The party is officially over.

Home loan borrowers, who have been used to low interest rates for the last four years, got a jolt on May 4 when Reserve Bank of India (RBI) governor Shaktikanta Das announced a 40-basis-point hike in the repo rate (100 basis points = 1 percentage point). While a rate hike was imminent due to rising inflation, what surprised markets was that Das did not wait till the next monetary policy to make the announcement.

Tough times ahead for borrowersBorrowers who got their home loans sanctioned after October 2019 - when the external benchmarking regime came into force — will see their interest rates inch upwards for the first time. For most banks, the external benchmark to which their home loans are linked is the repo rate. This means that the entire rate hike will be passed on to borrowers. Some banks such as ICICI Bank, Bank of Baroda and Federal Bank have already started raising their repo-linked rates and others will follow suit in the next few days.

The recent key policy rate hike was sharp, but economists predict more hikes will follow this year. “We expect 50-75 bps more in hikes this year — 50 bps for certain and another 25 bps if inflation is stubborn,” said Madan Sabnavis, Chief Economist, Bank of Baroda. Others say the aggregate of the hikes this year could even be as high as 100 basis points over the next 18 months.

Also read: How to cushion yourself against the RBI’s sudden rate hikeThose servicing home loans at 15-year-low rates of 6.5-7 percent could see their interest rates jump to as much as 8 percent in the months to come. This begs the question: if interest rates (on floating rate loans) are going to rise, are borrowers not safer in switching to a fixed loan rate?

“There could be an increase of 50-75 bps by December, and in 18 months, the aggregate rate hike could be in the region of 150 bps. So, by December 2023, those who are borrowing at 6.5 percent now could be borrowing at close to 8 percent per annum,” says Vipul Patel, Founder, Mortgageworld.in, a loan advisory firm.

Also listen: “Brace yourselves for an increase in home loan rates.”Typically, for those with credit scores of lower than 750 or non-salaried borrowers, the interest rates will be even higher. Patel and many other experts say that this is bound to bring the focus back on fixed-rate loans.

The obvious benefit of a fixed-rate home loan is the protection against the vagaries of interest rates.

You can plan your repayments over the long-term without letting EMIs or tenure fluctuations disturb your peace of mind. “The question before the borrower is whether the fixed rate offered today will be lower than floating rates in a year. This is hard to answer. If, in their loan math, refinancing to a fixed-rate option appears better, they should take it. This is assuming that they are offered a fixed-rate loan in the 7.5-8.5 percentage range, (and they are simultaneously) expecting floating rates to hit 8.5 percent in the next two years,” says Adhil Shetty, CEO of Bankbazaar.com, an online loan and credit card aggregator portal. Fixed-rate loans carrying interest rates of over 8.25-8.5 percent will not be worth your while.

The decision will also hinge on your age, remaining loan tenure and your plans to pre-pay the home loan within 5-7 years. “If you are over 50-55, you could look at fixed-rate loans. The scope of extending the tenure and salary hikes would be limited during this phase and, therefore, be inadequate to cushion the impact of floating-rate fluctuations,” says Patel.

The other option would be partially-fixed home loans, where the interest rate is fixed for the initial 2-3 years. For instance, HDFC’s Tru-fixed home loan scheme. “Partly-fixed loans are good options to consider in this scenario. Interest rates in the system will be at higher levels in the next 2-3 years, but could come down thereafter. So, these schemes could make sense to deal with the current rising-rate scenario,” says Patel.

If stability is the key benefit in fixed-rate loans, then floating rate loans’ advantage is lower interest rates at present. That is, even after accounting for the current and expected rate hikes in the next couple of years.

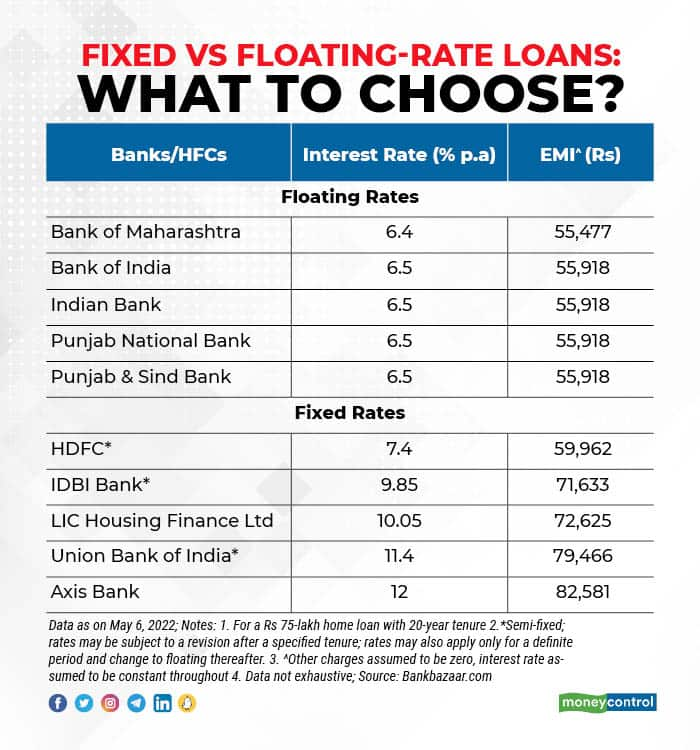

According to data from Bankbazaar.com, only HDFC offers interest rates of 7.4-8.2 percent on its partially-fixed-rate loan (Trufixed) of Rs 30 lakh, where the interest rate is fixed for two years and floating thereafter. Other banks on the list offer fixed/semi-fixed rates of over 9.85 percent on their home loans. The interest burden could be more taxing for those with lower credit scores. So, even if theoretically the fixed-rate loan concept does make sense in some cases, practical challenges abound. “Any fixed rate beyond 8.25 percent will not help the borrower’s cause. It would not be wise to switch to such expensive fixed-rate loans,” says Patel.

Moreover, you also have to factor in other charges involved in making a switch from floating to fixed loans. For instance, you have to pay neither prepayment nor foreclosure charges in the case of floating-rate loan refinancing. However, if you are stuck with a fixed-rate loan, you will have to pay foreclosure charges for a balance transfer. “These charges become barriers to pre-closure and also add to the cost of borrowing. There is no point in taking a 10-12 percent fixed-rate loan when you could get a floating rate loan under 8 percent even with a modest credit score,” says Shetty.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.