Building a meaningful retirement corpus under the National Pension System (NPS) means a long journey, often spanning two to three decades or even more. By the time subscribers reach the exit stage, the focus shifts from the accumulation phase to the distribution phase, which is how to turn that hard-earned pool of money into a steady income.

At present, for non-government subscribers with a corpus above Rs 12 lakh, up to 80 percent can be withdrawn as a lump sum or in a phased manner, which includes Systematic Lump Sum Withdrawal (SLW) and Systematic Unit Redemption (SUR). At least 20 percent must be used to buy an annuity that guarantees a lifelong pension, which creates a basic safety net, ensuring a minimum income regardless of how markets move.

While taking the lump sum is easy to understand, the real doubt begins when retirees opt for the phased withdrawal route. The impact on monthly income can vary widely. The choice decides whether the cash flow remains predictable or rises and falls with the market.

Here is the two option works:

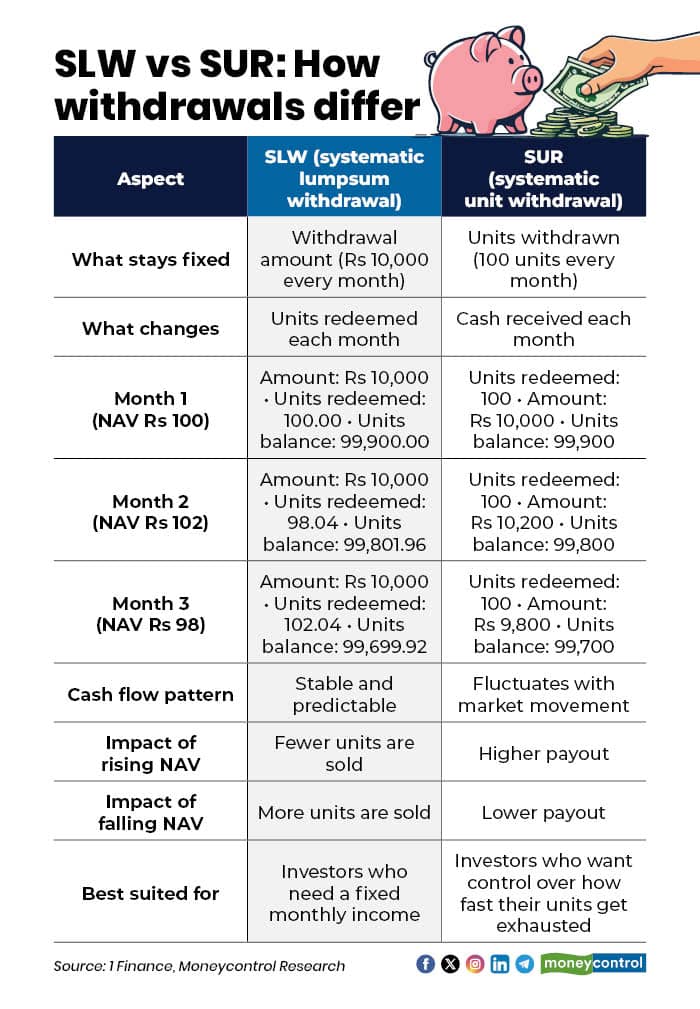

SLW: fixed amount; variable units

Systematic Lump Sum Withdrawal lets you draw a fixed amount of money every month, say Rs 1 lakh, regardless of how markets perform. The investor selects a predetermined rupee payout (for example, Rs 1 lakh a month). The number of units redeemed each time varies with the prevailing NAV, keeping the payout constant.

Withdrawals can be made up to the subscriber’s age of 75. According to the original SLW circular, dated October 27, 2023, subscribers may withdraw the lump-sum portion in installments at regular intervals (monthly, quarterly, half-yearly, or annually) rather than taking the entire amount at once. The minimum payout is Rs 500, according to the Fintech CRA mandate form.

“The lump‑sum withdrawal component at exit is exempt up to 60 percent of the accumulated pension wealth under Section 10(12A) of the Income‑tax Act. If you use SLW instead of taking that 60 percent at once, each installment is treated as part of that exempt lump sum, so long as the total you withdraw via SLW stays within your eligible lump‑sum limit,” said Anshi Shrivastava, Head - Personal Finance Training at 1 Finance.

Suppose your corpus at exit is Rs 30 lakh. The eligible portion of the corpus, Rs 18 lakh (60 percent) can be scheduled via SLW in monthly installments up to age 75; those installments are exempt until you fully exhaust Rs 18 lakh.

“Investors should watch out for any CBDT circular or finance act amendment that might extend the tax exemption beyond 60 percent,” Shrivastava addded.

SUR: fixed units; variable amount

Here investor selects a fixed number of units to redeem at each interval (for example, 100 units a month). The rupee proceeds vary with the prevailing NAV.

What should guide a retiree’s choice?

In retirement planning, the key decision isn't choosing the best option but picking the one that aligns with your income needs, risk tolerance and other cash flow sources.

Vishwajeet Goel, head of Pensionbazaar.com, said, “One should choose SLW (Systematic Lumpsum Withdrawal) over SUR (Systematic Unit Redemption) under NPS when income certainty matters more than market-linked upside. SLW suits retirees who need a predictable monthly income and have limited other earnings; it provides fixed payouts and budgeting clarity."

SUR works better for retirees with additional income sources and a higher risk appetite, as payouts fluctuate with markets but offer better long-term growth participation. "We believe the choice between SLW and SUR should depend on a retiree’s need for income stability, alternate income sources, and comfort with market volatility,” Goel said.

Over five to 10 years, SLW may provide a stable income but can deplete the corpus faster in falling markets, as more units are redeemed when the NAV drops (sequence risk). SUR maintains unit-redemption consistency and better protects the corpus structure but monthly income fluctuates with market movements, exposing the retiree to payout volatility, Goel said.

Taxation

Under the recent Pension Fund Regulatory and Development Authority (PFRDA) changes, non‑government subscribers can withdraw up to 80 percent of the corpus as a lump sum at exit (with a minimum of 20 percent allocated to annuity).

“Under the present Income‑tax Act framework, up to 60 percent of the total corpus withdrawn at exit is exempt. Any withdrawal above the 60 percent threshold, whether taken as a single lump sum or phased via SLW/SUR, may be taxable as per the investor’s slab,” Shrivastava said.

When designing an SLW or SUR schedule, it is prudent to track cumulative withdrawals against the tax‑free 60 percent bucket to manage potential tax exposure, he said.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.