Fifteen years ago when you opened your Public Provident Fund (PPF) account, retirement may have felt like a distant event. The annual deposits were small at first, the passbook entries routine and the promise of tax-free returns something you barely thought about year after year. Now, as the account reaches maturity, that quiet, disciplined habit has turned into a meaningful sum and a decision point many savers don’t prepare for.

When a PPF account matures after 15 years, it isn’t simply about withdrawing the money. Should you close the account and take the corpus, extend it and keep earning tax-free interest, or continue contributing? Each option comes with different implications for liquidity, returns and retirement planning and the “right” choice depends as much on your life stage as on tax rules.

Understanding what happens after PPF maturity is crucial because a well-timed decision can help your savings keep growing quietly and tax-free, while a rushed one could limit flexibility later.

Here’s how post-maturity options work, what the tax rules say and which option works the best for you.

What happens after PPF maturity?

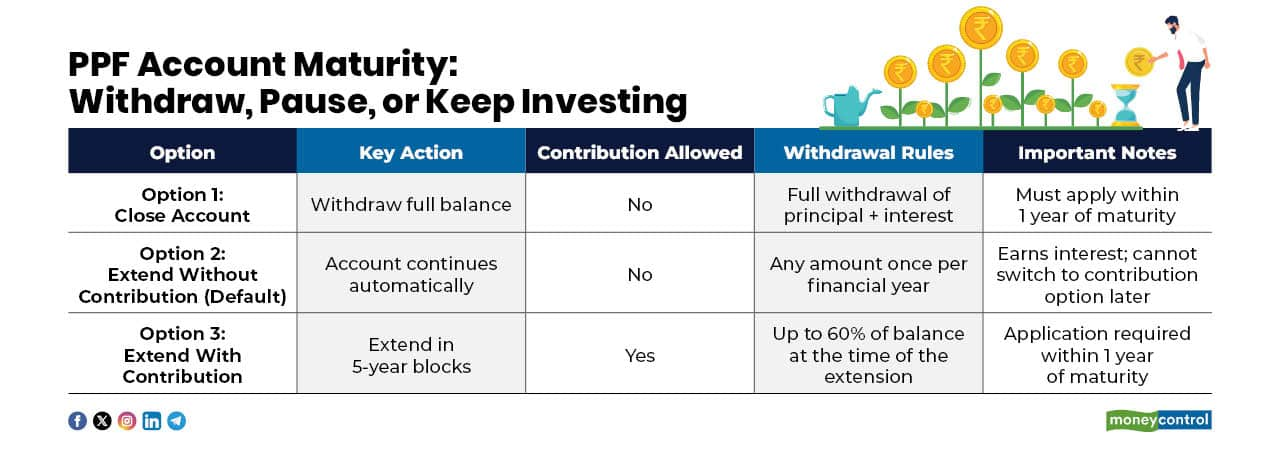

Once the retirement account completes its 15-year tenure, it does not end automatically. The account holder has to decide how to proceed, depending on their financial needs. At maturity, PPF offers three options, each with different implications for contributions, withdrawals and liquidity.

The first is to close the account and withdraw the entire balance. This can be done by submitting an account closure form along with the passbook. The full maturity amount is paid out, bringing the PPF journey to a complete close.

The second option is to keep the account active without making fresh contributions. In this case, the existing balance continues to earn interest at the prevailing PPF rate. The account holder is allowed one withdrawal in a financial year, offering limited liquidity while preserving tax-free growth.

The third option is to extend the account in blocks of five years with continued contributions. This extension can be exercised any number of times but the account holder must submit Form 4 (also known as Form H) within a year from the date of maturity. If this form is not filed within the stipulated time, the account is automatically extended without fresh contributions meaning the balance earns interest, but no new deposits are allowed.

Which option works best depends largely on where you are in life. “At an earlier stage, extending contributions helps build a larger tax-free retirement corpus due to continued earning capacity. At a mid-life stage, extending without contributions allows the accumulated balance to earn steady, risk-free and tax-free returns with annual liquidity. At an advanced stage, closing the account and withdrawing the full amount provides simplicity, liquidity, and ease of access to funds,” said Diviay Chadha, Partner, Singhania & Co.

With its fixed 15-year tenure and flexible extension options, the Public Provident Fund continues to offer savers a rare combination of safety, tax efficiency and choice, provided they understand the rules at the point of maturity.

How is the PPF tax structure

The Public Provident Fund follows the Exempt–Exempt–Exempt (EEE) tax framework, making it highly tax-efficient. “From a tax perspective, PPF follows an EEE regime—contributions, interest, and withdrawals remain fully exempt from tax across all stages,” Diviay said.

Contributions: Investments of up to Rs 1.5 lakh in a financial year are eligible for 80C deduction under old tax regime.

Interest: The interest earned on the balance is completely tax-free.

Withdrawals: The entire amount received on and after maturity is exempt from tax.

Opting to extend the account in a planned manner allows you to retain these benefits and keep your savings growing without taking on risk.

PPF interest rate for 2026

Applicable rate (FY 2025–26): 7.1 percent per annum, compounded annually

Interest credit date: March 31 each year

Method of calculation: Interest is computed on the lowest balance maintained between the 5th and the last day of every month

Loan Against PPF

A loan against a PPF account can be taken between the first and fifth year from the date of opening. The loan amount is capped at 25 percent of the balance at the end of the second year preceding the year of application. A fresh loan is permitted only once the existing loan has been repaid in full. If the loan is cleared within 36 months, the interest charged is 1 percent; beyond this period, the interest rises to 6 percent.

When and how are partial withdrawals allowed?

PPF permits partial withdrawals only after five financial years have passed from the end of the year in which the account was opened. Even then, the withdrawal is restricted to a maximum of 50 percent of the eligible balance.

This limit is determined by taking the lower of two amounts: the balance available at the end of the fourth year preceding the withdrawal year, or the balance at the end of the immediately previous financial year. For example, if an account opened in February 2019 had a balance of Rs 6 lakh in 2021 and Rs 8 lakh in 2024, the maximum withdrawal allowed in 2025 would be Rs 3 lakh.

How to open a PPF account online

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.