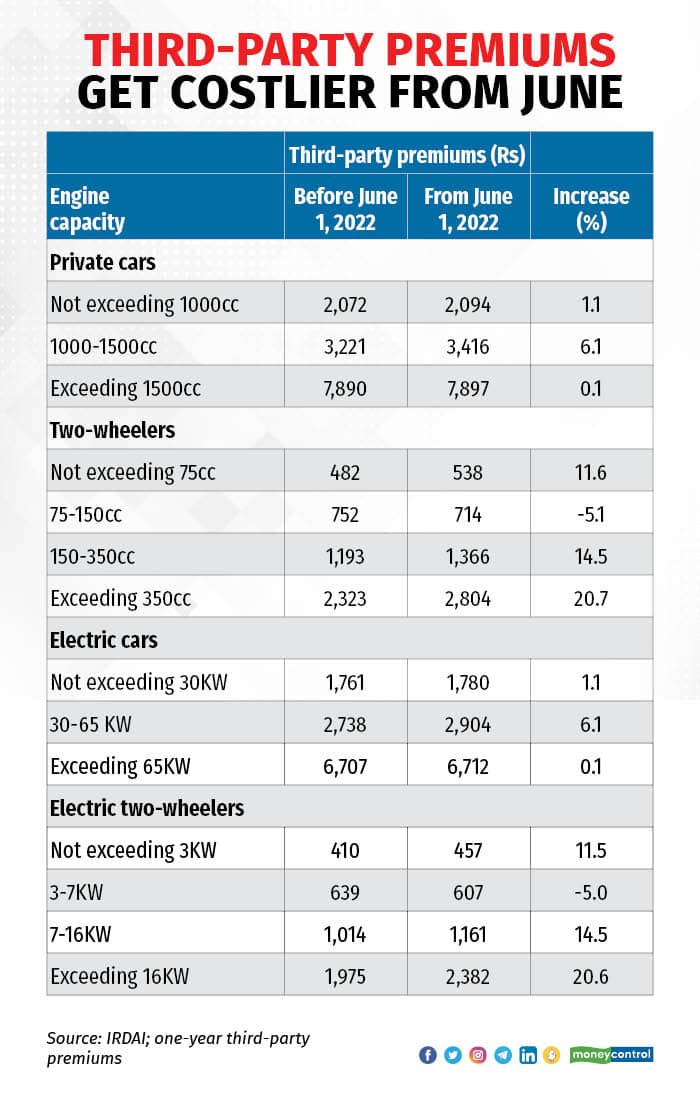

For car- and two-wheeler owners, the hike is in the range of 0.1-20.7 percent, depending on your vehicle’s engine capacity (see table). For example, third-party motor insurance premiums for private cars with engine capacities of 1,000-1,500cc will rise to Rs 3,416, up by Rs 195. Likewise, for bikes with engine capacities of 150-350cc, you will have to shell out Rs 173 more, with third-party rates increasing from Rs 1,193 to Rs 1,366 earlier.

From the insurers’ perspective, this was a much-needed revision. “It has been long-awaited, given the rise in inflation and significant increase in the award amounts granted by courts. The adequacy of the hike can however, be evaluated only after this year, since the last two years were not representative in terms of claims,” says Shanai Ghosh, CEO and Executive Director, Edelweiss General Insurance.

Here’s what you need to know about third-party motor insurance covers, the hike in premiums, and how the move will impact your pocket.

Also read: Third-party motor insurance premiums to go up from June 1 Buying a third-party motor insurance policy is mandatoryThird-party liability is the component of your motor insurance cover that is mandated by law ― no vehicle can ply on the roads without this cover. Put simply, it insures the policyholder against compensation that he/she might have to pay if the vehicle were to be involved in an accident, causing harm to another individual (third-party). The cover will also pay for any damages to the third-party’s property that your vehicle may have caused. The other component ― own damage ― takes care of expenses you might incur if your vehicle is damaged. However, you are not legally bound to purchase this cover.

Usually, the IRDAI comes up with a proposed third-party rate structure every year in March, which is then finalised towards the end of the month. Final rates are typically lower than the proposed ones. This time round, the insurance regulator proposed hikes in March, but did not notify the final rates ― road transport ministry made the announcement instead, with revisions effective from June 1.

Also, the hikes have come through after two financial years ― they were last raised in financial year 2019-20. The COVID-19-induced lockdown towards the end of March 2020 meant that the annual third-party rate hike could not be effected. “Due to the COVID-19 lockdown, people stopped buying vehicles and existing vehicles were used. Increasing third-party premiums during such tough times would not have been viable. These hikes, post a COVID-19-induced gap, are more or less around expected lines,” Balchander Sekhar, Co-founder, RenewBuy, an online insurance aggregator, said.

Since third-party cover is mandatory, all vehicle owners are bound to feel the pinch, more so, the bike owners in all but one category. “It’s between 11-21 percent for two-wheeler owners. Over 20 percent qualifies as a significant rise, as they will be paying these premiums annually,” says Saroj Satapathy, Chief Operating Officer, JB Boda Insurance and Reinsurance Brokers. Only premiums for bikes with engine capacity of 75-150cc have, in fact, dropped by Rs 38. For car-owners, the increased premium burden will be less taxing, as hikes will be in the range of 0.1-6 percent. From the insurers’ perspective, this was a much-needed revision.

Premiums of electric two-wheelers see spikeElectric vehicles (EVs) will see a rise of 0.1-20.6 percent in their third-party premiums. Again, it’s the two-wheeler space (barring the 3-7kW engine capacity segment) which will bear the maximum brunt in percentage terms. Hybrid EVs will be eligible for a 7.5 percent discount. “Discounts have been provided for hybrid electric vehicles this year. These are good measures that will help boost sales of these segments,” says Ghosh of Edelweiss.

Why it is important to buy own damage coverageWhile buying the own damage component is not mandated by law, you need one to safeguard yourself against financial loss due to accidents and other risks such as natural calamities, fire and burglary. Two-wheeler owners, in particular, should not be tempted to let go of own damage cover due to hike in third-party premiums.

“Having proper insurance for all your assets is a sound financial approach. Own damage cover is meant to protect the value of the car or two-wheeler without denting your pocket due to repair or replacement charges after an accident, irrespective of third-party premium hike. These are two different kinds of risks and should not be traded off. In fact, third-party liability and own damage risks are linked and correlated, because an accident can trigger both. Therefore, take adequate cover for both kinds of risks,” says Srinath, Co-founder and Director, SANA Insurance Brokers.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.