Returns on the National Pension System Tier I schemes have been mixed across asset classes and time horizons, with equity funds delivering up to 17.38 percent, government bonds 8.88 percent and corporate bonds 8.63 percent, the latest NPS Trust data shows.

NPS data on Tier I schemes, as of February 20, indicate that no single fund manager leads across all categories. While equity-oriented schemes continued to reflect market movements amid volatility, corporate bond and government securities funds offered relatively steadier returns across tenures.

At present, 10 pension fund managers under the NPS manage subscriber investments across equity, corporate and government bonds. We examined NPS Tier I schemes E, C and G, analysing returns up to February 20, 2026, and compared them with the January 17 update.

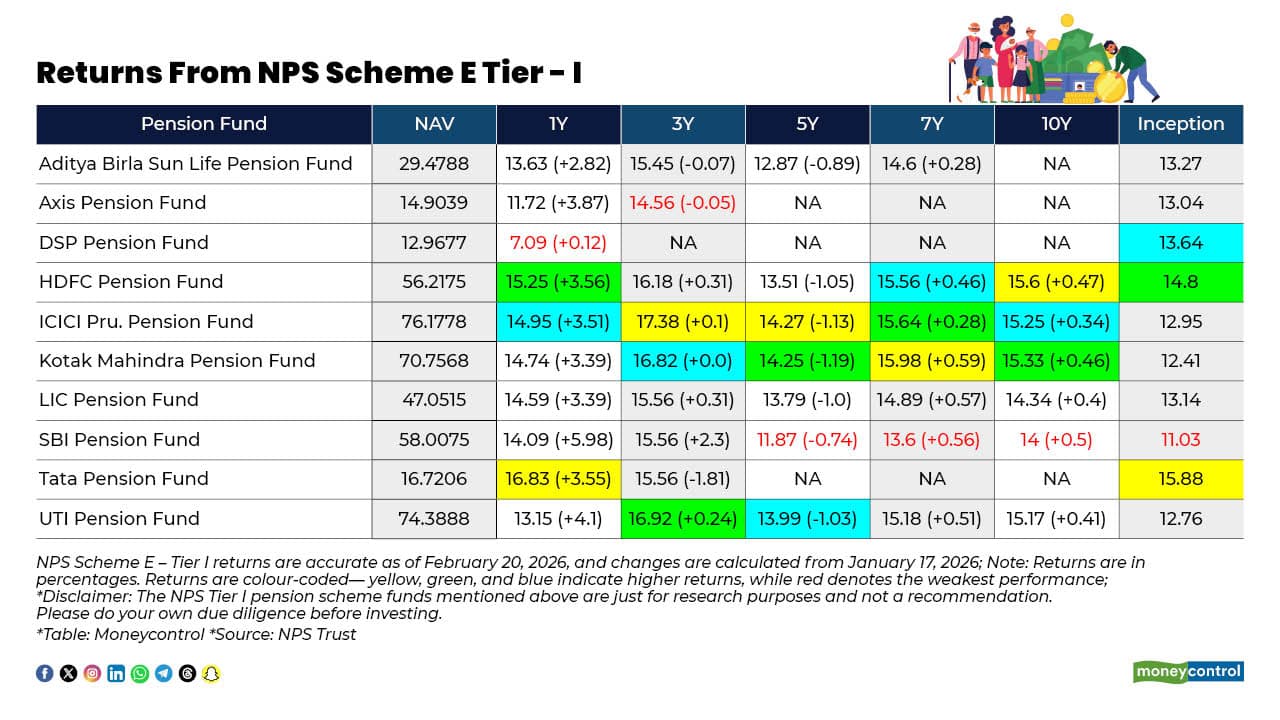

NPS Fund Performance: Scheme E-Equities (Tier I)

Risk level: high.

Under the NPS Scheme E Tier I, which focuses on equity investments, ICICI Prudential Pension Fund has shown consistent performance, followed by Kotak Mahindra, HDFC, Tata, and UTI Pension Funds. SBI Pension Fund, however, posted the weakest performance across the five-, seven-, and 10-year horizons, while DSP, Axis, and SBI recorded the lowest returns in the one-, three-, and five-year categories.

Overall, returns under the E NPS Scheme during the period up to February 20, 2026, ranged from 7.09 percent to 17.38 percent.

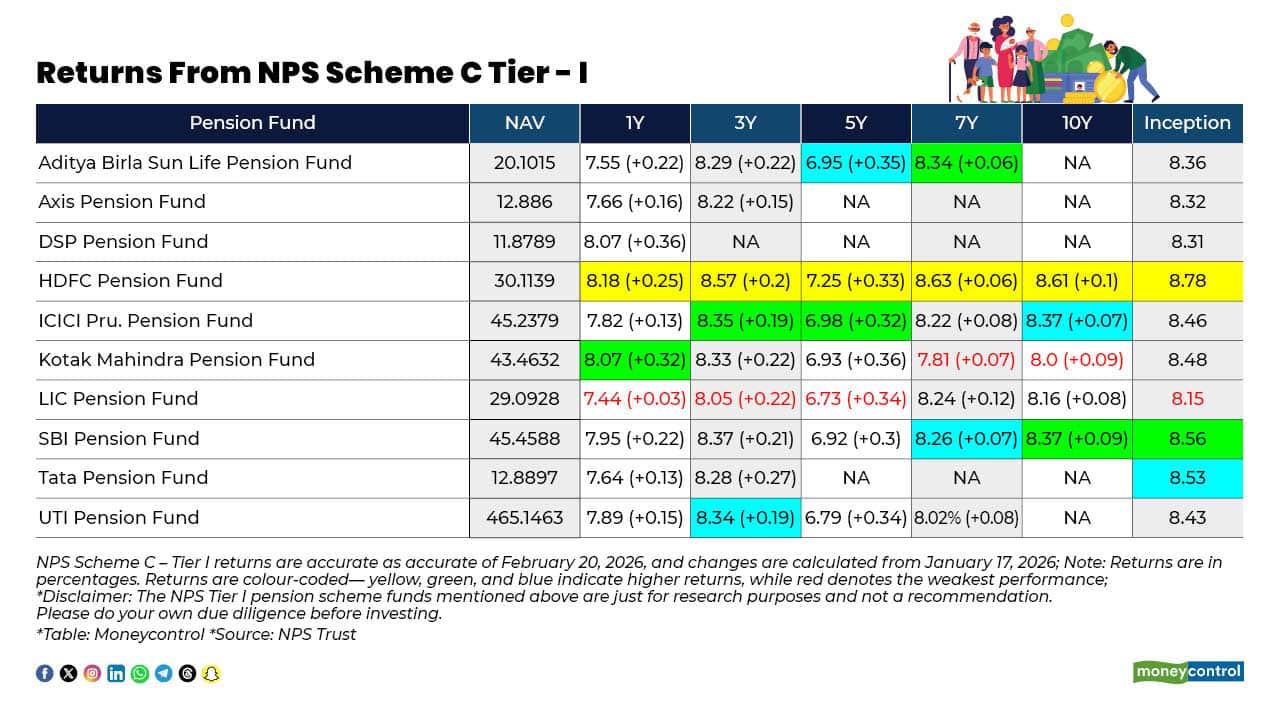

Scheme C-Corporate Bonds (Tier I)

Risk level: moderate.

Under NPS Scheme C Tier I, which focuses investments on corporate bonds, HDFC Pension Fund has shown consistent performance, followed by ICICI, Aditya Birla, SBI, and UTI. LIC, however, posted the weakest performance across the one, three and five-year year horizons, while Kotak Mahindra recorded the lowest returns in the seven and 10-year categories.

Overall, returns under the Scheme C NPS Scheme during the January 17 to February 20 period ranged from 7.44 percent to 15.88 percent.

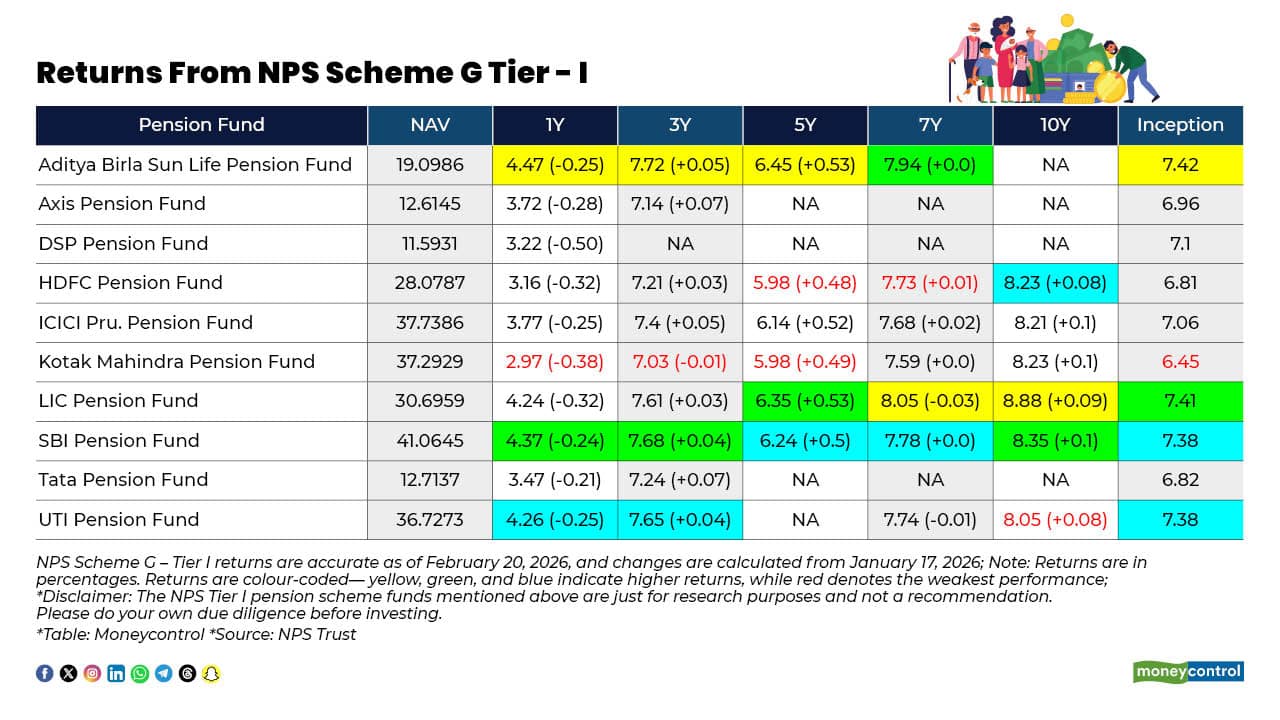

Scheme G-Government Bonds (Tier I)

Risk level: low.

Under NPS Scheme G Tier I, which invests in government bonds, Aditya Birla Sun Life Pension Fund has shown consistent performance, followed by LIC, SBI, UTI, and HDFC. Kotak, however, posted the weakest performance across the one, three, and five-year horizons. HDFC recorded the lowest returns in the five, seven-year categories, and UTI recorded the lowest returns in the 10-year category.

Overall, returns under the Scheme G NPS Scheme during the period up to February 20 ranged from 2.97 percent to 8.88 percent.

In equity schemes, ICICI Prudential Pension Fund emerged as the top performer, with 17.38 percent returns in the three-year category as of February 20. Within corporate bond schemes, HDFC Pension Fund posted returns of 8.63 percent over seven years. LIC Pension Fund led the government bond category with 8.88 percent returns in the 10-year segment.

What is NPS Tier I Scheme?

The National Pension System (NPS) is a government-sponsored retirement fund that allows investors to save for retirement while providing exposure to a diversified portfolio of assets. It offers partial withdrawal facilities and can be accessed across schemes for government and corporate sector employees, all citizens, and low-income groups, with the option to choose from auto-choice and active-choice funds.

To get started, a subscriber must open a mandatory Tier I retirement account, which comes with an age-appropriate asset allocation strategy that gradually reduces equity exposure as the subscriber ages but subscribers can choose to invest through different frameworks.

Common Scheme: It is the traditional NPS structure, where each pension fund manager offers one scheme per asset class, one equity (E), one corporate bond (C) and one government bond (G) scheme. Subscribers choose how much to invest in each asset class, but within a single scheme per category.

Multiple Scheme Framework (MSF): Enables PFMs to offer multiple schemes within the same asset class. Investors can allocate 100 percent to equities or create a mix of E, C, and G assets. It offers greater flexibility in terms of choice and control over assets to investors as compared to a common scheme.

Active Choice: This option allows subscribers to allocate funds themselves across asset classes, suitable for investors who are experienced in tracking periodic returns, as with mutual funds.

Auto Choice: Best suited for beginners, as asset allocation is automatically adjusted. This segment of investment follows an age-appropriate investment strategy, with equity exposure higher when young and gradually shifting as subscribers grow older.

These investment choices under NPS Tier I schemes have been balanced to help subscribers achieve their target returns to accumulate long-term wealth for retirement. Besides, the NPS has expanded its ecosystem to include schemes for central and state government employees and the corporate sector. There’s also the All Citizen Model. The NPS Lite scheme is designed for low-income groups. Importantly, returns vary across schemes.

Investors should exercise caution and carefully plan when selecting an NPS fund manager, and ensure that their asset allocation aligns with their risk appetite and long-term financial goals before investing in the National Pension System.

Disclaimer: The views and investment tips expressed by experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to consult certified experts before making any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.