Individual borrowers are set to feel the heat of higher interest rates, with Reserve Bank of India (RBI) governor Shaktikanta Das announcing a massive 50-basis point hike in repo rate on August 5.

This is the third repo rate hike in this financial year, starting with the unscheduled revision of 40 bps (one basis point is 0.01 percentage point) in May 2022. With the latest move, which aims to curb inflation, the cumulative repo rate hike between May and August now amounts to 140 basis points.

All floating-rate retail loans sanctioned by banks after October 1, 2019 are linked to an external benchmark, which is the repo rate in most cases. The latest round of hike will be fully passed on to retail borrowers in the days to come. The effect of the repo rate hike would be felt across all categories of loans, both secured and unsecured.

Also read: RBI hikes repo rate by another 50 bps, so what's next?Home loan borrowers worst hitHome loan borrowers are set to feel the maximum pinch, as interest burden over long tenures will be heavier.

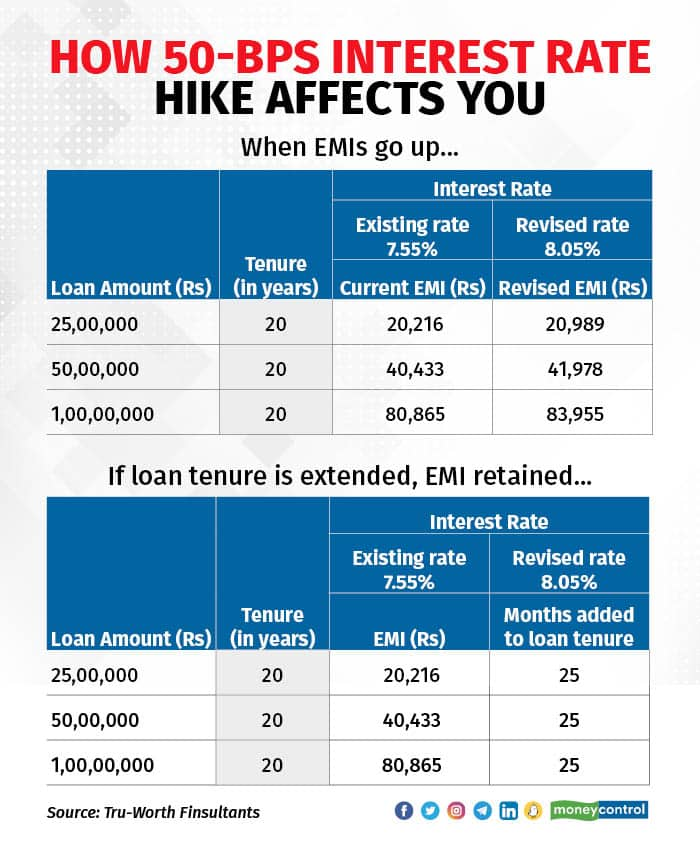

Typically, when interest rates goes up, banks tend to extend loan tenure and not equated monthly installments (EMI) first, pushing up the interest outgo for home loan borrowers significantly over long tenures of 15-30 years. “A home loan borrower with current interest rate of 7.4 percent, outstanding principal of Rs 30 lakh and tenure of 20 years could see his/her tenure being extended by over 24 months,” says Adhil Shetty, CEO, BankBazaar.com.

Larger loans will entail higher interest payouts. For instance, the revised repayment period for a Rs 1-crore home loan with an interest rate of 7.5 percent and original tenure of 20 years (240 months) will be over 22 years (265 months). This means that the interest payout over this period will rise by close to Rs 20 lakh. “If the EMIs are increased instead, you will have to shell Rs 3,085 more every month. The overall increase in interest burden will be Rs 7.4 lakh,” says Vipul Patel, Founder, MortgageWorld, a loan consultancy firm.

What’s more, you will also need to brace yourselves for further hikes. “I foresee another 50 bps hike between December and March 2023. So, home loan borrowers need to tighten their belts to deal with the higher interest outgo,” Patel says. On the upside, home-buyers could see some moderation in property prices. “Benign interest rates had fuelled demand from home buyers. With increase in interest rates, the demand could stabilise and price rise in real estate could be reined in,” he added.

Long-term loans like home loans allow you to make pre-payments. In a rising interest rate environment, rethink your home loan repayment strategy and consider making pre-payments to save on rising interest cost. Just an extra few thousand every month can reduce your interest payout over the long-term.

You must look to prepay lump-sum amounts – by dipping into bonuses or liquidating sub-optimal investments - in the initial years to reduce interest cost. If lump—sum pre-payment is difficult, voluntarily increasing EMI by 5-10 percent or paying off one extra EMI every year can also go a long way in cushioning the impact of rate hike . “An existing borrower can also consider refinancing their loan,” Shetty adds. For example, now as the repo rate is 5.40 percent, the lowest rate for home loan you can get right now may be around the 7.90 to 8.15 percent range. If you are paying higher despite having a good credit score, you can speak to your lender about it and refinance your loan to a lower rate.

Also Read: Key takeaways from the RBI Governor's addressGood times for depositors?Even as borrowers rejig their budgets and repayment strategies, the rate hike is bound to bring cheer for depositors who have had to put up with lower interest rates for a prolonged period of time. Interest rates on deposits are set to rise in the days to come. “However, you may not see the increase immediately. Banks are expected to raise deposit rates in a staggered way to ensure that their cost of funds don't escalate drastically. To maximise your returns, you can go for short-term fixed deposits till the rates rise further. Switch to a higher rate as soon as your short-term deposit matures. Laddering is another way to maximise your returns. It helps you to spread your deposits over different tenures and rates” says Shetty of Bankbazaar.

The rate hike is good news for senior citizens in particular. “For senior citizens looking at short term investment horizon of one to three years, the rise in bank interest rates offers attractive returns. Fixed deposits with 3-5 year maturity terms would now offer 6.5-6.75 percent (pre-tax) as compared to 4.5-5 percent in March 2022. Since there are many taxation benefits offered, those who earn up to Rs 8 lakh and claim section 80 C deductions can earn tax-free returns on FDs,” says Ajay Sehgal, Director, Allegiance Financial.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.